Advertisement

Anonymous

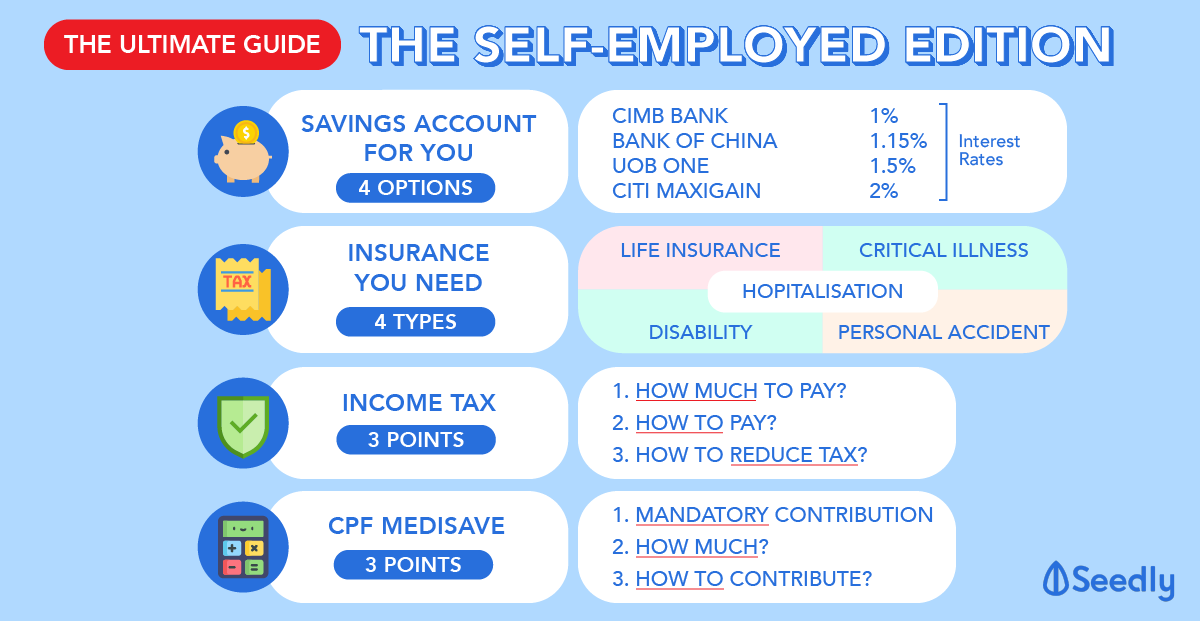

With the coming of year-end, it’s time to think about taxes. If today you’re self-employed and has $20k set aside for tax reduction purposes, which method would you do (more details in description)?

Which of the below method would you choose and why?

1. CPF voluntary contribution (Cap 37,740)

2. CPF Cash Top-up relief (7000 to SA account)

3. SRS contribution (15,300 Cap)

2

Discussion (2)

Learn how to style your text

JK

07 Jan 2021

Salaryman at Random Company

Reply

Save

Elijah Lee

07 Jan 2021

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon,

As a self employed, I did 2) first.

The reason is because I want CPF to be a safety net for my retirement. And since I am self employed and no one is going to contribute to my CPF other than me, I had better do something for myself. Of course, the tax relief helps as well.

Once that was done, then I did 1) up to the annual limit, for reasons similar to the above, just that I now take into account the fact that I would need money for a house downpayment, as well as to ensure that my MA has money for medical insurance and long term care insurance premiums.

Lastly, I would do 3), but I didn't do it this year. As I am still more than 20 years from 62, I'd prefer to leave SRS as another layer of tax relief when I no longer have the ability to do 1) due to reaching the FRS.

Thus, in your example, I'd just do $7K to 1) and then $13K to 2).

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi Anon,

Sorry that this came in late as we are already in 2021, but here's my opinion.

As a self-employed personnel, I feel that it is better for you to do SRS contribution. This is because you have a higher risk of running into income cashflow issues compared to salarymen. By contributing to your SRS, you will enjoy your tax relief, and should you require be able to liquidify it (at a penalty). This will allow you to have a safety net that you will be able to deploy s%!t happens, as compared to CPF where the funds are locked up until you use it to buy properties (OA) or when you hit retirement (SA).

Personally, as a salaryman at a company that did relatively well even during Covid's economy, I had top up $7k into my SA, as I feel that my income is stable, and because my CPF total is less than $60k while OA is almost at $20k. So this move was to allow me to take advantage of the 1% bonus interest for my CPF, earning me 5% interest instead of the usual 4% from SA.

Hope that this helps, even though it came in late. But that said, this is just my opinion, and consider your current situation to see which fits you best.