Advertisement

Dear respected Seedly gurus, humbly seeking your advice with the following profile: Father (Age 68, Retired with no dependant, house fully paid and CPF of OA-290k, SA-69k, MA-52k, RA-138k)?

- What is the maximum that Daughter can contribute to Father's CPF for tax relief?

- What is the maximum that Son in law can contribute to Father's CPF for tax relief?

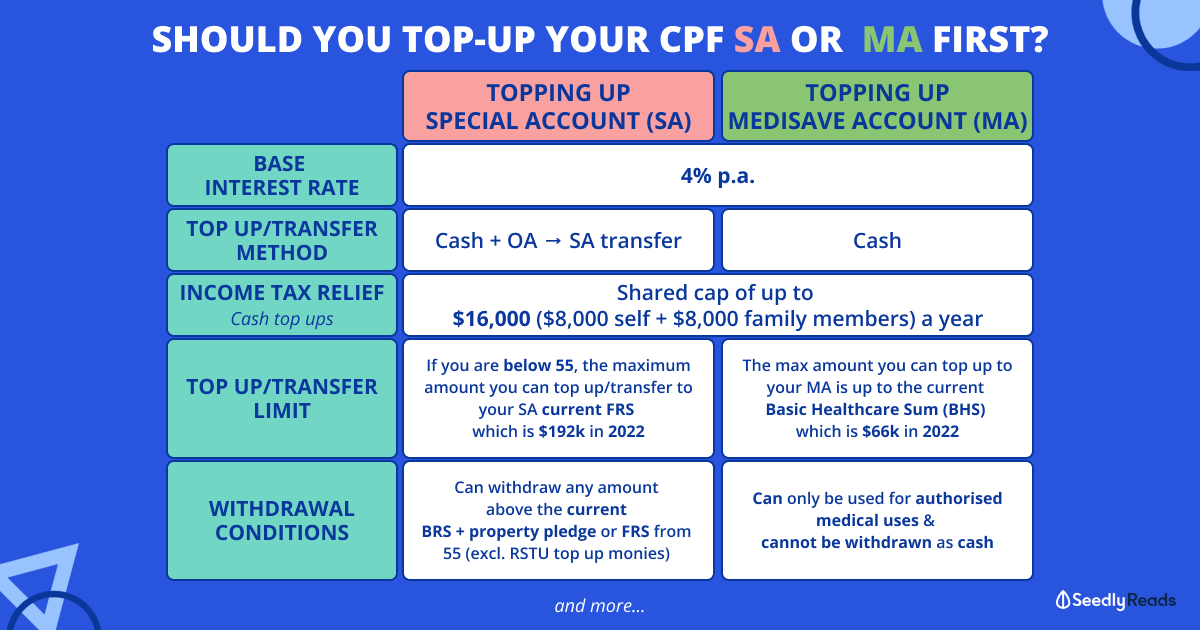

- Can/should contribute to OA/SA/RA?

- What is the max that Father can withdraw from OA or SA or both?

- Assuming the CPF monies is not needed as part of retirement, is it better to withdraw and invest in bonds that potential reap better % than CPF?

Thank you all in advance for your inputs.

11

Discussion (11)

Learn how to style your text

Reply

Save

Hariz Arthur Maloy

09 Jan 2020

Independent Financial Advisor at Promiseland Independent

Probably no more tax relief available. But I can't confirm. Will need to do a bit of a refresher.

Can consider contribute to RA if you want a higher RSS payout. Now that RSS money will last till 90 and not 95, you'll get a higher amount per year paid out. Alternatively, another private annuity may work with no capital drawdown but lower yield due to his age.

Do also check directly from CPF but I'm also assuming all his SA and OA is available with SA being the first account out first for withdrawal then OA. So 359k.

I say to beat 2.5% in OA with minimal risk is possible but 4% in SA, very unlikely. The only issue is he can't just take out OA money only. He has to take out SA money first. So maybe keeping in CPF could be the better option. But not saying it's not possible to beat CPF rates if you're open to some risk, but once you take out, cannot put back in.

Reply

Save

Elijah Lee

09 Jan 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi Musang,

- Daughter can contribute $7K via RSTU to father's RA per year for tax relief as long a...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

1) The max amount for tax relief would be 7k. This is because the RA is less than the current FRS (currently $176000 for YA2020). The current FRS amount changes every year.

2) Same as for the daughter in (1).

3) I don't think you can contribute to your father's OA/SA/MA as you can only contribute to your own account? Not sure if I am interpreting your question correctly. To assess whether you should do voluntary contribution to your own CPF would require more details on your current profile.

4) The following link by heartland boy details the calculation.

https://heartlandboy.com/money-withdraw-from-yo...

You will need to dig out the basic retirement sum for your dad's age and determine if you have sufficient property pledge.

5) It is hard for bonds to hit a higher % than CPF (unless u are referring to corporate/junk bonds). If you want a higher % it would be better to invest in equities but I would not really recommend that for your dad's age.

I'm not an expert in CPF so my answers may not be completely correct - do drop your questions to CPF I believe they will be able to answer them better (except for the last question)