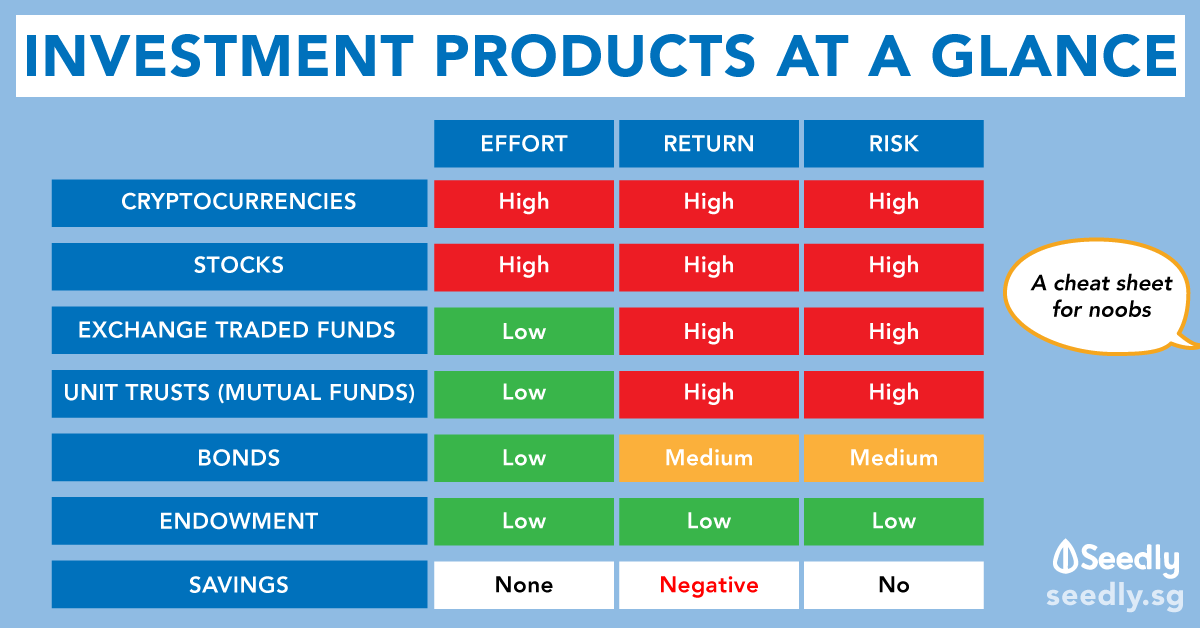

Advertisement

Why choose a Participating (par) product if are already doing investments yourself?

In a par product, the money goes to an investment fund and returns from that fund are used to pay the par benefits. The fund itself looks like a fairly well-diversified mix (at least for AIA - mostly fixed income with a minority of equities), all internally managed, no wacky assets.

I know there is some smoothing - but that just means good years pay less, and hold back and when there is a lean year - use heldback to payout more.

Why would this is better than just investment yourself?

3

Discussion (3)

Learn how to style your text

Loh Tat Tian

20 Nov 2019

Founder at PolicyWoke (We Buy Insurance Policies)

Reply

Save

Hariz Arthur Maloy

19 Nov 2019

Independent Financial Advisor at Promiseland Independent

Let's say theoretically you invest in a similar portfolio allocation as a participating fund. A conservative 30% Equity, 65% Fixed Income, 5% Property portfolio.

If you manage costs well, you'll probably receive a slightly higher compounded return as compared to an endowment doing the same.

However with an endowment, there'll always a be a floor of guaranteed return that the portfolio may not have. And you take emotions and decisions out of managing the portfolio bh yourself.

Like hiring an advisor, you're paying for advice and management. That's just what an endowment is. You pay for the advice by the insurer taking a spread on your returns with a management component that makes sure you have a guaranteed return, that also takes profit yearly in the form of Reversionary bonuses.

Reply

Save

Pang Zhe Liang

19 Nov 2019

Lead of Research & Solutions at Havend Pte Ltd

In investment, the returns are always non-guaranteed (assume we have very strong knowledge and techn...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

It has to do a lot with the following:

(1) Par funds are created as a safe and diversified portfolio which removes all the required thinking, managing and decision making process to the insurer/fund manager that does it.

(2) Its also designed to give gauranteed and non-gauranteed (portion in Benefit Illustration), which in about 95% case, safe enough.

(3) You pay fees for the peace of mind, and having others to manage it for you while you focus on other jobs and aspect of your life.

For returns, anything above 2.5% (fixed deposit etc) has risk which comes in many forms (investment non-gauranteed and base off your exit of investment) and types (CPF SA - long term lock-up, political risk etc). Even inflation is a risk for not doing anything to your money.

So the benefits of a par plan is lower returns in return for smoothed and gauranteed 1% with potential of up non-gauranteed (but gauranteed yearly once bonus is declared) to 4% (perpetual endowment).