Advertisement

Anonymous

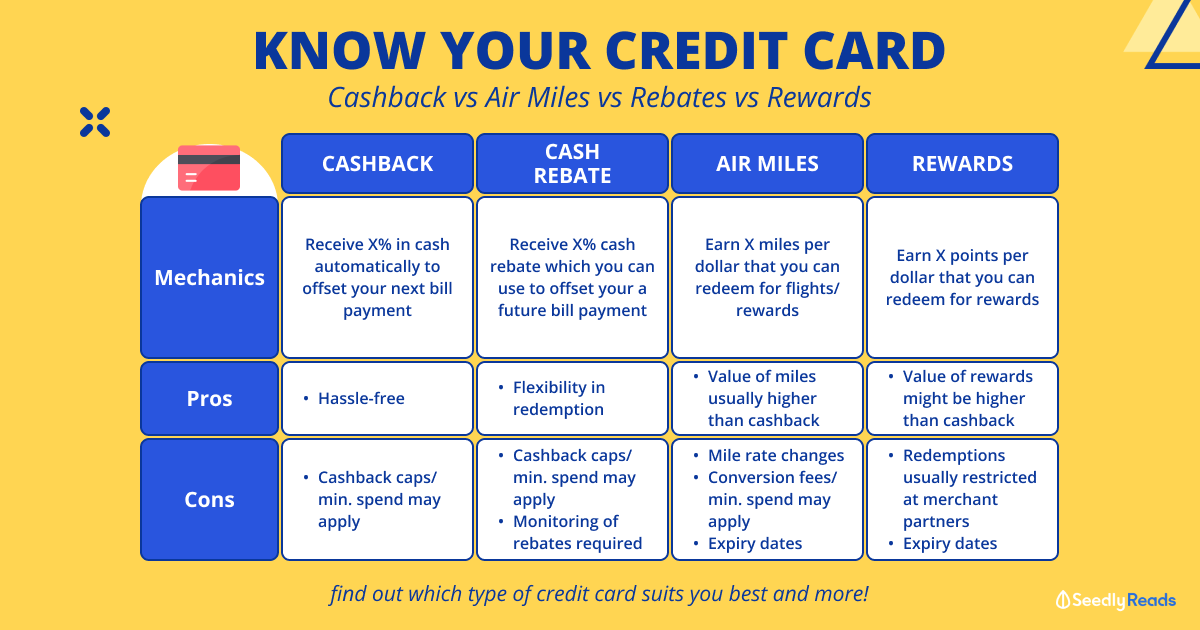

HSBC revo VS citi rewards

I would like to know the pros and cons of these 2 cards. Which would be good for normal grocery shopping and dining? I would also like to accumulate miles. Would u get 2 cards for different purpose or just 1 would do?

4

Discussion (4)

Learn how to style your text

thefrugalstudent

13 Apr 2021

Founder at thefrugalstudent.com

Reply

Save

Pang Zhe Liang

11 Apr 2021

Lead of Research & Solutions at Havend Pte Ltd

HSBC Revolution card is more for general spending where you can take advantage of contactless payment for up to 4 miles per dollar.

On the other hand, Citi Rewards is more for online spending where you can get up to 4 miles per dollar.

Given that your emphasis is for grocery shopping and dining, I believe the former will be more suitable. By and large, there is nothing wrong with holding both cards to expand your spending's versatility.

I share quality content on estate planning and financial planning here.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

Citi Rewards Credit Card

4.4

58 Reviews

2.27% cashback in local, dining, and retail

CASHBACK

1x reward point per dollar on all other spending

ALL SPEND

10x rewards points per dollar on online spending

ONLINE SPEND

HSBC Revolution Credit Card

3.4

48 Reviews

UOB One Card

4.2

168 Reviews

Related Posts

Advertisement

Hi Anon,

Here's what I can think of off the top of my head:

HSBC Revo Pros:

4 mpd earn rate with contactless payment on many different categories (including groceries and dining)

$0 annual fee

Free HSBC Entertainer subscription

Sign up bonuses available

HSBC Revo Cons:

4 mpd only with contactless payment (for retail spending)

4 mpd earn rate capped at $1k spending/month

Limited to Asia miles/KF miles

Citi Rewards Pros:

4 mpd earn rate on shopping & online spending

Widest range of airlines for miles transfer in SG

Many Citibank promotions at F&B/shopping outlets

Sign up bonuses available

Citi Rewards Cons:

4 mpd only on shopping & online spending (groceries and dining not included)

4 mpd earn rate capped at $1k spending/month

Reward points validity period is awkward (expire every 60 months from card opening date, so miles earned today = 5 years validity, but miles earned in 3 years = 2 year validity)

HSBC Revolution is definitely the better card to get for everyday expenses, although there's nothing wrong with having both cards especially if you foresee yourself spending more than $1k/month. In that case, you can use the Citi Rewards exclusively for online spending and retail shopping, and use the HSBC Revolution for all other expenses (dining. groceries, etc).

Hope this helps!

Regards,

thefrugalstudent