Advertisement

Hi everyone. I'm 33 years old this year, I would wish to retire around 50 years old with $1.5 million, is it too ambitious? My monthly income is close to $5K and I can save half of my take home.?

I have about $200K in savings (mostly in FD, high yield savings account), ~$60K in my OA and SA combined. I do not have any dependents and my only liability is my housing loan which I'm servicing fully with my OA, til the age of 60.

I have only just started to invest with robo, stashaway global portfolio at 18% risk preference and syfe reits. What can I do to grow my portfolio? I'm looking at adding ETF but I'm not sure whether it will overlap with my SA portfolio?

Thank you!

14

Discussion (14)

Learn how to style your text

Reply

Save

So many people think 1 million is not enough to retire. Once I saved 1.5 million, I will buy a fund like Allianz income and growth which gives around 8% dividend which is almost 80k pa. Each month is around 6.6k dividend. 6k/mth is enough to retire for most folks out there.

Reply

Save

SGD1.5M savings can give u monthly SGD3.7k. Hope thats enuff for u to retire by 50.

Reply

Save

Great to see that you have a good retirement plan in mind.

i'm also striving to reach FI by 45.

Currently 29 yrs old.

Sadly i'm self-employed, no CPF and think it's worthless to put it in as there are a lot of restrictions in place.

So here's what i'll do if i were you.

I'll continue paying my Housing loan with CPF. Because my cash can be used to generate a high growth returns than the 2.5% growth in CPF.

I'll set aside 6 months worth of expenses in DBS Multiplier.

I'll also set aside any short term(1 yr) committments(Large amount) that i'll be going to spend aside.

Like Holiday, Insurance, income tax and medisave( For self employed)

Next i'll deploy the remainder into 2 tranche.

First will be lump sum.

Second will be DCA for the next 6-9 months.

For myself i do my own ETF investment.

Though i have 20% in my high growth stocks.

But my main 80% is in ETF.

For ETF, i don't time the market. Because it's kinda wasting time.

If you want to wait till it drop and buy also can. Like how it drops in the late Oct Period.

But why i don't time is because i don't know when the recovery will be.

Like what happened in Oct 2020 is that it drops for 3 weeks.

But it recover and Exceed the previous high in just 1 week.

So I'll lump sum in 50% of the allocated amount.

Then i'll DCA over 6-9 months depending on how comfortable you're with it.

When i first started, i only did 40 % Lump sum, 40% DCA and 20% Warchest.

But it seems like the 20% warchest is quite waste of time Because it always seems that i'll be buying higher than what i would have bought in the 40% Lump Sum tranche.

So example if 100k is what you have decided,

Then 50k in lump sum first

Remainder 50k split over 6-9 months.

Overlapping with SA is not so much of a concern for me.

Initially i had SA also. But i find the growth too slow.

So i went all in with my ETF.

My logic is that i think no point worrying about overlapping and stuff like that because my investment horizon will be 10 years - 15 years.

So doesn't matter to me.

I started this year Jan till Now.

Still buying in every month, week.

Hoping to FI by 45.

Reply

Save

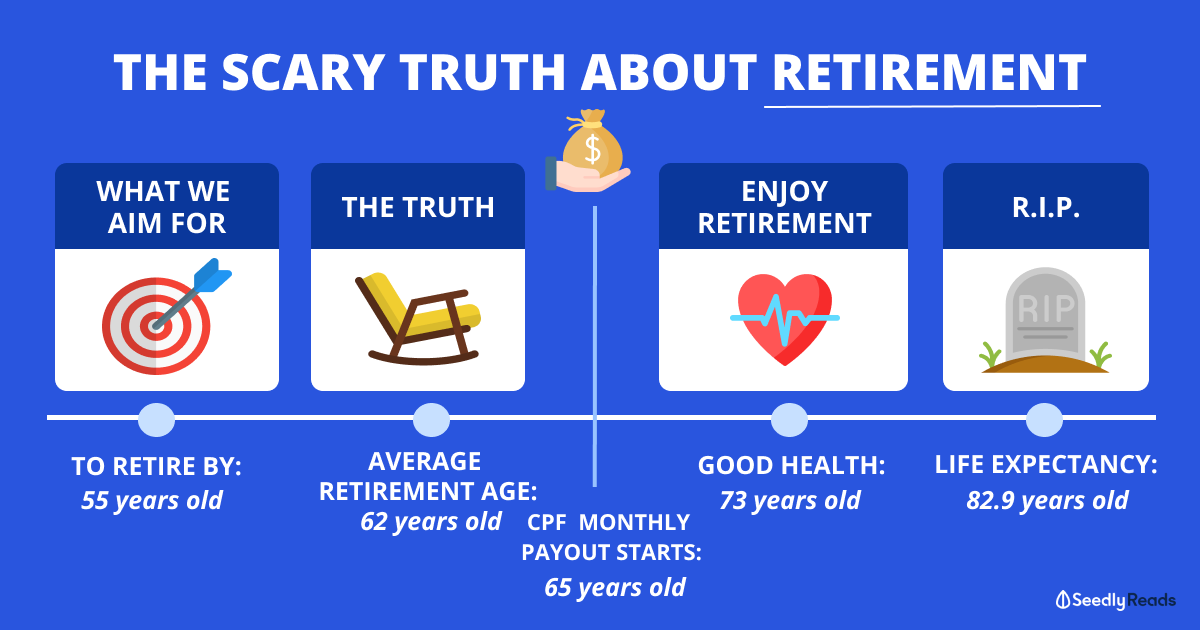

Is 1.5m enough for 30years...

Read 7 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1297 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

662 Reviews

Syfe

4.6

936 Reviews

Related Posts

Advertisement

From your story, i can see thet you have either little investment knowledge or low risk tolerance as you invested into low risk portfolios.

It's good that you have $200K cash savings even after purchasing a home.

It's possible to reach $1.5million in 20 years which is age 53.

But the issues are;

If want to reach that goal in shorter period, you need to start off with much more funds e.g $350/$400K.

That's why the banks target uncles & aunties for investment policies because they know this cateory of clients have at least $300K to $700K inside their banks. Haha=P

But they will be the ones who become richer instead of you. I have witnessed it myself as my loved ones are their "Cai Shen". Haha=P