Advertisement

Anonymous

Would like to seek everyone's opinion on what credit card should i use to maximise the benefits. Mainly for paying 1) monthly insurance premiums 2) starhub bill 3) household electricity/water bill 4) very minor daily spending.?

3

Discussion (3)

Learn how to style your text

Reply

Save

Kenneth Lou

30 May 2018

Co-founder at Seedly

Really depends on whether you are a cashback person or a miles person also.

For a cashback person:

Ideally you can do both but for you, also depends which bank account you are using :) You can do the DBS multiplier strategy like what Gabriel Tham suggested. That will be able to help you classify as +1 more transaction type.

Or if all those are too complicated for you, you can consider the SCB unlimited cashback card which has pretty cool and rave 4 or 5 star reviews here: https://seedly.sg/reviews/savings-accounts

It's helpful cos really there is no need to overthink but get the 1.5% back on your spend. Not too bad :)

For a miles or points person:

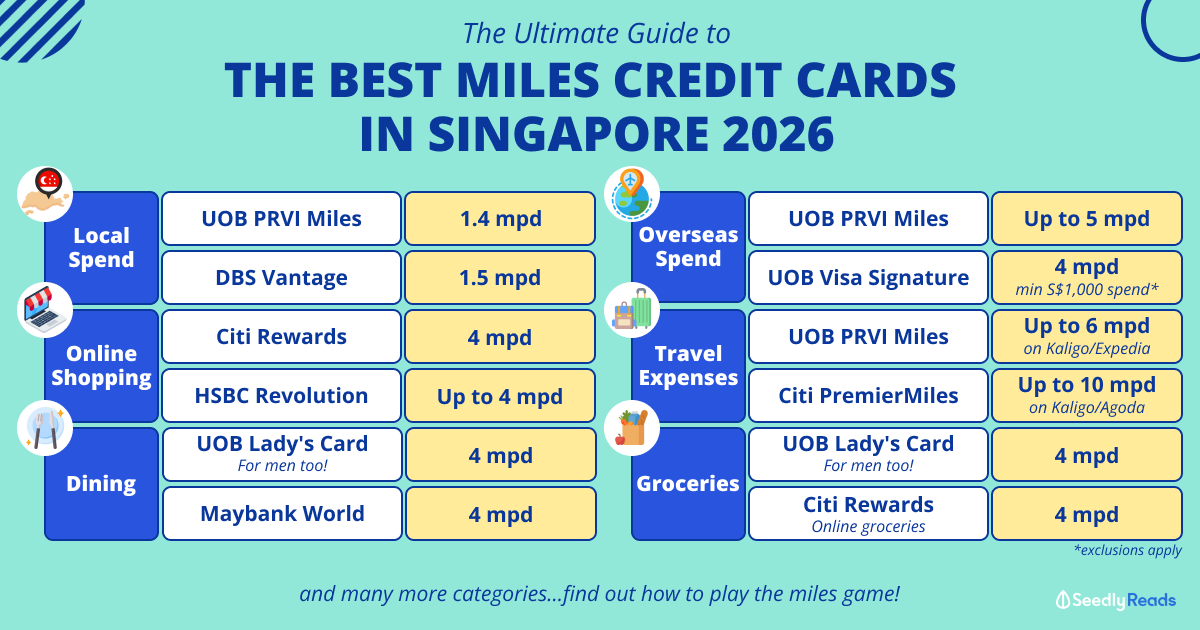

Can recommend you to consider the CITI rewards card, also very useful and effective for no min spend collection over time. https://seedly.sg/reviews/credit-cards/citi-rew...

You can read the reviews there and understand for yourself also! "Best card I have as i get the most rebates or miles out of it. On lazada membership giving lots of rebates for lazada (now 8% rebates), Grab and Chope and RedMart purchases and most miles for most online shopping. I only use this card for the 4x miles return for the above and avoid using it when it gives me less than that equivalent. "

Reply

Save

Gabriel Tham

30 May 2018

Tag Team Member at Kenichi Tag Team

I would choose the DBS multiplier account since you got bills, and small daily spendings.

Multip...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

Standard Chartered Simply Cash Credit Card

4.1

176 Reviews

Standard Chartered Simply Cash Credit Card

Up to 1.5% on eligible spend

CASHBACK

Unlimited

CASHBACK CAP

$30,000

MINIMUM ANNUAL INCOME

UOB One Card

4.1

166 Reviews

DBS Altitude Visa Signature Card

4.3

98 Reviews

Related Posts

Advertisement

Depending on how you utilise the cards.

1) I used OCBC Cashflo card for all insurance premiums. I converted all my premiums to yearly payments and clock it under thisthis card. Reason being, if the premiums are more than $1000, it will auto translate it into a 6 months instalment plan. If less than $1000 It's a 3 months instalment plan. All with no additionaadditional charges. Secondly, if the monthly payment exceeds $1000, it's a 1% monthly cash back. Lesser than $1000, it's 0.5% cashback.

Note: not alall cashback cards gives cashbacks for insurance premiums.

2) I put my starhub bills on recurring basis on my bonus saver credit card. Starhub gives me 100 free sms (for my grab hitch usage) monthly by doing credit card recurring payments. At the same time I gain usage at my card to increase my bonus interest (0.78% pa) earn on up to $100k deposits in my bonus saver account.

3) utilities bills are parked under my hubby's posb everyday card. He has a DBS multiplier account.

4) minor spendings will first be looked through the above 3 mentioned cards. If I have met the minimum, then the rest will be spend on unlimited card or Citibank rewards card. Depending on my spending in the month.