As of now, Aug 2020, it's still relatively early days as the MAS full digital banking licences are still in processing phase...

But with some experience studying this market for awhile now, I can hazard some quick guesses and a simple framework as to what many of these digital banks are thinking of.

What is interesting is that all the various banking players are going after the retail mass market consumer space already with some form of installed & retained userbase.

In Singtel and GRAB collaboration case, it's clear from a telco and everyday point of use.

In Razer's case its about gaming community.

In SEA's case is from the shopping and eCommerce/gaming community with Shopee and Garena.

All in all, I do believe that it's a 'land-and-expand' Beach head strategy which will ultimately serve a larger wider market for all consumers.

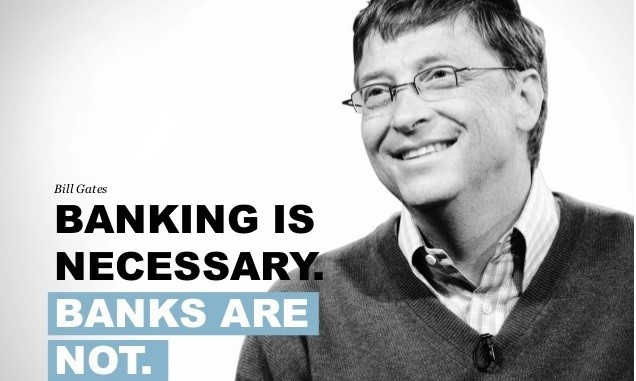

There's also a famous saying by Bill Gates about 5+ years ago when this whole Digital Banking and FinTech thing was getting started..

Key Steps and core components of Banking remain the same:

Somewhere to store your savings, deposits (CASA) maybe as a stored value facility first.

Some method to spend (Debit card first)

Some way to transfer money (Domestic or International,Multicurrency)

Some credit decisioning model/framework (this will unlock the next level of banking, where you can start to loan, do credit cards, and earn from interest revenue)

Perhaps even adding other layers to unlock other forms of personal finance and Insurance will definitely be a big one (moving from General insurance, eg Travel, home, car insurance and finally to Life insurance this is the big one that everyone will want to go after because of the predicatbility in revenues)

Another exciting layer which GRAB has recently done as well is with the Bento acquisition for the investment layer, a strong and easy way to hook people in. People in Singapore love to either spend money or invest to make money work for them.

With the above core pillars, that's my simple idea of breaking down how I think this landscape may change and evovle as we go overtime.

And with a better UIUX on the front end and a lighter, more efficient back-end with little to no legacy of old banking tech, the sky's the limit for these new Digital banks.

So exciting!

As of now, Aug 2020, it's still relatively early days as the MAS full digital banking licences are still in processing phase...

But with some experience studying this market for awhile now, I can hazard some quick guesses and a simple framework as to what many of these digital banks are thinking of.

What is interesting is that all the various banking players are going after the retail mass market consumer space already with some form of installed & retained userbase.

In Singtel and GRAB collaboration case, it's clear from a telco and everyday point of use.

In Razer's case its about gaming community.

In SEA's case is from the shopping and eCommerce/gaming community with Shopee and Garena.

All in all, I do believe that it's a 'land-and-expand' Beach head strategy which will ultimately serve a larger wider market for all consumers.

There's also a famous saying by Bill Gates about 5+ years ago when this whole Digital Banking and FinTech thing was getting started..

Key Steps and core components of Banking remain the same:

Somewhere to store your savings, deposits (CASA) maybe as a stored value facility first.

Some method to spend (Debit card first)

Some way to transfer money (Domestic or International,Multicurrency)

Some credit decisioning model/framework (this will unlock the next level of banking, where you can start to loan, do credit cards, and earn from interest revenue)

Perhaps even adding other layers to unlock other forms of personal finance and Insurance will definitely be a big one (moving from General insurance, eg Travel, home, car insurance and finally to Life insurance this is the big one that everyone will want to go after because of the predicatbility in revenues)

Another exciting layer which GRAB has recently done as well is with the Bento acquisition for the investment layer, a strong and easy way to hook people in. People in Singapore love to either spend money or invest to make money work for them.

With the above core pillars, that's my simple idea of breaking down how I think this landscape may change and evovle as we go overtime.

And with a better UIUX on the front end and a lighter, more efficient back-end with little to no legacy of old banking tech, the sky's the limit for these new Digital banks.

So exciting!