Advertisement

Anonymous

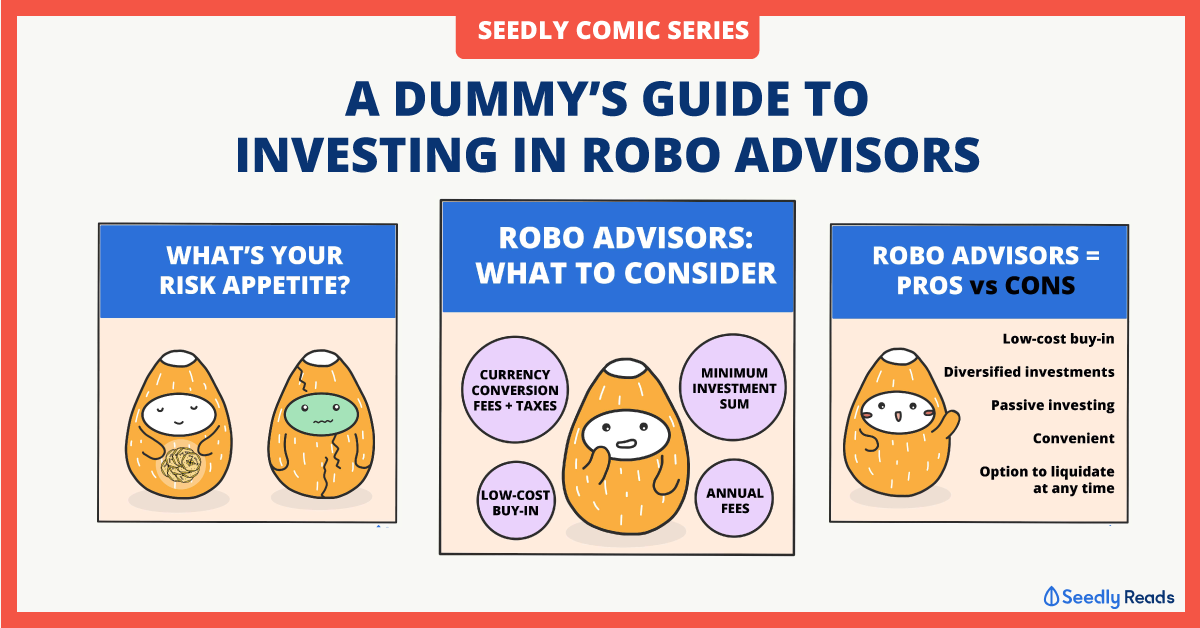

I have just come to know about Robo Advisors. Would like to ask if Robo Advisors or Financial Advisors would be a better choice?

18

Discussion (18)

Learn how to style your text

Jonathan Chia Guangrong

07 Jun 2019

SOC at Local FI

Reply

Save

Here's my personal thoughts if you are looking to invest- go with Robo Advisors. If you are looking for entire portfolio mgt advice, perhaps FAs might suit you better.

First off understanding todays context, Robo Advisors has entered only within the past few years and been picking up traction recently, undercutting not just FAs but traditional fund managers and fundhouses in terms of attractiveness of charges. In fact, FMs and FHs and now scaling back their margins to simply stay relevant.

Essentially, the business models of Robo Advisors has been designed to minimise the inefficiencies of existing traditional structures- going through FAs-FA's company-Investment product's company-before reaching the Fund Management Team(all of whom take a cut along the process). Of course there is the question of whether Robo Advisors perform as well as Traditional Fund Management Teams, but I believe a little researching would reveal Robo Advisors are not much worse off, if at all, to justify the hefty charges of Traditional FMTs, much less transacting bottom up through FAs.

That being said, there is still due diligence to be done on the consumers end. There are now plenty of credible Robo Advisors in Singapore- eg. Autowealth, Smartly, Stashaway. In fact, Banks such as OCBC are catching on with RoboAdvisors of their own. My advice- look not just on their charges but beyond that, eg. the teams credibility with managing funds, whether they publish their existing portfolio track record, i.e indicators that show how their algorithms and strategies have been performing against index benchmarks. If such information is not readily available online, set up a meeting with their company team and request for these. Clarify as many queries as you have. As an potential investor, you deserve to know as much there is to know.

Reply

Save

Firstly, you can look at the fees charged by both. Traditional investment advisors typically charge anywhere from 1% to 3% of the value of your portfolio, while robo advisors charge less than 1%. You are essentially paying more for more personalised services.

Next, if you are someone that likes personal contact with your investment, financial advisors would be a better choice. If you are contended with not having personal contact, Robo Advisors would be a better choice.

If you are willing to let someone else do your investment, then a robo advisor would work. When you invest in a robo investing platform, the site will handle all of your investment activities for you.

Reply

Save

Hariz Arthur Maloy

07 Jun 2019

Independent Financial Advisor at Promiseland Independent

I'm an FA that can also distribute robo advisor options but also have his own managed portfolio service. Ultimately, it depends if you prefer passive or active management, plus if you'd like human advice on your investments instead of just a computer screen.

I would think that human advisors do better at explaining why you need to be invested even in an economic downturn and in fact top up your portfolios, while robo advisors would not be able to calm you down during negative performances.

Your investments are just one part of your entire financial plan as well, and having an FA handle that can also provide a more holistic view of your entire end goal.

Reply

Save

Cedric Jamie Soh

03 Jun 2019

Director at Seniorcare.com.sg

Robo advisors.

No emotions, stick to a crafted plan, only concern is to provide mathematically scri...

Read 3 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1293 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

658 Reviews

Syfe

4.6

934 Reviews

Related Posts

Advertisement

I'd think robo advisors will be a better choice. Not just fees wise, as Zann mentioned is lower (which will eat significantly less into account value over time), but also through the experience of the professional investment team behind each robo advisory. How many financial advisors out there know each and every mutual fund they market in depth and can choose the ones that fit your needs?