Advertisement

OPINIONS

Do You Need a Financial Advisor in Singapore?

If your finances are simple and disciplined, you may not need an advisor.

This post was originally posted on Planner Bee.

Wondering if you really need a financial advisor in Singapore?

Many Singaporeans pay hefty advisory or management fees each year, thinking professional help is always essential. In truth, not everyone needs one. If your finances are simple, your goals are clear, and you’re disciplined about saving and investing, you may be perfectly capable of managing your own money.

However, the idea of handling money alone can feel intimidating. With so many investment products, insurance plans, and online tools available such as robo-advisors, CPF calculators, and online brokerages, it’s natural to worry about making mistakes.

The good news? Today, technology and better financial education have made DIY financial management easier than ever. Let’s explore seven signs that show you could be ready to manage your finances independently.

1. Your finances are simple

If your financial life is straightforward, you may not need a full-time financial advisor. You’re likely in this category if you:

- Have a single income source and no side businesses.

- Own one property with a manageable mortgage.

- Manage only a few bank or investment accounts.

- Focus on basic goals such as building an emergency fund or saving for retirement.

When your money matters are simple, you can achieve strong results through budgeting, saving, and long-term investing. Advisors add the most value when finances involve multiple properties, business income, or complex tax structures.

2. You track and automate your finances well

Do you already use apps like DBS NAV Planner, OCBC Money Insights, or Seedly? If so, you’re already doing what many advisors help clients start doing. Automation helps you:

- Save regularly without thinking about it.

- Avoid missed bill payments.

- Track expenses and savings in real time.

If you’re consistent, tech-savvy, and review your finances monthly, you might not need a paid advisor. Just stay disciplined and update your plans annually.

Read more: Zero-Based Budgeting 101: How To Use It To Maximise Your Finances and Achieve Your Money Goals

3. You can build and rebalance a basic investment portfolio

Investing doesn’t have to be complicated. If you know how to build a diversified portfolio using ETFs or index funds, you can invest effectively without hiring a financial advisor. A balanced portfolio might include:

You can review and rebalance once or twice a year to maintain your desired asset allocation. Many Singaporeans also invest through CPF Investment Scheme (CPFIS) or Supplementary Retirement Scheme (SRS) accounts for long-term goals.

Low-cost, diversified portfolios often outperform actively managed funds over time, especially after accounting for management fees. The key challenge is behavioural, stay calm during market swings and focus on long-term growth instead of reacting to short-term news.

4. You are not overwhelmed by insurance jargons

Insurance documents can be difficult to navigate. There are many terms and jargon that can feel overwhelming at the beginning. If you’re comfortable researching and understanding these on your own, you may not need a financial advisor.

You can break insurance down into two main areas:

- Insurance to cover medical bills (e.g. MediShield Life, Integrated Shield Plans, personal accident plans)

- Insurance to replace income loss or higher daily expenses (e.g. term life insurance, critical illness plans)

Pro tip: __Review your coverage every two to three years, especially when life events change your needs. You can also use the Planner Bee insurance calculator to check if you’re adequately covered and find out what gaps you might need to fill.

5. You understand basic tax matters

Singapore’s tax system is simple compared to many countries. If your main income comes from employment and you don’t own rental properties or complex assets, handling your own tax filing can be straightforward.

The Inland Revenue Authority of Singapore (IRAS) pre-fills most income data for salaried employees through the Auto-Inclusion Scheme. Usually, all you need to do is log in, verify details, and submit your return, in under 15 minutes.

You can also claim deductions like:

- CPF contributions

- NSman relief

- Parent relief

- Course fee relief

If you earn freelance or side income, IRAS offers clear calculators and guidelines for accurate declarations. Since Singapore has no capital gains tax or inheritance tax, most working adults don’t need complex tax planning. The key is staying updated on policy changes via IRAS or official channels.

6. You stay calm when markets move

Good investing depends more on temperament than technical skill. If you remain calm when markets fall and don’t rush to buy during rallies, you already have a quality many investors lack.

Behavioural steadiness means:

- You stick to your investment plan.

- You don’t panic-sell during downturns.

- You ignore market noise and short-term speculation.

A written investment plan helps you stay focused on your time horizon and risk tolerance. Long-term investors prepare for volatility instead of trying to predict it, that’s the mindset that builds wealth over time.

7. You only need help with execution, not strategy

If you already understand your financial goals, know how to diversify, and use tools like Endowus, Syfe, or FSMOne, you may not need a traditional advisor. You’re clear about what to do, your challenge is staying consistent. You can set reminders to rebalance or review your portfolio yearly.

For motivation, join local finance communities like Seedly or The Fifth Person to exchange tips and stay accountable.

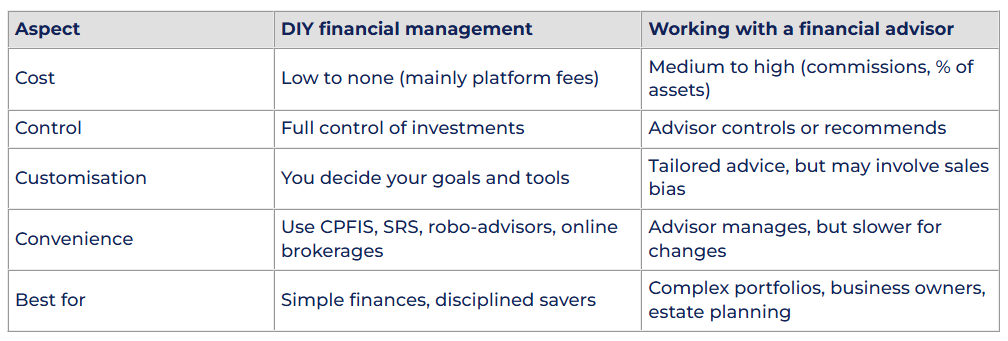

DIY vs financial advisor in Singapore

Read more: 5 Signs It’s Time To Break Up With Your Financial Advisor and How To Do It

Frequently asked questions

How much does a financial advisor cost in Singapore?

Most charge in three ways:

- Percentage of assets under management (AUM): Typically 0.5 to 1% per year.

- Flat or hourly fees: Usually S$150 to S$300 per hour.

- Commissions: Built into insurance or investment products.

Fee-only advisors are often more transparent since they don’t earn from product sales.

Is DIY investing through CPFIS or SRS enough?

Yes, for many people. Platforms like Endowus and FSMOne let you invest CPFIS or SRS funds in diversified portfolios. These tools are regulated by MAS and can suit long-term investors who prefer low fees and autonomy.

When should I hire a financial advisor?

You should consider professional advice if your finances become complex, such as when you start a business, manage large inheritances, or need estate planning or tax-efficient retirement strategies.

Final thoughts

Singapore offers plenty of ways to grow your wealth without paying steep advisory fees. As mentioned earlier, if your finances are simple, your goals are clear, and you’re confident using tools like CPFIS or robo-advisors, managing your own money can be both cost-effective and empowering.

But if your situation grows complex, don’t hesitate to seek independent, MAS-licensed financial advice. The key is to know when guidance adds value, and when you can confidently go it alone.

Comments

11

5

ABOUT ME

Your Personal Mobile Financial Advisor Application Join us at telegram! https://t.me/plannerbee

11

5

Advertisement

No comments yet.

Be the first to share your thoughts!