Advertisement

Anonymous

How does the Maybank SaveUp Account work? Any differentiating factor from other savings accounts?

Other than interest rates, what makes it different from the other savings accounts out there?

2

Discussion (2)

What are your thoughts?

Learn how to style your text

Carrie Rose

17 Apr 2020

Senior Research Analyst at ValueChampion

Reply

Save

The thing with multiplier accounts it that it depends on your eligible transaction amount monthly. You can use Seedly's Savings Account Comparison tool to check which is best for you: https://seedly.sg/reviews/savings-accounts

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

Maybank SaveUp Account

3.5

10 Reviews

Up to 3% p.a.

INTEREST RATES

$500

MIN. INITIAL DEPOSIT

$1,000

MIN. AVG DAILY BALANCE

Standard Chartered JumpStart Account

4.8

783 Reviews

DBS/POSB Multiplier Account

4.3

329 Reviews

Related Posts

Advertisement

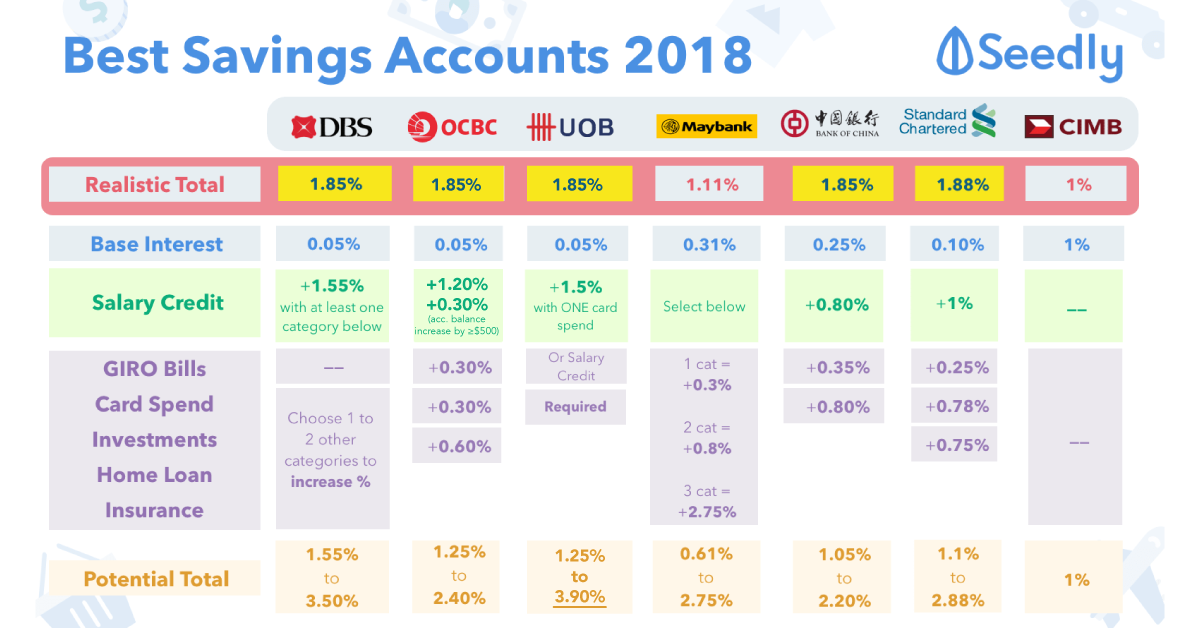

Maybank SaveUp Account is really interesting–though it's a bit more complex than a standard account (maximising your interest rate requires engaging with multiple bank products, just like with DBS Multiplier and OCBC 360 Accounts). Just as an intro, here's a quick breakdown:

You'll earn a base rate that varies by each "band" of your balance size

You can then boost your rate by engaging with other Maybank products (ie. loan, insurance, investment, credit card, etc). The size of the boost is based on how many products you engage with; 3+ products provides the largest boost at a (very) impressive +2.75% p.a.

So that's a basic rundown on the rates–but I know you're interested in how this structure makes Maybank SaveUp different. There are 2 main things that I would point to:

It's a lot easier to get the product-based boost than it is with other accounts. This is because salary crediting (S$2k/month) counts as 1 "product" in itself. If you pair this with a Maybank Credit Card (MB Platinum Visa or MB Horizon Visa) and spend just S$500/month, you'll hit the 2 product mark and get a meaningful +0.80% p.a. boost (not so bad, seeing as both of these card options come with relatively easy fee-waivers). If you need to take out a loan or insurance, you'll max out the bonus completely. Most banks do not count salary crediting and have more stringent product qualifications

You can reach the maximum effective interest rate (3.00% p.a.) at a S$50k balance. This is truly remarkable. Why? The rate is really competitive in itself, and the balance size is achievable for moderate savers. For most savings accounts, consumers need to have a balance of S$100k+ to max out their effective interest rate. At the S$50k level, their rates are much lower than achievable with Maybank SaveUp

If you're curious, I cover this account much more closely in a review below. Hope this helps!

https://www.valuechampion.sg/bank-accounts/mayb...