Advertisement

Anonymous

Background: 54 years old, still working, slightly over 1mil in combined savings. Owns HDB 4 room, looking to buy 2nd property for investment (or own stay in the future)?

Have 2 overseas properties amounting to approx $2mil sgd. No debt, no life insurance, daughter is financially independent and son is in uni on scholarship with plans to go overseas for masters approx 3 years later.

Should I empty our combined savings now for the a freehold property with approx ~100k in savings leftover? Do not wish to take a loan due to personal reasons and also do not wish to invest in stocks. Thanks in advance.

4

Discussion (4)

Learn how to style your text

Reply

Save

Teo See Hwa

12 Nov 2020

MArketing Associate at Propnex

Answer those in Bold

54 years old, still working

slightly over 1mil in combined savings (CPF or CASH)

Have 2 overseas properties amounting to approx SGF $2mil (Any rental income)

100k in savings leftover (CPF or CASH)

Do not wish to take a loan

Owns HDB 4 room (How many owner)

Do you know your next property purchase is BSD + 12% ABSD if you are the owner of HDB?

https://www.straitstimes.com/business/property/...

https://www.facebook.com/Teo.See.Hwa/posts/1022...

Reply

Save

Since you categorically stated no loans, and no interest in stocks, the only thing left to do with y...

Read 2 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

I'm a real estate agent myself.

But yet i won't pitch buying a 2nd property in Full Cash. Instead if i were you, i will work out my objective with this investment that you're thinking of.

If i'm at your age with not much worries in life, i'll start planning for my retirement.

And when it comes to retirement, i would want flexibility and not assets that illiquid. Property is an illiquid asset.

And it's not going to compound as much as other assets you could possibily put into.

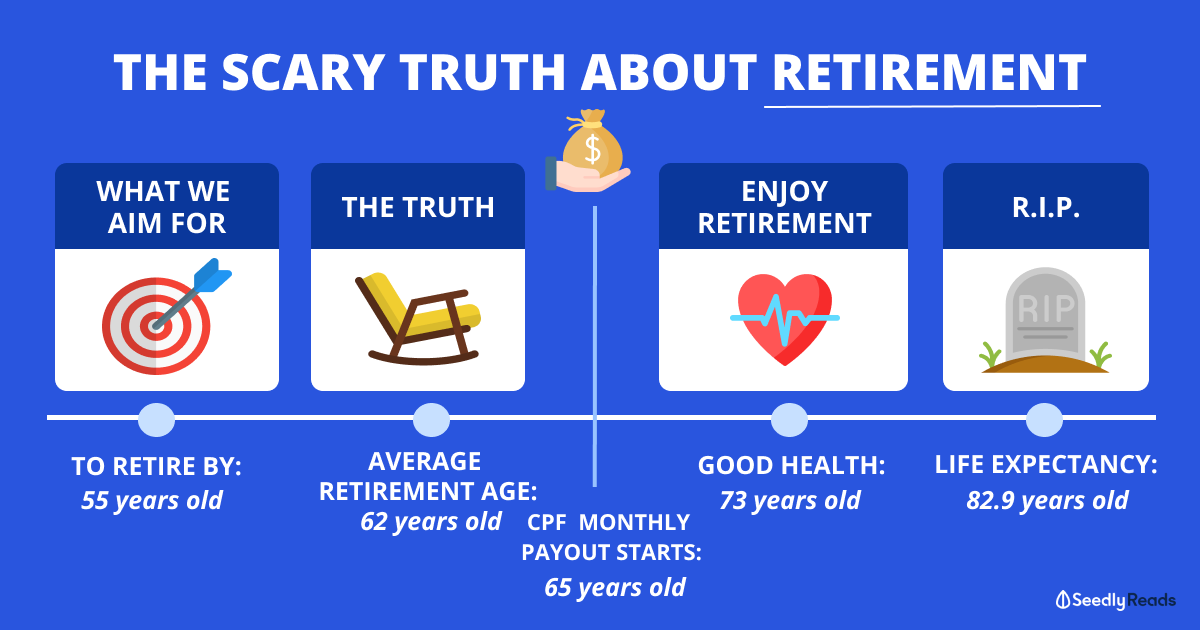

So first i'll work out on the appropriate expeneses that i would want to spend first when i reach my retirement age.

Supposedly it's going to be 65 yrs old at $50,000 for the next 30 years.

Means i have got 11 years to accumulate 1.5m. (Assuming complete withdrawal with no growth in capital)

Which is not tuff for you.

From 1m to 1.5m, what's the investment i need to do to reach that goal.

It means that i need to grow my asset at 3.75% CAGR minimally to reach that goal.

If i were to invest in a safe assets that looks at 50% bonds(BND) and 50% equity(VT), i should be able to grow my investment at a rate of 7.804%

Means my 20k will reach 48,804 in 11 years.

Therefore, my 1m will reach $2,440,200

With this 2.4m, i'm sure you're able to start your retirement of 1.5m even without neeeding to sell your entire FH property. yet still can sell at different batches depending on your needs. And still be able to pocket 900k for any "holiday retirement plans"

Just my 2cts thoughts...