Advertisement

Anonymous

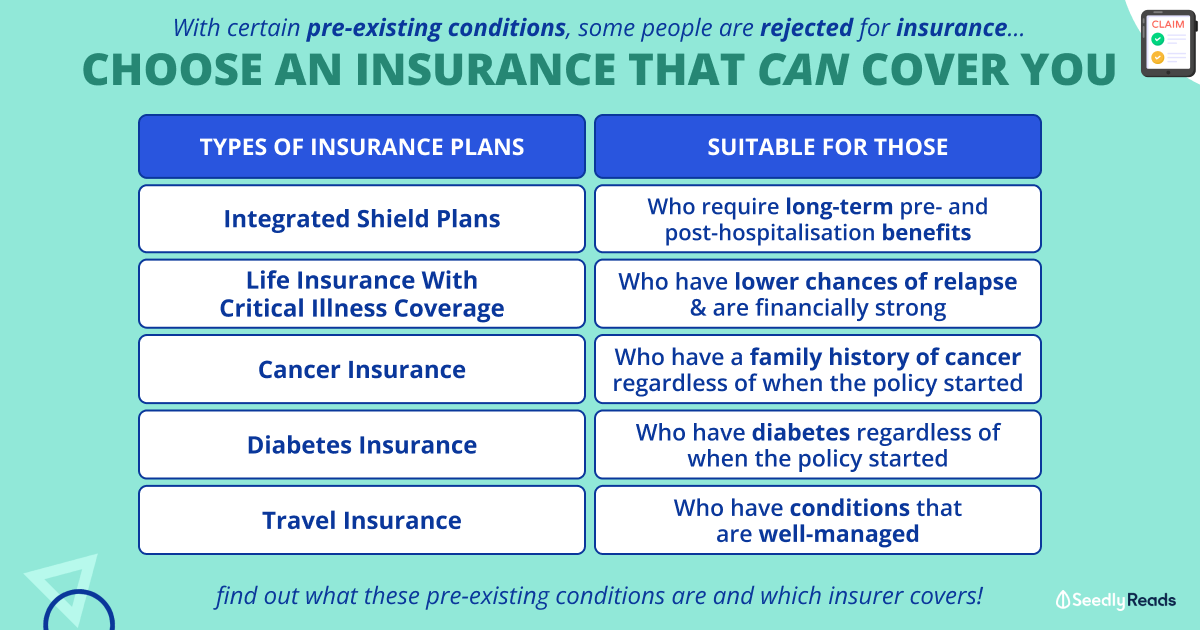

I've AIA essential max (no rider). Was told that I can switch AIA to Pru (with rider). If no pre-existing conditions, ok to chg & coverage will nt affected? true? Considering Term (ECI + CI): 250K SA, till age 65.. Premium range?

Am 33F, Income 48k.. Advice appreciated!

3

Discussion (3)

Learn how to style your text

Eric Chia

16 Aug 2018

Senior Financial Consultant at Prudential

Reply

Save

Hariz Arthur Maloy

15 Aug 2018

Independent Financial Advisor at Promiseland Independent

Hi Anon,

AIA's ISP is called the HealthShield Gold Max. The rider is called Max Essential.

If you do have the rider, you'll be penalised with the new 5% co-pay since the March announcement on changes to ISP Riders.

If you don't and sure that 100% healthy, you can do a switch. But honestly AIA HSG Max is pretty good and one of my recommendations to my clients.

Now for your life insurance.

The rule of thumb for death cover is 10 X your Annual Income, so you should looks at 480k of cover. ~ round up to 500k because got discount.

For CI cover 3-5 X your annual income is the rule of thumb. So that's 150k - 250k.

Whole life or term you can discuss with your advisor. I would suggest a mix of both.

On top of this you may be interested to get a Female Illness cover as well which will allow you to go for a full screening at a private clinic for free every 2 years and a reimbursement for skin grafting or masectomy. You can check out this page for more information. facebook.com/SGWomanInsurance/

Now, have you shopped around to get quotes from multiple insurers? You want to speak to an Independent FA for an unbiased comparison.

Reply

Save

Brandan Chen

15 Aug 2018

Financial Planner at Manulife Singapore

Let me address it based on 2 parts.

1) Replacement of AIA Health Insurance

- I'm not an AIA advis...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hello, not sure if you got the name of your policy right. If you have AIA essential max, that's the rider. If you signed the rider before 7 March 2018, please stick to it to retain full coverage after 2021. Otherwise, you'll have to transit to a copayment plan after 2021 when you switch now. So even if you do not have pre-existing conditions it's not recommended to change.

Term coverage until 65yo for $250k ci and $100k eci can be about $100/month. The earlier you take, the cheaper it is! Rates also differ whether you are smoker or non smoker.