Advertisement

Anonymous

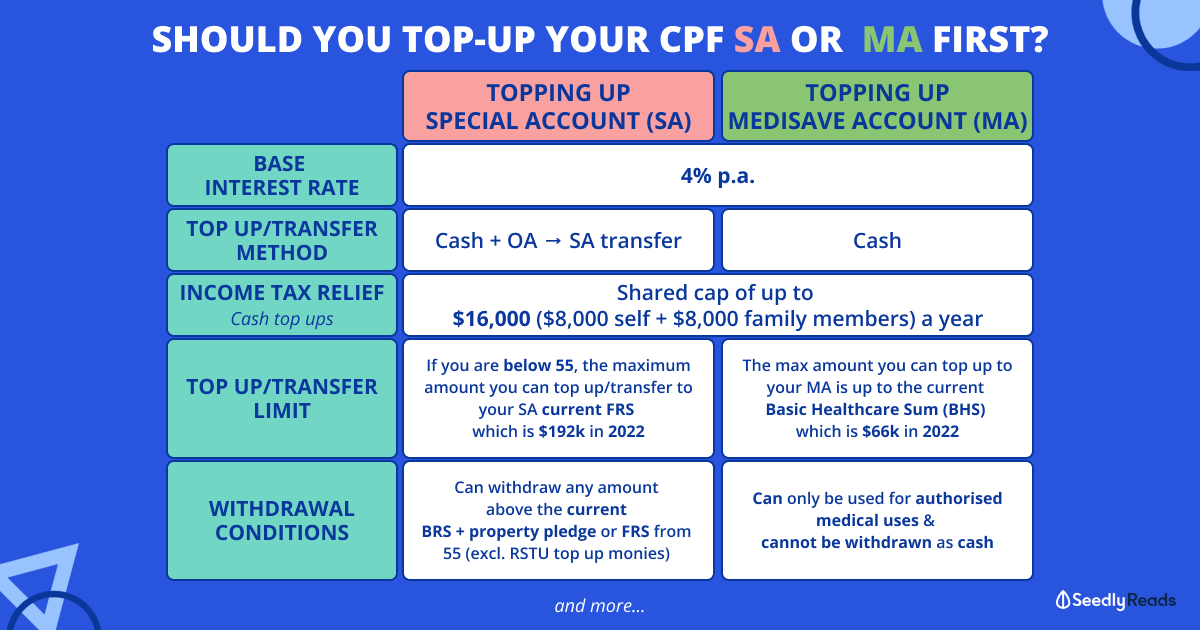

Should I be topping up my CPF as a fresh grad?

I am a fresh graduate with $2500 monthly salary, and I see all the posts regarding topping up your CPF to reduce/eliminate taxes and gaining from the interest rate. What should I do to make the most out of my time horizon? Should I top up $7000 to my CPF? Should I top up the OA or the SA? Thanks!

3

Discussion (3)

Learn how to style your text

Elijah Lee

24 Jan 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Mark Chan

24 Jan 2020

Business Manager at Amobee

Hi Anon!

Congratulations on embarking on the first step in taking charge of your retirement.

In assessing whether you should do a top-up (Voluntary Contribution) into your CPF, here are some notes and factors I would consider:

1. Liquidity

The first point I would like to flag here is that any contributions to your CPF are one-way. There is no way to withdraw the monies thereafter; even though you may use them for very specific applications (e.g. OA monies for Housing, MA for Medical treatments, etc). So please consider your current liquidity scenario before even thinking of topping up.

2. Current Cash & Cashflow

The next important point to note would be your current cash situation.

a. Have you paid off all outstanding loans/non-good debt? The interest charges from your loans (e.g. Credit Card debt / Student Loan) will erode any tax relief / interest yield from CPF.

b. Do you need the cash in the immediate future? You need to plan what the immediate milestones are for yourself. You may need the cash to get married (wedding banquets are expensive!), or place a downpayment for a home and also for renovation. Consider how much these costs, factor in your cash inflows, and consider whether you still have enough set aside for topping up into CPF.

Having said that, compound interest works wonders for you the earlier you start. So yes, if you have the factors above pinned down, I would definitely recommend topping up into your CPF-SA. (Do kindly note that you are eligible for tax relief only if you top up into your SA) You may consider topping up less than $7,000 in the first year of your working considering that $7,000 is more than 20% of your total income earned in the first year.

Hope this helps!

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi anon,

With a $2500 monthly salary, your focus should be on growing your human capital. Aim to increase your salary rapidly in the early years. At a $30K p.a. salary, your tax is quite negligible, literally $80/yr. Sacrificing $7000 to top up SA will not save you much in terms of tax, and it is a one way journey for those funds.

Start by building an emergency fund first to cover 6, and then 12 months of expenses, and paying off any study loans. At the same time, get Critical Illness and Hospitalization insurance to mitigate risk. I would only top up SA for tax relief if I'm projected to be in the 7% tax bracket and above, and I am totally comfortable with the money being locked away pretty much till retirement.

You can't top up OA directly, it has to be via 3-account contribution. What you can do is to do OA to SA transfer if you have no short term (i.e., in the next 3-5 years) plans to get a house and pay the downpayment with OA money. This helps your SA compound faster. Once a house is on the horizon, do your maths and stop transferring OA to SA.