Advertisement

Anonymous

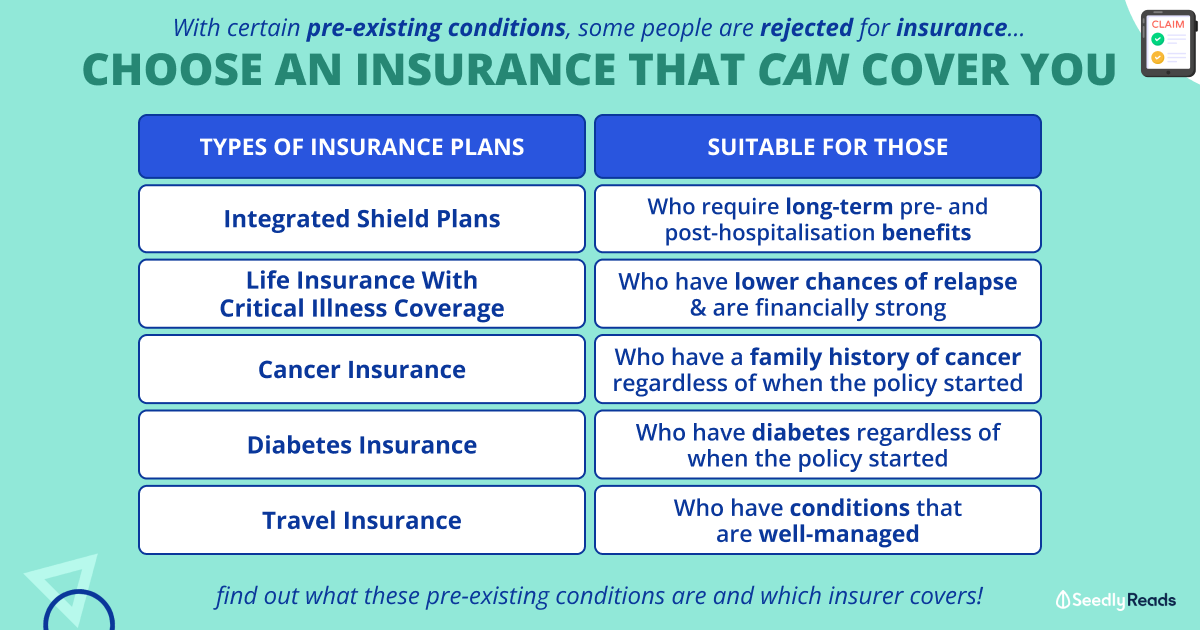

Can I get disability income insurance if I have pre-existing conditions?

3

Discussion (3)

Learn how to style your text

Elijah Lee

17 Jun 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

PolicyPal

17 Jun 2020

Official Account at PolicyPal

It depends on the specifics of your conditions but in general, you can. While some Disability Insurance Company will automatically disqualify you from coverage, there are some that continue to provide coverage.

If the pre-existing condition is on the excluded list, you will still be allowed to apply, but you would not receive coverage for that condition. Alternatively, if the pre-existing condition is covered, you might be charged a higher premium for the policy.

Essentially, it is key to disclose any pre-existing condition at the point of application. Insurers have the right to deny your claims if you are found to withdraw this information when applying for the policy.

Reply

Save

Pang Zhe Liang

17 Jun 2020

Lead of Research & Solutions at Havend Pte Ltd

It depends on the severity of your condition. Without knowing the details, there is no way for us to...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

Great Eastern GREAT CareShield

4.1

18 Reviews

$5,000

MAX MONTHLY BENEFIT

Unable to perform ≥ 1 ADL

MONTHLY PAYOUT CRITERIA

300% of first monthly benefit

MAX LUMP SUM PAYOUT

Unable to perform ≥ 1 ADL

LUMP SUM PAYOUT CRITERIA

Singlife Careshield Standard

4.3

3 Reviews

NTUC Income Care Secure CareShield

No rating yet

0 Reviews

Related Posts

Advertisement

Hi anon,

Disability income insurance is subject to medical underwriting and hence there is a possibility that any pre-existing conditions may lead to rejections or exclusions. So this really depends on what the condition is.

You might end up with exclusions, or loading, depending on the underwriting outcome. However, it is always better to declare any pre-existing conditions or else the insurer will have the rights to void the policy.