Advertisement

Anonymous

(Stocks Discussion) SGX: Riverstone (SGX: AP4)?

Discuss anything about Riverstone SGX: AP4 share price, dividends, yield, ratios, fundamentals, technical analysis and if you would buy or sell Riverstone SGX: AP4 on the SGX Singapore markets. Do take note that the answers given by our members are just your opinions, so please do your own due diligence before making an investment in Riverstone SGX: AP4

2

Discussion (2)

Learn how to style your text

Reply

Save

TL;DR: Riverstone is currently trading at its 52-week low. Revenue in 1Q2019 saw a 14.6% increase YoY.

Business overview

Riverstone is a Malaysia-based company that specialises in manufacturing cleanroom and healthcare gloves. Incorporated in 1991, they have since received significant awards and certifications.

Share price

The share price of Riverstone is trading at $0.97 (as of 17 May 2019). The 52-week L/H is at $0.96/$1.24, i.e Riverstone is trading near its 52-week low.

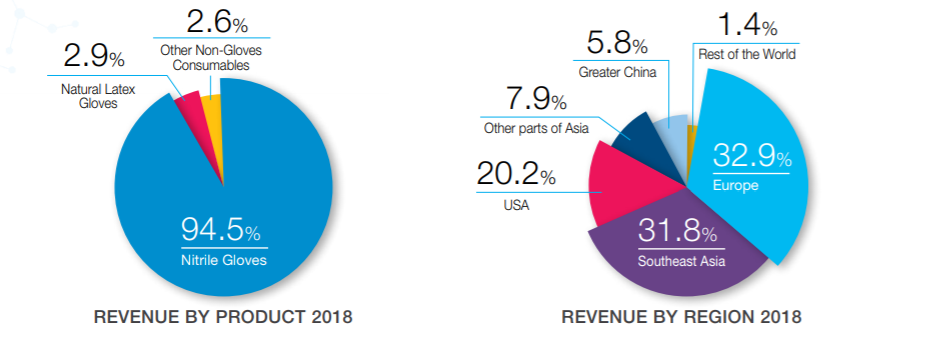

Revenue portfolio

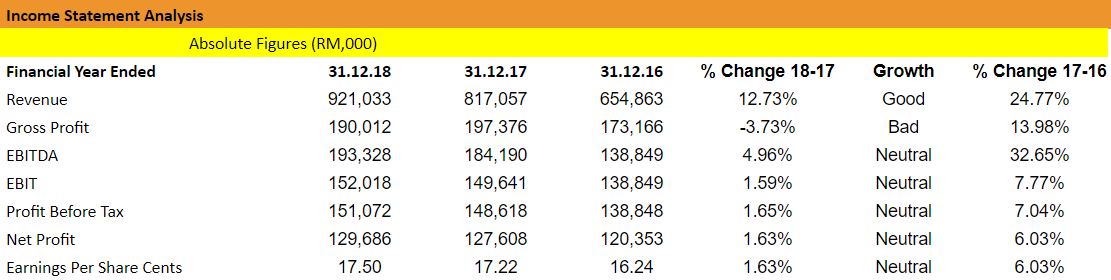

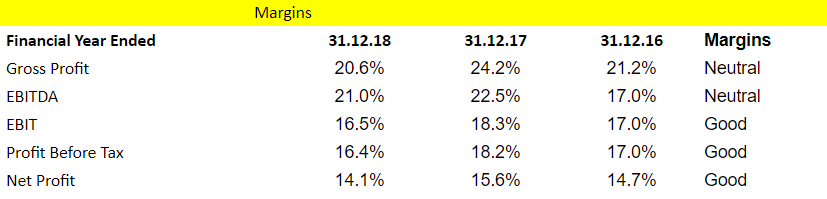

Financials

*note that figures are in RM

Dividend payout ratio of 40%, with a dividend per share of 7.0 sen per share.

P/E ratio sits at 16.6, which is pretty alright, not a great bargain but it could have been undermined by the lower profits. Their cash will be able to cover all their short and long term debt.

1Q2019 performance

Revenue in the first quarter grew, but the cost of goods increased thus leading to an overall decrease in net profits of 2.8%. Now they are undergoing phase six of their capacity expansion plans which they expect to add 1.4 billion pieces to amass a total production capacity of 10.4 billion pieces of gloves per annum by end FY2019.

SWOT Analysis

Strengths

- Expanding its production plants, which can bring about greater economies of scale with higher production.

- R&D and technical expertise: Being in the field for 28 years, they possess the strength in research and product development to produce high-quality healthcare gloves and that is used by multinational corporations.

Opportunities

- According to the Malaysian Rubber Glove Manufacturers Association, the rubber glove industry has been growing at an average of 8% to 10% for the past 25 years, and we expect this to continue in FY19. This is underpinned by the growth in the healthcare industry, an increase in hygiene standards and economic growth in emerging economies.

Threats

- High competition from other glove makers (such as in China), triggering a price war that impacts their margins and they are not able to pass on the rising costs due to competitiveness.

- A shortage of raw materials led to a 10.0% hike in average raw material prices, while a shortage of manpower toward the last two quarters affected their operating performance. They also faced a weakening US Dollar, a currency where the majority of our sales are denominated in.

Conclusion

In the first quarter of 2019, revenue increased but profits decreased. A decrease in profits doesn’t mean that we shouldn’t consider this stock. Although they are faced with macroeconomic risks, I feel that the fundamentals of this company are pretty strong, and they are undergoing expansion too which means higher revenue.

Links:

Reply

Save

Write your thoughts

Related Articles

Advertisement

I noticed Tracy Lim's post dated 4th June 2019 when the price was S$0.97 trading at 52 week low. Since then it has gone up to a high of S$2.01 on 31st August 2020.

Today, it hit a 52 week low of S$0.90.

Compared to Tracy's report in 2019, as of today.

Current Share Price: S$0.92

Market Cap: S$1.36B

Earnings per share: S$0.277

PE (Adj): 3.31x

Dividend Yield: 9.32%

Seems like a 2019 again with the price trading close to 52 week low today but with improved fundamentals at a lower price than in 2019.

What would you do? Would you buy? Or not?

Share your views with us.