Advertisement

Anonymous

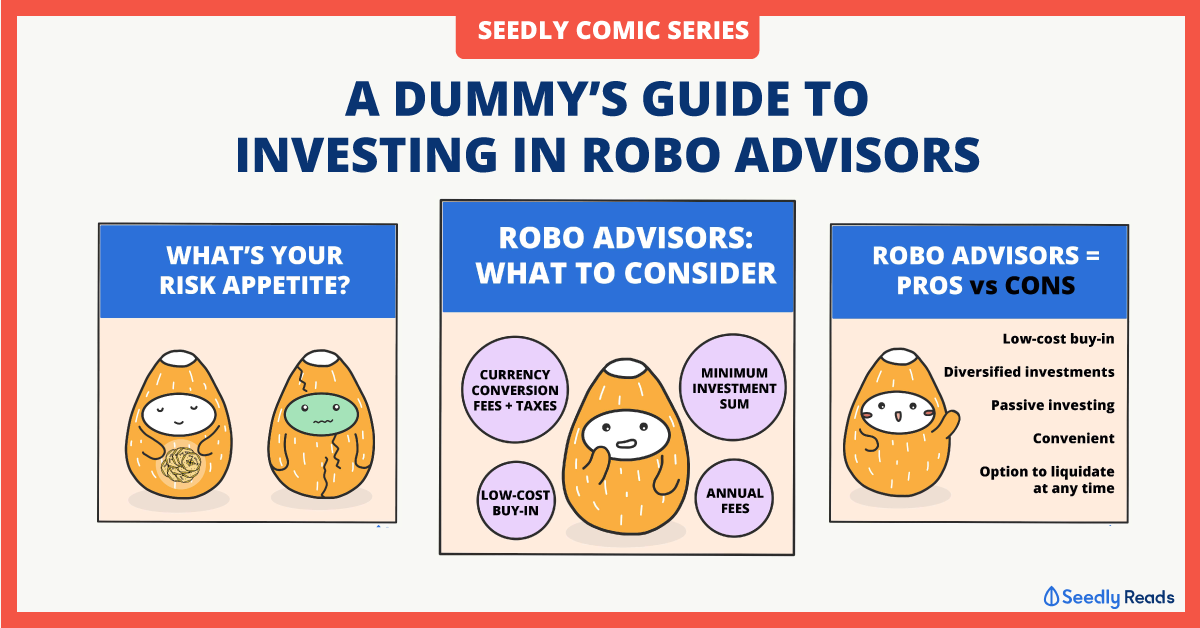

How can a person who is uninitiated in investing start investing with these robo-advisors? What is the catch behind them and what are the risks?

I'm totally new to investing and I so I'm looking for something more passive. Don't see myself trading stocks. Hence I was more interested in starting with Robo-advisors. What are the pros and cons when investing in Robo- advisors?

3

Discussion (3)

Learn how to style your text

Reply

Save

Hi Anonymous!

To answer your question, I think that most robo-advisors do the job of assessing your current financial position and recommend a portfolio strategy after reviewing your risk profile. As for the "catch", I would say that robo-advisors are still not very different from your ordinary financial advisors as both options will still have a management fee incurred for users. The difference lies with the amount, as robo-advisors have lower management fees. You can check out Kristal.AI (https://solutions.kristal.ai/seedlypost) as they have no management fees for investment amounts lower than $50 000.

Practically speaking, robo-advisors replace that human element that traditional financial consultants would provide with an AI system. Depending on your preference, that may or may not be a disadvantage/con for you. There are also a plethora of robo-advisors and some do not rely solely on AI/technological capabilities and retain the human element (see Kristal.AI).

Hope that answers your query!

Reply

Save

Chuin Ting Weber

30 Apr 2019

CEO and CIO at MoneyOwl

Hi Anonymous,

Thank you for your questions. This is Chuin Ting, CEO/CIO of MoneyOwl. Perhaps as a p...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1297 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

662 Reviews

AutoWealth

4.7

223 Reviews

Related Posts

Advertisement

Pros:

Use my referral code and save on robo-advisor management fees (Have you started investing with StashAway yet? Sign up with my link and we'll both get up to $10,000 SGD managed for free for 6 months! https://www.stashaway.sg/referrals/vinasp2m)

The management fees for stashaway is 0.8% (https://www.stashaway.sg/faq/115003861428-what-...), much lower than $10 per buy/sell transaction on trading platforms like FSMOne.

The portfolio is quite diversified so you get to invest in etfs of many countries (like US, China), as well as bonds, commodities and tech etfs etc.

You also get regular dividends from the stashaway etfs and the system automatically reinvests any dividends you may earn

Easy to deposit and withdraw, with no charge

Cons:

Just like with any investment, there is a risk of losing all

Returns from robo-advisor etf is more slow and steady (it is an etf afterall so it is more diversified), so it might not be as fantastic as picking a good stock and profiting high returns in a short span of time (provided you managed to safely pick a good stock ;p)