Advertisement

What’s the difference between cash top up on SA and SRS?

I’m 30 this year, planning to top up SA with cash of $7k each year. Saw smth about SRS but am pretty unsure what is it about.

Can anyone shed some light? It will be great if there are articles to refer to or can share what are the various options of CPF top up and benefits. Thank you!

2

Discussion (2)

Learn how to style your text

Elijah Lee

13 Sep 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

There's plenty of articles comparing topping up the two accounts:

https://blog.seedly.sg/supplementary-retirement... (What Is The Difference Between Topping Up SRS vs CPF SA vs Cash?)

https://www.areyouready.gov.sg/YourInfoHub/Page.... (CPF SA vs SRS: Which is better?)

https://endowus.com/insights/three-things-to-do.... (Which account to prioritise? A returns and flexibility perspective.)

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi Daniel,

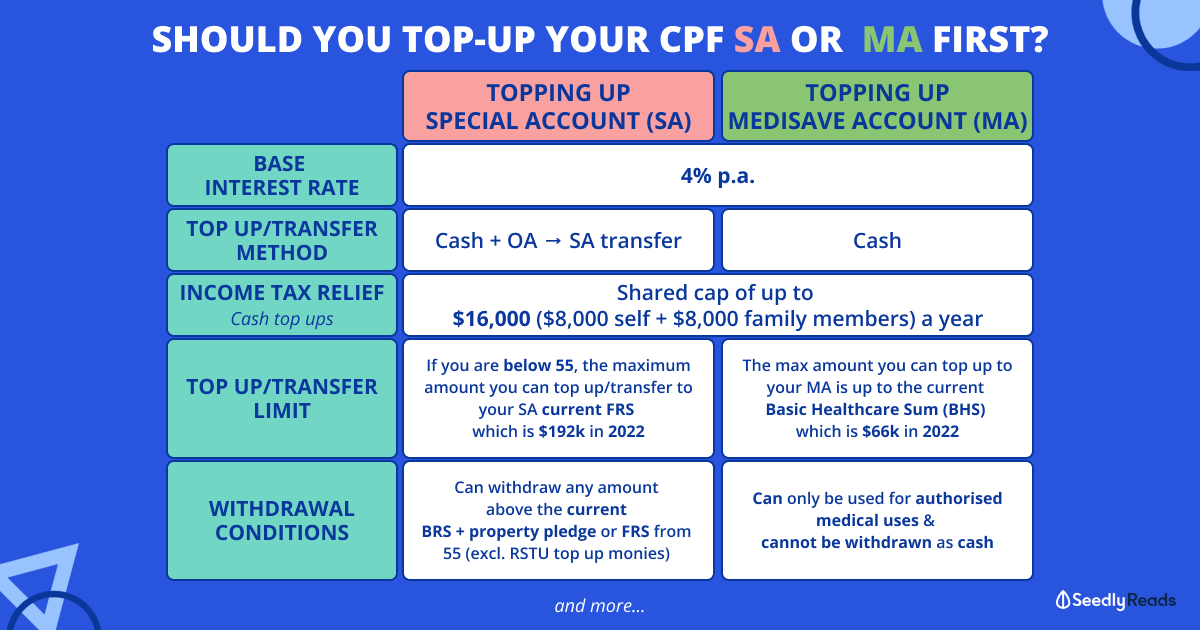

In a nutshell, topping up SA directly with cash of $7K/yr is known as the Retirement Sum Topping Scheme. You'll get tax relief of up to $7K, and this money will compound at 4% to help you reach FRS faster. However, there isn't much you can do with this money (not many investment options for CPF SA monies) but you might really be better off leaving the money in SA since it's safe there. You can top up as long as your SA has not yet hit the prevailing FRS.

Topping up SRS is capped at $15.3K a year (but no lifetime cap) and also confers tax relief on the full amount. However, the interest on SRS is only as high as the current bank interest rate (i.e. 0.05%) and thus you would want to invest your funds to grow it further. There are a wide range of instruments you can invest in, such as SG listed stocks, unit trusts, SG listed ETF, SSB, FDs, retirement income plans. You can take out the money subject to a 5% penalty if you really needed funds, if not, wait till 62 (the prevailing retirement age as of the year you open your SRS account) to be able to withdraw your money/assets. At that point, half of what you withdraw is taxed as income, the other half is tax free. Thus, withdraw after 62 if you have no other income and no more than $40K/yr to avoid being taxed. You have 10 years to withdraw, after which the SRS account is deemed close (unless you have bought an annuity plan that pays in perpetuity)

For further reading, Yang Teng has linked some articles.