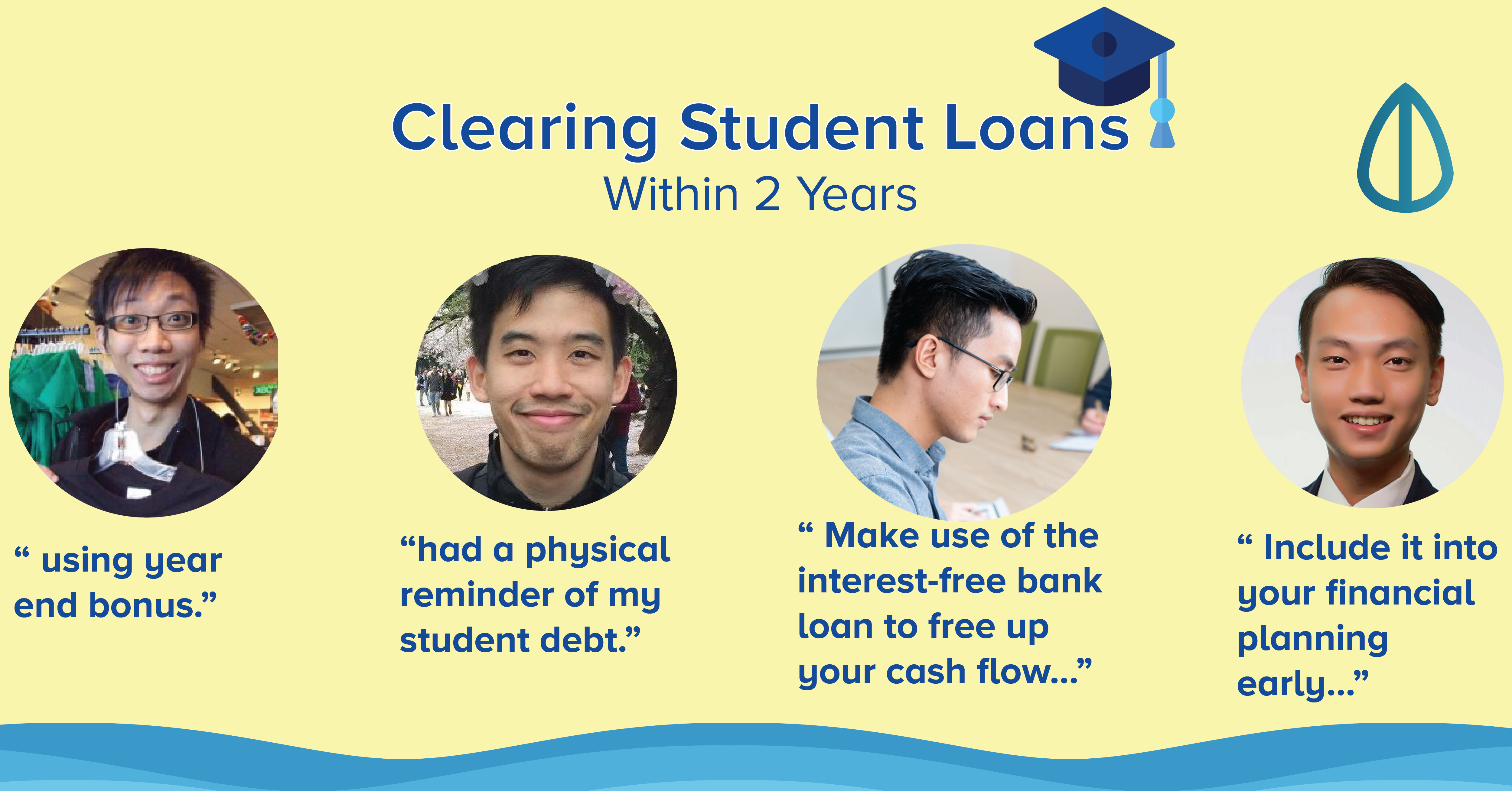

Firstly, we need to have a complete understanding on our cashflow. Through this process, we will understand our earning ability and spending habit. Here is a guide to help you: https://www.blog.pzl.sg/understanding-your-pers...

Next, create a detailed tracking for both of the loans and understand which will result in a greater repayment over time, i.e. higher effective interest.

Thereafter, create a budget that is capable of helping you to plan for the future. The best way to do this is via automation and this is how I do mine: https://www.blog.pzl.sg/how-to-create-a-monthly...

The objective of your budget will be to clear the loan with the higher effective interest as soon as possible while maintaining the repayment for the other loan. At the same time, restrict yourself from taking up further loans or any form of debt facility.

Always go back to your cashflow and budgetting to ensure that you maintain at least the same level of surplus every month (use the budget article to help you enforce greater discipline).

Finally, yes - you should build up your rainy day funds at the same time. This will act as a safety net in case of an emergency. The last thing that you want is to be left with nothing and two debts to repay. Therefore, always have a safety net in place.

While we focus on your debt management, I will like to take this opportunity to highlight the importance on insurance coverage for yourself. While this may seem unnecessary because the focus is on loan repayment, the focus is still on you as mentioned earlier - without you as the engine to generate income, you will be left with debts. Therefore, ensure that you have the right insurance coverage. To this end, one of the most important things to do is to have a complete understanding of your existing insurance portfolio. Through this process, it allows us to understand the coverage that we have, any financial gap, as well as to find out whether we are overpaying for our insurance policies. I have highlighted the rest of the reasons here: https://www.blog.pzl.sg/why-every-client-needs-...

All things considered, do proper tracking and devise a plan that is capable to help you overcome this situation.

Here is everything about me and what I do best.

Firstly, we need to have a complete understanding on our cashflow. Through this process, we will understand our earning ability and spending habit. Here is a guide to help you: https://www.blog.pzl.sg/understanding-your-pers...

Next, create a detailed tracking for both of the loans and understand which will result in a greater repayment over time, i.e. higher effective interest.

Thereafter, create a budget that is capable of helping you to plan for the future. The best way to do this is via automation and this is how I do mine: https://www.blog.pzl.sg/how-to-create-a-monthly...

The objective of your budget will be to clear the loan with the higher effective interest as soon as possible while maintaining the repayment for the other loan. At the same time, restrict yourself from taking up further loans or any form of debt facility.

Always go back to your cashflow and budgetting to ensure that you maintain at least the same level of surplus every month (use the budget article to help you enforce greater discipline).

Finally, yes - you should build up your rainy day funds at the same time. This will act as a safety net in case of an emergency. The last thing that you want is to be left with nothing and two debts to repay. Therefore, always have a safety net in place.

While we focus on your debt management, I will like to take this opportunity to highlight the importance on insurance coverage for yourself. While this may seem unnecessary because the focus is on loan repayment, the focus is still on you as mentioned earlier - without you as the engine to generate income, you will be left with debts. Therefore, ensure that you have the right insurance coverage. To this end, one of the most important things to do is to have a complete understanding of your existing insurance portfolio. Through this process, it allows us to understand the coverage that we have, any financial gap, as well as to find out whether we are overpaying for our insurance policies. I have highlighted the rest of the reasons here: https://www.blog.pzl.sg/why-every-client-needs-...

All things considered, do proper tracking and devise a plan that is capable to help you overcome this situation.

Here is everything about me and what I do best.