Advertisement

Anonymous

Any recommended credit card for miles and cash back for uni fresh grad?

I have been using citi cc student version and realised that I can use the points to deduct for my previous transactions. Would it be better to go for citi or perhaps other bank? miles or any other ? how would u evaluate which credit card to get ? My monthly expenses would be around 600$ per month or lesser.

4

Discussion (4)

Learn how to style your text

Zac

05 Apr 2021

Noob at Idiots Invest

Reply

Save

thefrugalstudent

05 Apr 2021

Founder at thefrugalstudent.com

Hi Anon,

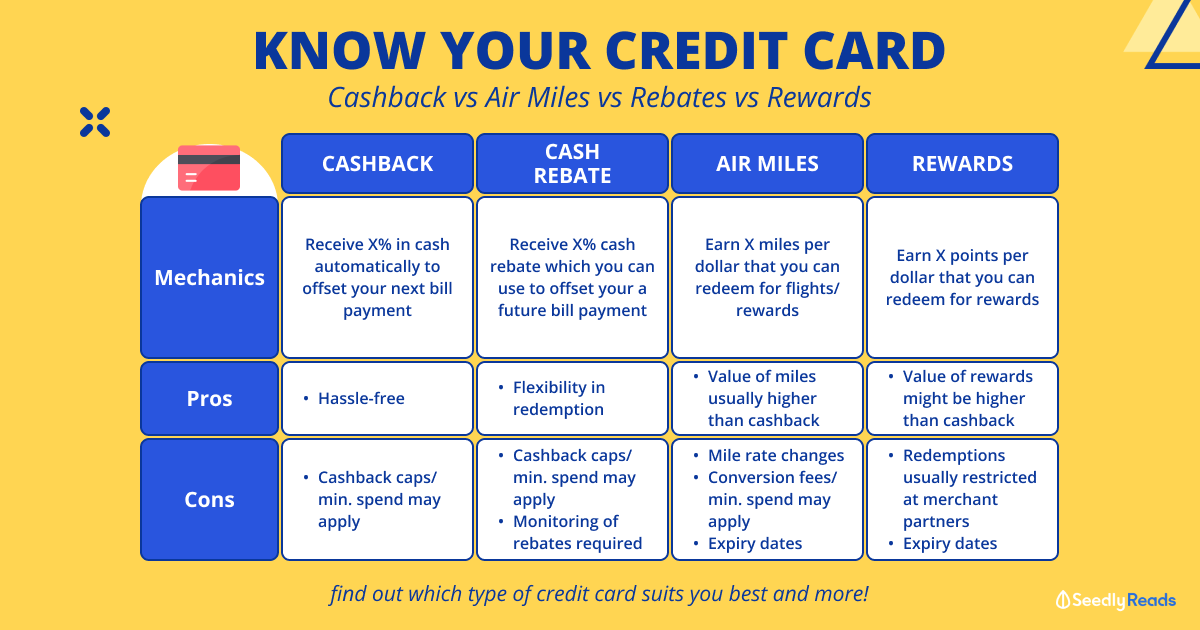

The question of miles vs cashback ultimately comes down to how much you value miles over cash. If you're someone who loves travelling and will want to experience luxurious travelling in the future (ie business class flights), miles will definitely be more worth it than cash. If you don't mind travelling without such luxuries, you may prefer cash instead. The reason for this distinction is that the usage of miles to redeem flights is generally not that worth it for regular economy class tickets, but more worth it for business class tickets and above. So if you don't see yourself caring much for business class flights, you may not value miles as much.

If you prefer miles, I'd recommend you to go with a 4 mpd rewards card over a regular miles card (~1.2 mpd). Such examples include HSBC Revolution, UOB PPV, and Citi Rewards. The difference in miles earn rate is huge and will allow you to earn miles a lot faster. Personally, I think HSBC Revolution is the best option because it charges a $0 annual fee and comes with free Entertainer promos, albeit with less variety than the regular Entertainer.

If you prefer cashback, then there are really many options out there. With a monthly spending of $600, you'd be eligible for several high cashback cards like DBS Live Fresh and OCBC FRANK. But you should re-evaluate your $600 spending to find out how much of it can be counted towards "eligible card spending", which is the criteria for such high cashback cards (ie if you have cash payments like hawker meals or non-eligible card payments like Grab top-ups/insurance payments, you may find it hard to actually be eligible for the cashback). In such cases, you should consider no-frills cashback cards like AMEX True Cashback, Citi Cashback+, or Standard Chartered Unlimited Cashback. You can also consider the rewards cards mentioned above because even though they are often associated with miles, they actually earn rewards points. These points can be exchanged for dining/shopping vouchers, which is basically cash for you to use.

Finally, before applying for a credit card, do lookout for any sign-up promotions. Banks and other financial entities (SingSaver, MoneySmart) tend to give rewards to new-to-bank customers which can be very attractive. On this note, you may want to check out this post to find out whether or not you should cancel your Citi Clear student card.

Hope this helps & all the best!

Regards,

thefrugalstudent

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

UOB One Card

4.2

168 Reviews

Get up to 10% cash rebate across 5 categories

CASHBACK

Up to 5% cash rebate on all other retail spend

ALL SPEND

Standard Chartered Simply Cash Credit Card

4.1

178 Reviews

DBS Altitude Visa Signature Card

4.3

99 Reviews

Related Posts

Advertisement

With relatively low monthly expenses of $600, I think the miles and cashback earned from your expenses won't justify the effort spent researching.

I suggest coming back to this when you've got a big ticket item on the cards - much easier to rack up spending that way if you're innately thrifty.