Advertisement

Discussion (5)

Learn how to style your text

Elijah Lee

22 Aug 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Jonathan Soh

20 Aug 2020

Wealth Manager at Aviva Financial Advisers

Hi there. Both are known companies in the insurance space. Aviva's term insurance is well known because of how value for money it is, especially with ongoing discounts. FWD is a newer entrant into the market with their term plans, being traditionally a general insurance provider. You can't go wrong picking either.

You can reach me here to find out more. I cover 9 major insurers including Aviva, NTUC, Manulife etc.

Reply

Save

Both are from reputable companies regulated by MAS, so both should be fine. Some things to consider:...

Read 3 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi anon,

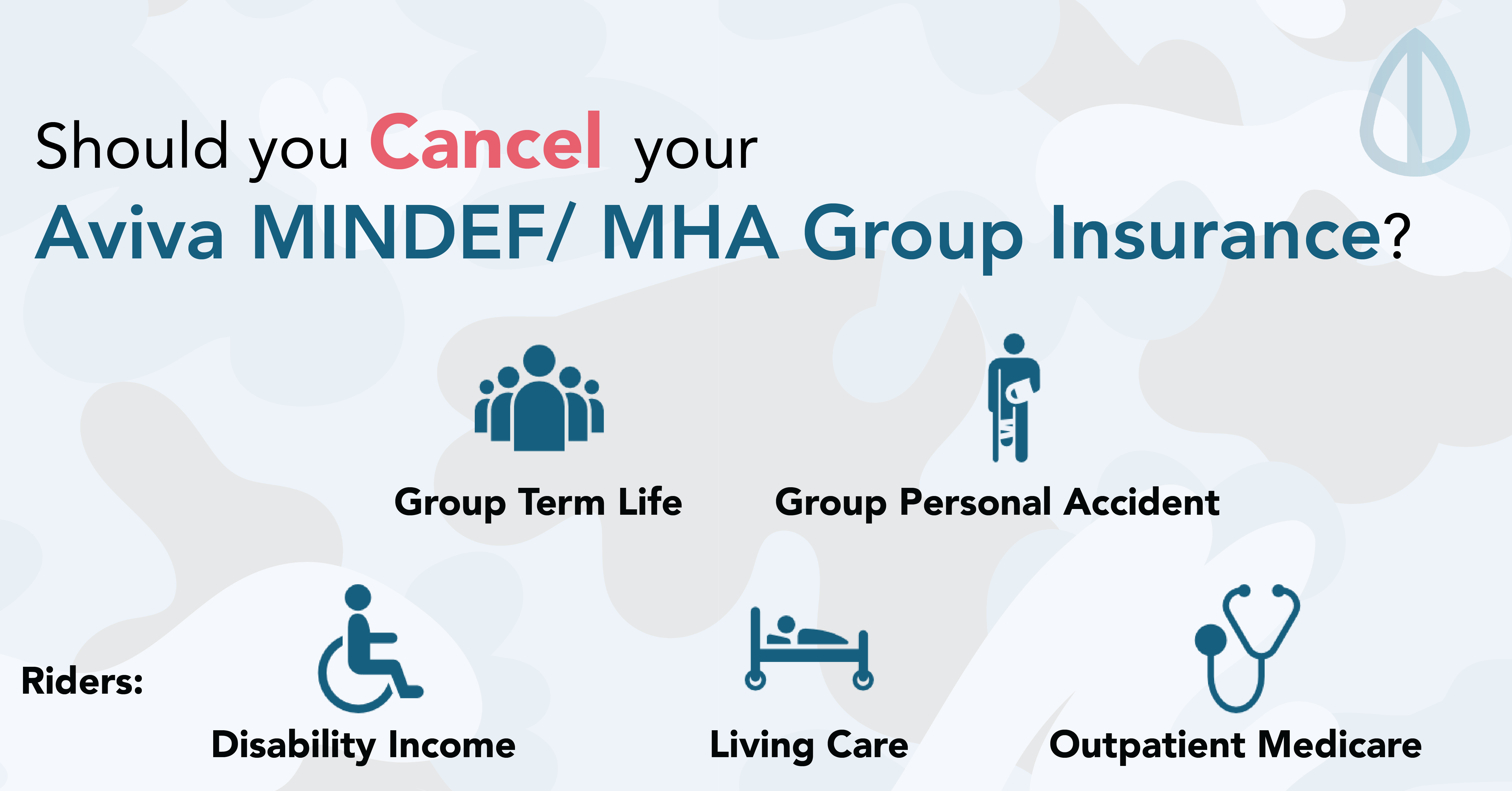

Without sufficient context, we can only assume that you are looking at getting individual term coverage from either company (and not the group term from Aviva)

In this case, you might want to compare premiums across the board for various companies, as the defintion of death/TPD is pretty much similar for all companies.

FWD's maximum for death/TPD is $1.5million if I recall correctly. Aviva allows more coverage, but subject to financial underwriting (you can't buy $10 million if you earn $50K/yr for example)

If you are adding CI on your term, the equation changes slightly. Note that FWD can only add on late CI (Aviva can add both ECI and LCI), but Aviva's early CI cover is additional payout. Both insurers have a CI waiver rider available. Some other insurers can also add early CI to their payouts.

Without enough information, I am afraid I can only speak in general terms.