Advertisement

Anonymous

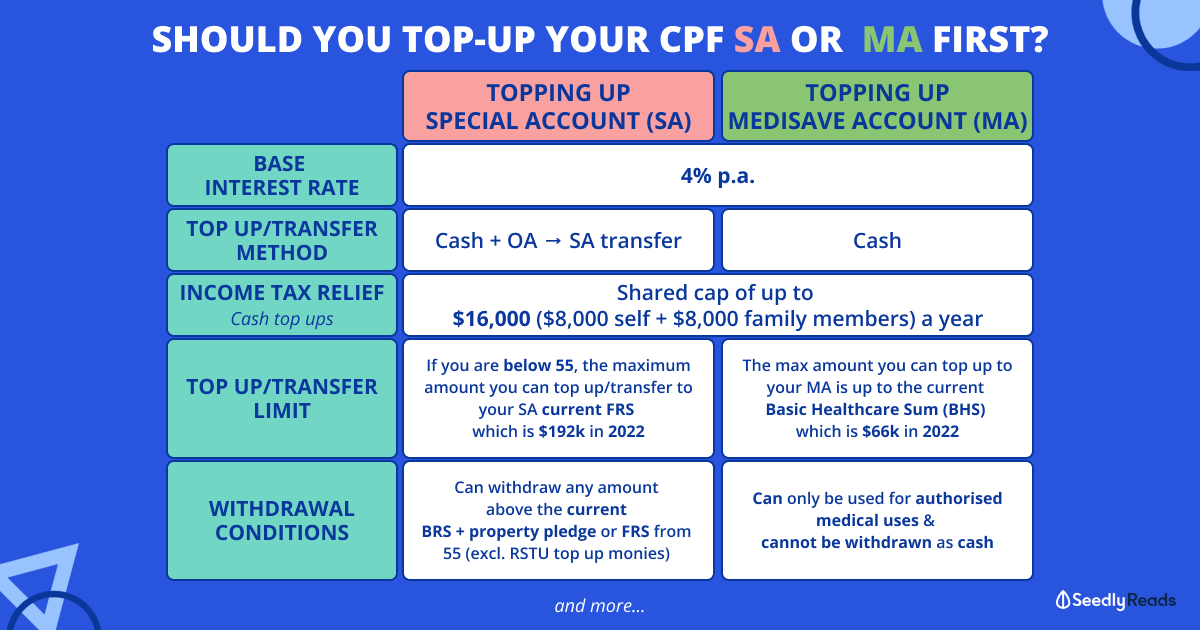

Is it the right choice for me to top up my son's CPF SA & MA to the full amount?

My son 26 had a trauma head injury and he is TPD. He had short memory too. We had ard 350k and decided to top up his SA & MA account for his retirement ard 200k and 150k to buy him an endowment plan (Any good endowment plan suggestions for 20 to 30years so that when he reach 45 or 50 he had some money?) We don't like investment cause we can't take any risk. I had 2 agents from prudential & great eastern. I doing some comparison between them & even some other company and can't decide yet. Thanks.

4

Discussion (4)

Learn how to style your text

Elijah Lee

08 Oct 2019

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Hariz Arthur Maloy

08 Oct 2019

Independent Financial Advisor at Promiseland Independent

Hi Anon, I can't imagine what you're going through right now as parents. I'm really sorry your family had to go through such an event.

There are a few things you may want to consider to help your son out. But here are some assumptions.

a) You'll be supporting him financially until you retire where hopefully there'll be enough income streams for the whole family to live on.

b) You'll be physically taking care of him until both parents are no longer around.

c) After you're no longer around, someone else has to take care of him and there's a need for income during this time as well.

So my suggestion would be:

1) You might want to buy a life policy on both parent's life as this will be used to help take care of him after you're no longer around. Include CI cover as well because if you need to take care of as well, that might be an issue.

2) Create a trust/foundation to manage the estate you leave behind to continue using this money to take care of your son. Create an instruction that will turn the lump sum into a product that will provide perpetual income for your son.

3) To buy products on your son's name that provides an income stream as soon as possible but choose to reinvest this money with the insurer until you need that income whether during your retirement or some other event.

4) I may not recommend using the money to buy future lumpsum products because you might need anticipated liquidity. This may include his SA top up because you can only effectively use that money after he turns 55, and CPF Life might pay at 65 or maybe even later. There's also no way to have an early surrender of this money for any circumstance.

5) Keep about 3 years of expenses in cash.

Instead of wealth accumulation, focus on income accumulation. If you can as quickly as possible create 2-3k/mth income without much market risk through lifetime annuities, this may be a good consideration.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi anon,

I'm very sorry to hear about what your son went through, as well as the emotional pain as parents that you would have endured.

In light of this, topping up of his MA and SA will be a good choice as the interest earned in MA and SA can snowball to a significant amount when he reaches the age where he can start to withdraw from SA (30 years from now), or when he will start to get payouts from CPF life (40 years from now). This is provided that there are no policy changes. MA interest is credited to SA when SA is full, and that helps compounds SA faster. When SA is also full, MA interest will credit to OA. SA interest will stay in SA. Thanks to compounding, this will give your son a good basic source of guaranteed income in his later years. Naturally, you'll want to make sure any of your own risks are mitigated as well, i.e. death/TPD/CI/Long Term Care on yourselves, and your own plans for your retirement.

I would like to point out that an endowment plan will be paying out in a lump sum, whereas a retirement plan would pay him a stream of income for a certain period. Assuming that you are looking for the former, there are many insurers that offer endowment plans (fixed maturity date), and some have perpetual endowment plans whereby the money in the plan will keep growing and you can choose to cash out when you need it (don't cash out too soon though). To do a proper and fair comparison, I would need to look at what samples in detail were given to you from the other insurers so that I can benchmark properly.

If it is actually the latter you are looking for, again, to run a fair comparison, we would need to see the options available and 'equalize' them in terms of premium, duration, etc. As I am from an independent advisory firm carrying multiple insurer products, I would be able to provide you with the comparison that you need to understand your options better and eventually reach a decision. To maintain privacy, feel free to reach out to me at [email protected] and we can converse there.