Advertisement

Anonymous

I'm a working adult in my 30s and have never owned a credit card. I now realise the usefulness and benefits and would like to take the first step. Can anyone recommend 2 cards and why?

6

Discussion (6)

Learn how to style your text

Reply

Save

Maybe you can check on the different savings account available and check which one suits you best (there's a seedly savings account calculator for that), as some will require you use their bank's credit cards to hit a certain limit a month for higher interest rate.

Reply

Save

If you haven't been focusing on this area for the past 10 years, my guess is that you're not too keen in tracking rewards and requirements.

Keeping thing simple if you're lazy to have the 'depends on your needs and spending talk', pick a card which pairs with your high yield savings account, and another hassle free card which is brainless and doesn't require tracking.

Sure, there may be many other cards out there, but you'll have to be willing to pay some attention to your card spending strategy.

Otherwise, simplistically:

Credit card which pairs with your high yield savings account - UOB One, DBS Live Fresh, OCBC 365

Simple general cashback card - Citi Cash Back+ (1.6%), or Maybank FC Barcelona (1.6%)

Miles cards are sexy and everyone talks about them, but you are probably better off with cashback unless your default travel is with business class / optimising your strategy closely. Else, you're just being upsold and tricking yourself into believing you're getting a 'free' business class ticket.

Reply

Save

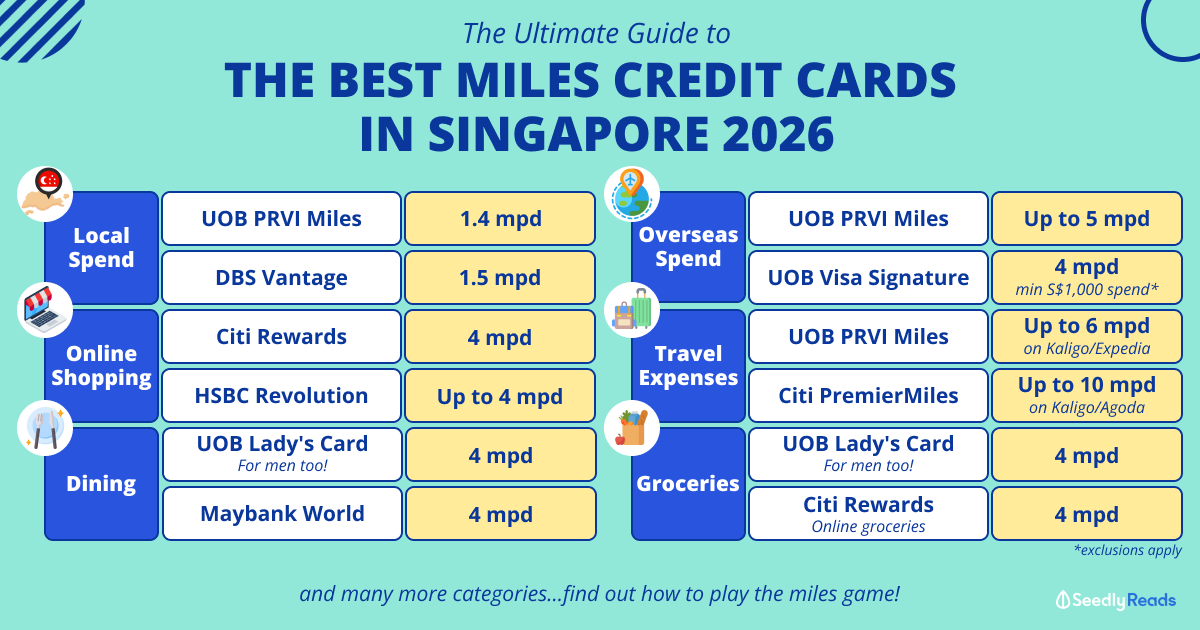

Personally I am more of a miles person, and my 2 favourite miles card are DBS Altitude and DBS WWMC.

DBS Altitiude offers 1.2mpd (in the form of DBS poins) for general spendings with no expiry date

DBS WWMC offers 4mpd (in the form of DBS points) for online spendings with 1 year validty

Personally I will transfer out my miles in DBS on a yearly basis since the points in my WWMC expires in a year, but it depends on my travel plans for that year.

In general, I would recommend miles if your spendings are not too low because it may take some time for you to accumualte miles if your spendings are low.

Also because I use DBS multiplier account, so have cards from DBS helps to get a higher interest rate for my bank account!

If your expediture is quite low and you are looking for cashback, you can consider citibank cashback+ for no miniminum spend and uncapped cashback. You can also consider SCB spree card for 2% cashback for mobile payment, contactless transcations and online spending with no minimum spend but a cap of $60 cashback a month. If you are looking to apply SCB spree card, singsaver currently has a promo where you can get free airpods with wireless charging case if you are applying through their site!

Reply

Save

Elijah Lee

21 May 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon,

There are two types of cards out there, those that reward cashback, and those that reward ...

Read 3 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

Standard Chartered Simply Cash Credit Card

4.1

176 Reviews

Standard Chartered Simply Cash Credit Card

Up to 1.5% on eligible spend

CASHBACK

Unlimited

CASHBACK CAP

$30,000

MINIMUM ANNUAL INCOME

UOB One Card

4.1

166 Reviews

DBS Altitude Visa Signature Card

4.3

98 Reviews

Related Posts

Advertisement

It's difficult to recommend because we have different spending habits and different cards will let you get more out of it. Personally, I would list down my usual spending to know what I am spending on and then move it from there.