Advertisement

What's the best sequence for CPF tax relief? Medisave top up, CPF cash top up, SRS?

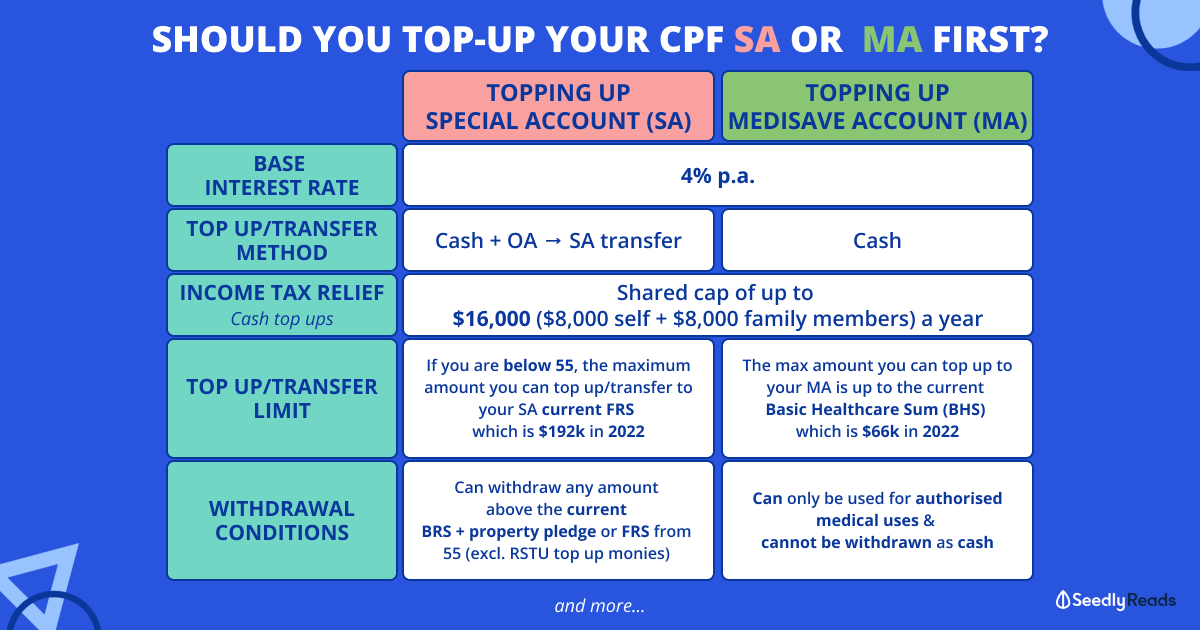

Hi, I am planning on tax relief for YA2021. I saw that there are 3 ways of top up for tax relief, ie. medisave top up, CPF cash top up (SA) and SRS.

While all have pros and cons, what's the best sequence?

It seems that top up to MA is better than SA, given that you can still withdraw for medical purpose & same interest rate as SA, as long as you don't hit the max tax relief ad BHS right? If MA is full, then go to SA?Thanks

7

Discussion (7)

Learn how to style your text

Jiayee

01 Nov 2020

Salaryman at some company

Reply

Save

Need to check what is your compulsory CPF contributions (both employee and employer) level first and what is the difference to the CPF Annual Limit. If the limit is not exceeded, you can contribute through all three.

For the tax relief portion, the tax relief amount per method is as below.

MA: Lowest voluntary contribution cash amount up to BHS or Annual CPF limit

SA: $7000 for cash top up to self/$7000 for cash top up to parents

SRS: Lowest amount of cash contribution up to the maximum SRS limit

In terms of targets, you could try to meet the BHS first if your MA is within reach. Once BHS is reached, the compulsory MA contributions will flow to your SA account. For more flexibility, you can do the SRS first as you can do early withdrawal subject to tax.

Otherwise you might need to consider other ways to reduce your tax bill.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Yes, if Medisave hits BHS, overflows go to SA.

Voluntary top-ups to Medisave are capped by CPF annual contribution limit of $37,740 - mandatory CPF contributions across 3 accounts. So if you've been contributing close to $37,000 already, you can't top-up much to your Medisave.

On the other hand, RSTU lets you top up your SA with annual tax relief cap of $7,000 when you top up your own SA and another $7,000 when you top up across your family members' SA.

SRS has an annual tax relief cap of $15,300 for citizens. For PRs and foreigners, you will need to check IRAS site (I only remember my own cap). Withdrawal before statutory retirement age (it's fixed once you first deposit money into SRS) incurs both income tax and additional penalty so you are discouraged from withdrawing so early.

But unlike CPF, you can withdraw as long as you accept the penalties. For CPF, you need to write in and get approvals due to family/medical reasons, etc. It's harder to get money out of CPF when you aren't old enough.

There's not much sequence to these. If you are already investing with robo-advisors and what not, feel free to contribute to SRS and invest your SRS monies via robo-advisors. If you can't stomach risks, consider topping up your CPF. Just be aware of the reduction of liquidity for both CPF and SRS.

Between Medisave and SA, I plan to top up Medisave first because I want my Medisave to sustain itself while paying for my hospital plan. SA top-ups via RSTU never see the light of day unless in the form of CPF LIFE annuities. That's 40 years away for me.