Advertisement

Anonymous

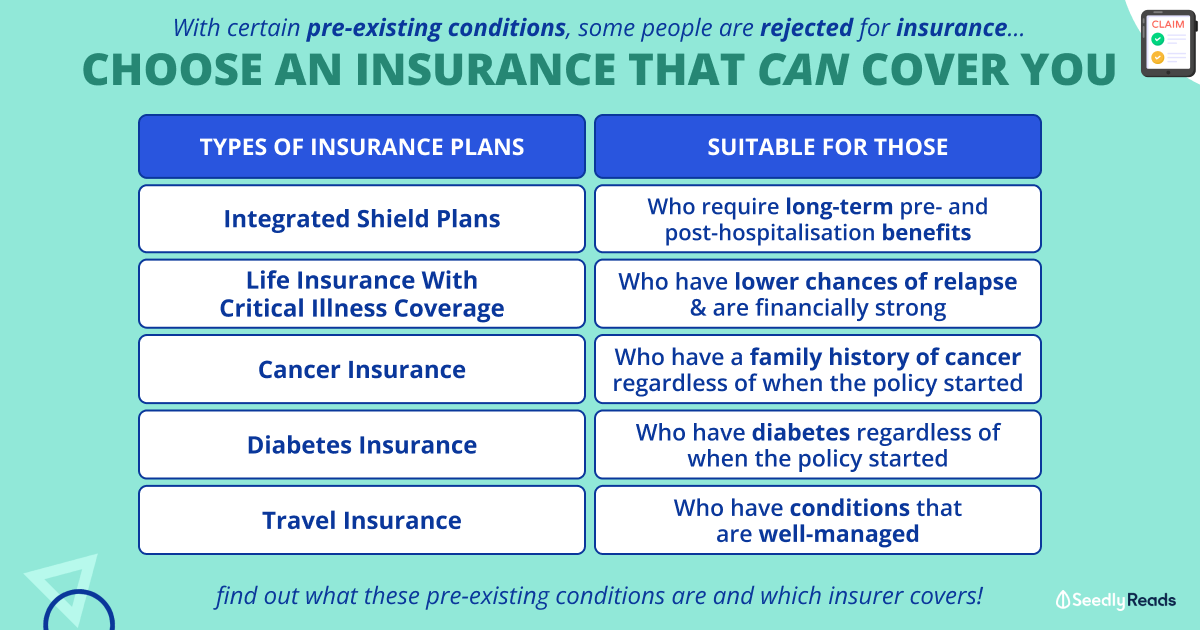

I am a 30 year old with pre-existing conditions, and most insurance companies have rejected my application for a shield plan. Should I take up the Raffles shield plan?

Raffles Shield plan offered me coverage excluding pre-existing condition and without a rider-costs about 223/yr. This cost via medisave could have been used to pay for my pre-existing condition consultations which i still go to every other yr. Taking up the shield plan, could mean out of pocket cost for the consultations and tests. Currently, i also do have hosp coverage from my workplace's insurance. Any thoughts on whether i should still take up the raffles shield plan? Thanks!

5

Discussion (5)

Learn how to style your text

Sam Wai Git

08 Sep 2020

Business Development Manager at Raffles Health Insurance

Reply

Save

Hariz Arthur Maloy

29 May 2020

Independent Financial Advisor at Promiseland Independent

Hi Anon, Raffles is offering you coverage while others have rejected in full? Getting most things covered even though pre-ex is excluded, which is expected, is all you can ask for.

Take it. You can use your group medical benefit to cover co-pays if they do. For your pre existing conditions, you'd still have Medishield Life to rely on if you're a Singaporean or PR.

Reply

Save

Pang Zhe Liang

29 May 2020

Lead of Research & Solutions at Havend Pte Ltd

For the same cost to you, it is either

Pay for your pre-existing medical condition; or

Get c...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

Raffles Shield Integrated Shield Plan

4.5

85 Reviews

Raffles Shield Integrated Shield Plan Private

$1,500,000

LIMIT PER POLICY YEAR

180 / 365 days

PRE & POST HOSPITAL

As Charged

OUTPATIENT BENEFITS

Private Hospital

WARD ENTITLEMENT

Income IncomeShield Integrated Shield Plan

4.4

311 Reviews

AIA HealthShield Gold Max Integrated Shield Plan

4.2

21 Reviews

Related Posts

Advertisement

Depending on what your pre-existing condition is, it may or may not make sense to take up a shield plan with exclusion.

Let's say for example someone has an exclusion on the "3 high" conditions, any other conditions related directly or indirectly will equally be excluded. If you think about heart attack, stroke, blindess, deafness, liver/kidney deterioration etc, all these conditions may be linked to the 3 highs which somewhat, the exclusion imposed might make the Shield plan pretty much meaningless.

A shield plan is nevertheless still the most important insurance plan (in my opinion) for a person who intends to stay in SG for long term, regardless his citizenship.

Also for someone who intends to retire in SG, please do not bang all your hopes on your employee benefits (aka workplace insurance) becaus one day you will leave the company volunteerily or involunteerily. By then, you may no longer be insurable by Shield plan.

If you haven't try to apply with all insurers, please give it a try. Evaluate which insurer offers you the best coverage since not all underwrites with the same rule for certain conditions.