Advertisement

Anonymous

Should I only start topping up SRS only after maximising MA and SA? What are the considerations?

As I read through articles, it is more of MA or SA first, then SRS. Should I only start SRS after MA and SA are settled? What are the considerations?

2

Discussion (2)

Learn how to style your text

Nigel Tan

02 Nov 2021

Executive Senior Financial Planner at Great Eastern Life

Reply

Save

Elijah Lee

Edited 01 Nov 2021

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon,

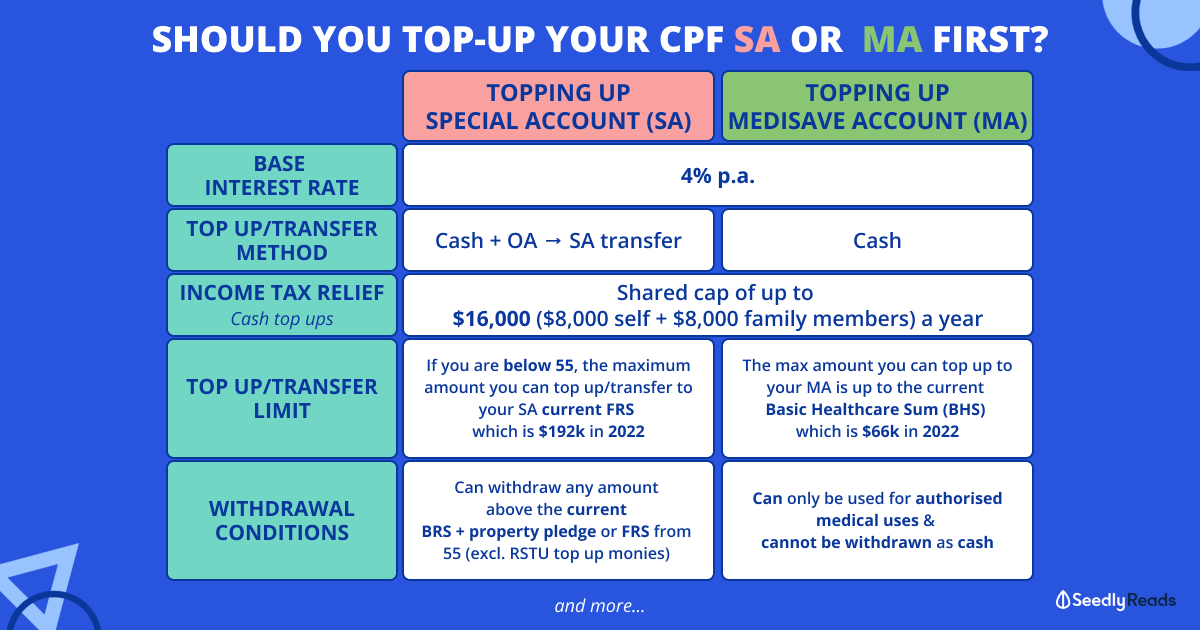

No, not necessarily. If you happen to be in a high enough tax bracket, there is nothing stopping you from doing both MA, SA and SRS contributions for the tax relief. However, if you are already in a very high income tax bracket, it is likely that you won't be able to perform a MA top up since you would hit the CPF annual limit from your wages alone. SA topups are independent of the CPF annual limit so you can always top up as long as you have not hit FRS.

I do know of people who do all 3 for the purpose of building their nest egg and saving tax and saving up for medical expenses at the same time. But you need to be aware that if you have contributed a lot to SRS, then when you withdraw later on after 62, you might have to pay some income tax. So you'll need to do your maths to see what works for you.

Then again, you could just focus on SA/MA topups first, and when that is no longer an option since you have hit the respective limits, you can start SRS top ups to continue to save tax. So your age also matters since it will be a lot easier to have over $400K in SRS if you start topping up from say, age 30.

The usual restrictions apply for the top ups, i.e. SRS maximum limit is $15300, SA top ups are capped at FRS, etc,.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hey Anon, based on what you shared I assume you're looking to top up these accounts for tax savings purposes.

Topping up your MA / SA has its benefits:

Guaranteed 4% interest by CPF board

Tax relief of up to $7k

Builds up funds in your Retirement Account created at 55 faster (excess of Retirement sum amounts may be withdrawn at 55)

(Topping up MA works only if you haven't reached the CPF contribution limit of $37,740; but topping up SA is a separate independent relief)

but it also has drawbacks:

Irreversible transfer, cannot be withdrawn unless for specific reasons

Limited by its uses: SA can only be used for retirement; MA can only be used for hospital bills / pregnancy related costs / health insurance / careshield or eldershield premiums

SRS is great if your annual income $80k or more.

The contribution limit is higher - $15,300 per year

You can invest the funds in the SRS accounts for potentially better returns.

Foreigners working in singapore who don't have CPF contributions can contribute up to $35,700 and withdraw after 10 years from first contribution.

Drawback:

Its a tax deferment rather than a write off, you'll need to pay 50% tax back when withdrawing from 62 years onwards

Withdrawing halfway will incur penalties & costs, but you still have the option to do so if you need it for an emergency.