Advertisement

Anonymous

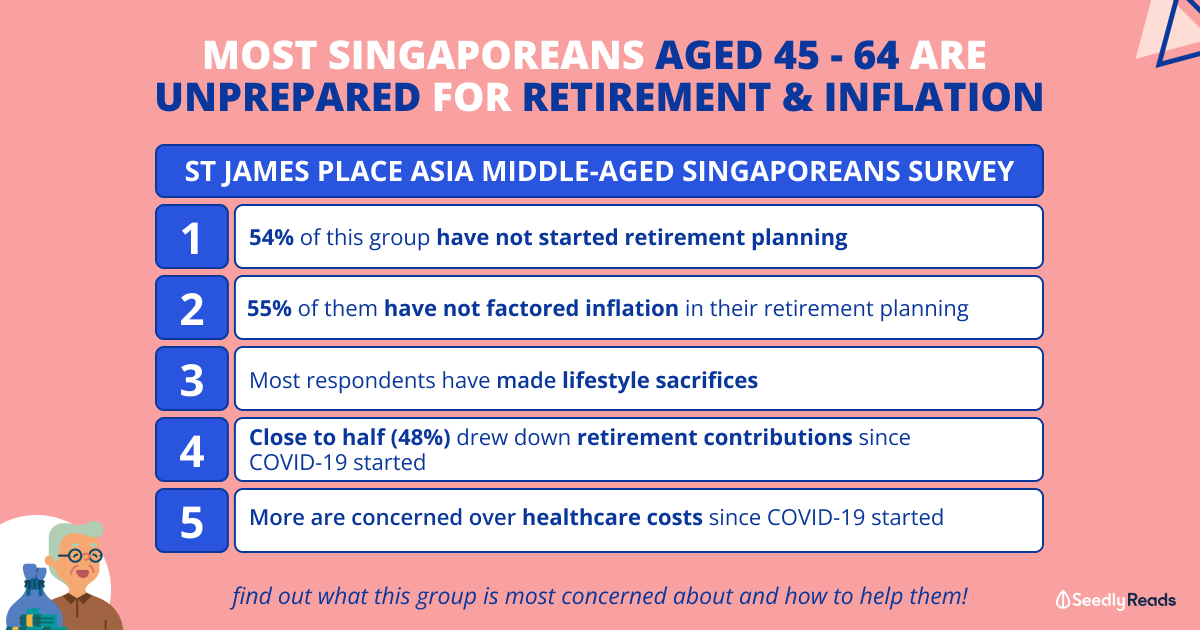

When to start planning for retirement? What to take into considerations when planning?

Is there any tools that help with retirement planning?

6

Discussion (6)

Learn how to style your text

Reply

Save

Elijah Lee

04 Mar 2022

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon,

There really isn't any specific time to plan for retirement, rather than a specific action that one takes at a certain point in time, I see retirement planning as a continuous process that gets refined as one either gets closer to retirement, or as one's needs and expectations about retirement changes.

Retirement is about income, not assets. You can have all the 'assets' in the world but if they do not produce income for you, your assets are of little use to you in retirement. This is essentially a balancing game of cash inflows and cash outflows.

You'll want to understand your expenses first.For example, how much are you spending on a month to month basis? This largely boils down to your lifestyle, which depends on what you expect in retirement. A simple lifestyle with the occasional treat or holiday will almost always mean that your retirement funds can last longer, something more extravagant may mean that you may run the risk of running dry in your final years.

Your cash outflows must also include things like your medical insurance premiums, mortgage, etc (if any). Once you have this number, that'll be valid for this year and perhaps the next 2 years, but over the long run, whatever number you have, you'll have to increase it to account for inflation.

The next step would be to look at your income generating assets. There's no way anyone can retire if they do not have income (passive or otherwise). Thus a $1million condo doesn't help one retire unless it's monetized (by renting it out), in fact, I would consider it a liability if you have to pay your mortgage and maintainence fees.

Look at your net worth, and see what assets you have that generate income. This can come from many sources, such as stocks, bonds, unit trusts, CPF, retirement plans, etc. You'll want to reasonably estimate what kind of income you can get from this, and on top of that, know when the income starts coming in (e.g. CPF LIFE may pay out $2K a month, but it's not much help if it only starts at 65, you need income to retire earlier than that, or you'll have to draw on your savings)

You'll want to build multiple layers of income; consisting of both guaranteed income and non-guaranteed income. Naturally if the entirety of your retirement income can be guaranteed, that is the best as you will have no worries, but it may be impractical to do so.

You'll want to then construct a "retirement cashflow timeline" which shows the expected inflows of income year to year and expected outflows, both accounted for inflation. This will then let you visualise if your income can last forever, if not, when do you need to start liquidating your riskier assets to sit on cash?

The key risks you will want to cater to includes:

- Longevity

- Health Risks

- Inflation

- Sequence of returns

- Market volatility

When you retire, look for income that is stable, inflation hedged, and with low volatility. To that end, I would recommend you create a 3-pronged retirement strategy, ensuring that

- You have a systematic withdrawal plan from your assets

- Proper segmentation of your assets into various buckets and layers

- Have a basic retirement income floor with guaranteed income solutions for the essentials.

The finer details of the recommendations (e.g. which areas to diversify to, which asset class) have to be tailored to your specific situation, as without sufficient details, I can only provide an overall picture of how retirement planning should be done.

Reply

Save

This retirement calculator is pretty good, helps...

Read 4 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Best to start as early as possible. retirement is never about old age. its about how much your income is more than your expenses. income can be active and best is passive and money come even your are sleeping. buy assets not liability. i plan 2 years ago and start my investment portfolio and returns every month about 75% PA passive positive cash flow that is 4x my expenses. i am 49yo and retired in apr 2021 after company ask to go in the mid of the covid pandemic. So do it as early as possible and start anything bette than think and talk and never do anything at all.