Advertisement

Anonymous

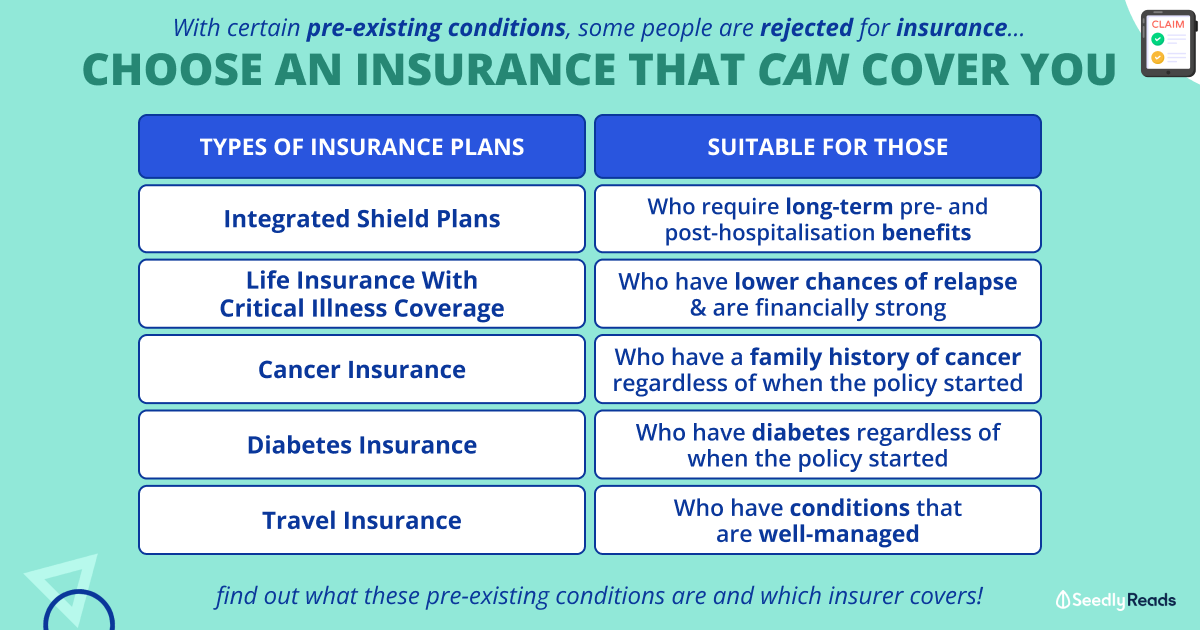

Health Insurance for foreigner with pre-existing condition

My partner is a foreigner holding a S pass and intends to get a health insurance. She was seeing a psychiatrist for work depression and has recently been off the meds. I have seen from forums/articles that it is generally difficult for people with history of depression to obtain health insurance despite doctors providing a written memo. Hence I am thinking of solutions for worst case scenarios.

Recently, I came across AXA Globalcare and it seems to have moratorium underwriting which can possibly cover her 'preexisting condition"? Is this true? Or are they any products that might suit her too? TIA!

2

Discussion (2)

Learn how to style your text

Elijah Lee

20 Jul 2021

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Read the brochure regarding AXA Globalcare, yes they do cover pre existing condition with some term and condition and there is also a limit to how much can be claimed.

If your main concern is still hospital bills, not limiting to psychiatric treatment, getting a health insurance will still make more sense economically. Some insurers might still accept the shield plan but would exclude psychiatric treatment.

If your concern is regarding pre existing condition, maybe would be good for you to look up for an agent working in AXA to understand it better.

I do know of an agent working for AXA, I can link you up with him if you don’t mind. :)

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

Income IncomeShield Integrated Shield Plan

4.4

305 Reviews

NTUC Income IncomeShield Integrated Shield Plan Preferred

$1,500,000

LIMIT PER POLICY YEAR

180 / 365 days

PRE & POST HOSPITAL

As Charged

OUTPATIENT BENEFITS

Private Hospital

WARD ENTITLEMENT

Raffles Shield Integrated Shield Plan

4.5

84 Reviews

AIA HealthShield Gold Max Integrated Shield Plan

4.2

20 Reviews

Related Posts

Advertisement

Hi anon,

Just note that Global Care only covers pre-existing condition provided that you meet certain criteria.

The first criteria is that to be fully covered for pre-existing conditions, you must be "Trouble Free for two consecutive years & two years of consecutive cover", i.e. you must have held the plan for 2 consecutive years and made no claims.

The definition of trouble free is as follows:

Trouble Free

When a Life Assured:

• has not had any medical opinion from a medical practitioner including general practitioners (GPs), specialists or alternative practitioner; and

• has not taken any medication (including over the counter drugs) or followed a special diet; and

• has not had any medical treatment; for the medical condition or any associated medical condition.

The second criteria to take note is that any claim within the first two years (or nine months, for plan A/B) will invalidate the trouble free status and you'll either end up with lower cover (Plan A/B) or no cover at all (in the case of plan C, D, E). So it is not as straightforward as you think. Your partner will need to have not consulted a doctor or receive any treatment for two consecutive years before anything can be paid out.

The other way is to try a local insurer but this will almost certainly have an outright decline or extensive exclusions.