Advertisement

Anonymous

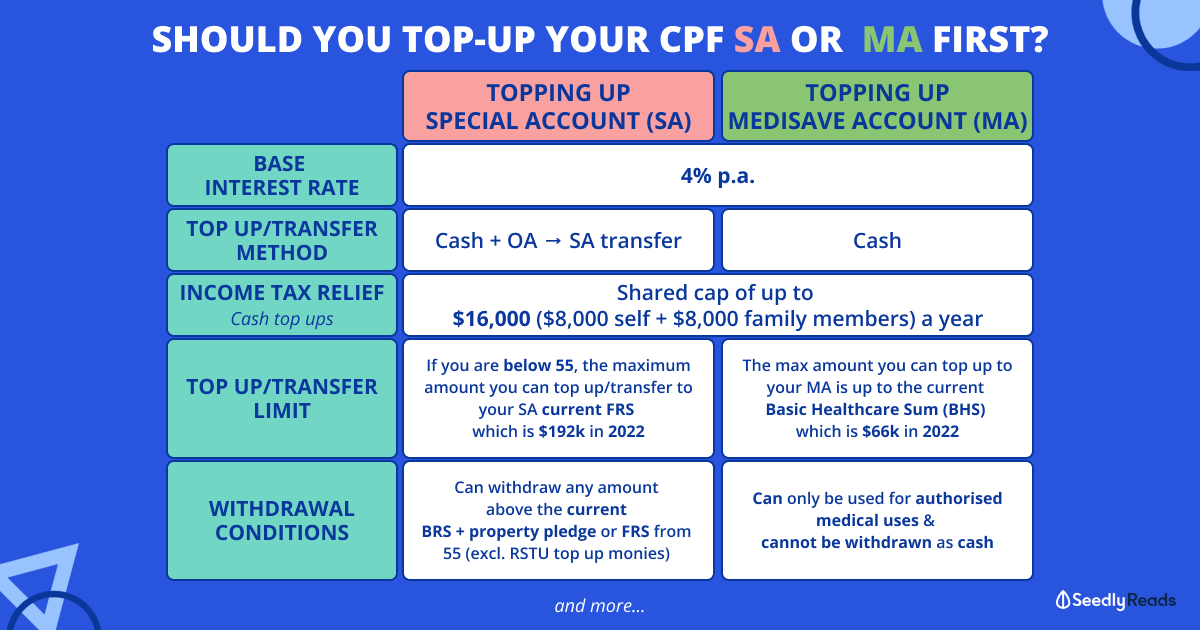

Cash top up to SA, SRS and MA? Which to prioritise or what factor to consider?

SA: FRS 181k, cap 7k

SRS: No limit?, cap 15.3k

MA: BHS, cpf contribution cap

-Just knew these, is my understanding above correct?

-Which will you advise to prioritise?

-Have not top up, can I top up lump sum max amt at once? Does it matter when to top up?

-For SRS, once I top up can immediately used it to invest? Any recommendation?

-Saw trsf from OA to SA, is it advisable? Or should accumulate 20k then invest?

-Are there things to consider when top up? No plan for house at least next 8 yrs.

4

Discussion (4)

Learn how to style your text

Reply

Save

Hi there!

For FRS:

It is the amount that will be transferred into the Retirement Account (RA) upon reaching age 55. The exact amount depends on when you reach age 55. Funds from Special Account will first be transferred into the RA, and followed by Ordinary Account should there be any shortfall.

For example:

Right before age 55

OA: $200,000

SA: $150,000

Upon reaching age 55

OA: $169,000

SA: $0

RA: $181,000

Also, for the $7K cap, I think you are referring to the tax-relief cap for cash top ups into your own SA. You can still choose to top up more, though the tax relief is capped at $7K

For SRS:

There’s no limit of how much you can have in your account. You are right that the current maximum yearly contribution (for Singaporeans) is $15.3K.

For MA:

The Basic Healthcare Sum is $60,000 this year. For those who have reached age 65 this year, it will be fixed for life. For those who have yet to reach age 65, it will be adjusted yearly.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1293 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

658 Reviews

Syfe

4.6

934 Reviews

Related Posts

Advertisement

This is a question with no right or wrong answer — but below is my opinion:

PRIORITIES

1.. If your income has not reached the CPF contribution cap, prioritize MA up to the BHS because:

2.. If you have exceeded the CPF contribution cap, prioritize SRS first (and yes you can and should invest the sum!) over top up SA in cash because:

3.. If you still have spare cash then top up $7k to SA for tax relief... If you still have cash even after that, consider topping up another $7k in cash to your loved ones CPF for tax relief as well

TIMING

Big picture wise though, timing is a much more minor decision than the decision about priorities.

TRANSFER OA TO SA

If you have no foreseeable use of your OA in the mid term future, then whether to transfer from OA to SA becomes a question of risk appetite (ie do you prefer a very safe 4% return or a potentially higher return in OA beyond the first 20k but with some risk).

I would say though that circumstances / plans do change, and I personally would think leaving $20k in OA just in case is not a bad idea..