Advertisement

Anonymous

Should I still contribute to my own CPF after I start my career in real estate? What other personal finance tips should I know as a self employed person?

7

Discussion (7)

Learn how to style your text

Rachel Yeo

19 Sep 2019

Content Strategist at Seedly

Reply

Save

Jonathan Chia Guangrong

27 Sep 2018

SOC at Local FI

Mm if you are not investment savvy and are looking towards the long term, contributing to CPF after embarking on your new career is a good choice. Other considerations to take note of are your insurance protection coverage. Make are these are in place before you start in real estate. All the best in your new career

Reply

Save

Jeff Yeo

27 Sep 2018

amateur Social contributor at School of social sharing

Emergency funds

- work out your basic expenses per month x 6 = emergency funds (x12 if market conditions are bad)

- regularly review the monthly spending to make sure your emergency fund can always cover you for 6 months.

CPF

- TOP up only after emergency funds are sufficent

investment

- build a dividend portfolio that can supplement your income

- stocks if your risk acceptance Is higher

Reply

Save

Loh Tat Tian

26 Sep 2018

Founder at PolicyWoke (We Buy Insurance Policies)

There are plenty to know for self-insured. The basics are

1) Know your income and expenses.

Income tax, medisave (declaration to CPF as self-employed)

2) Plan your cashflow very well. Plan for 1 year expenses first. (Self employed has unstable income)

3) Calculate your income tax. If assessable income more than $80,000 annum, do your tax relief (SRS preferred) to bring it to the lower bracket of 7%, Since your income tax rate will hit 15%. pass $80,000

With regards to your CPF, treat it as a bond segment if you are going BTIR, especially if you are doing retirement sum top up (tax relief up to $7,000).

Reply

Save

CPF is for retirement purposes. if you are disciplined enough and if you can get returns of more tha...

Read 3 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

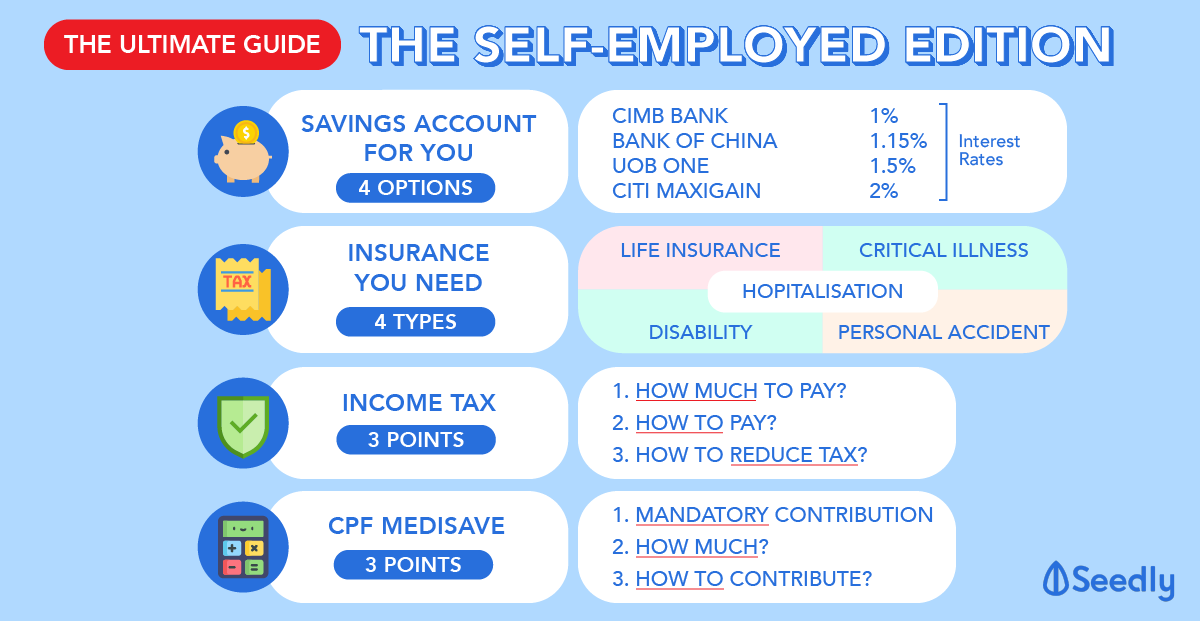

Hello! In terms of other personal finance tips for freelancers, you may find these articles useful:

https://blog.seedly.sg/self-employed-cpf-medisa...

https://blog.seedly.sg/freelance-insurance-sing...

https://blog.seedly.sg/freelancer-self-employed...