Advertisement

Anonymous

What do you think of investing in a second property in Singapore in current times?

Is it still worth it to go through the hassle of purchasing a second property in Singapore in current times - with stamp duty and rising interest rates. And limited capital appreciation. I know that in our parents' time, property investment is the way to go - or so it seems. But how about now? How does it compare to say, UT or insurance? Can someone enlighten me? Thanks!

3

Discussion (3)

Learn how to style your text

Cedric Jamie Soh

23 Nov 2019

Director at Seniorcare.com.sg

Reply

Save

Devanshi Singh

20 Feb 2019

Investment Planner, Writer, Adviser at Financial Advisory Services

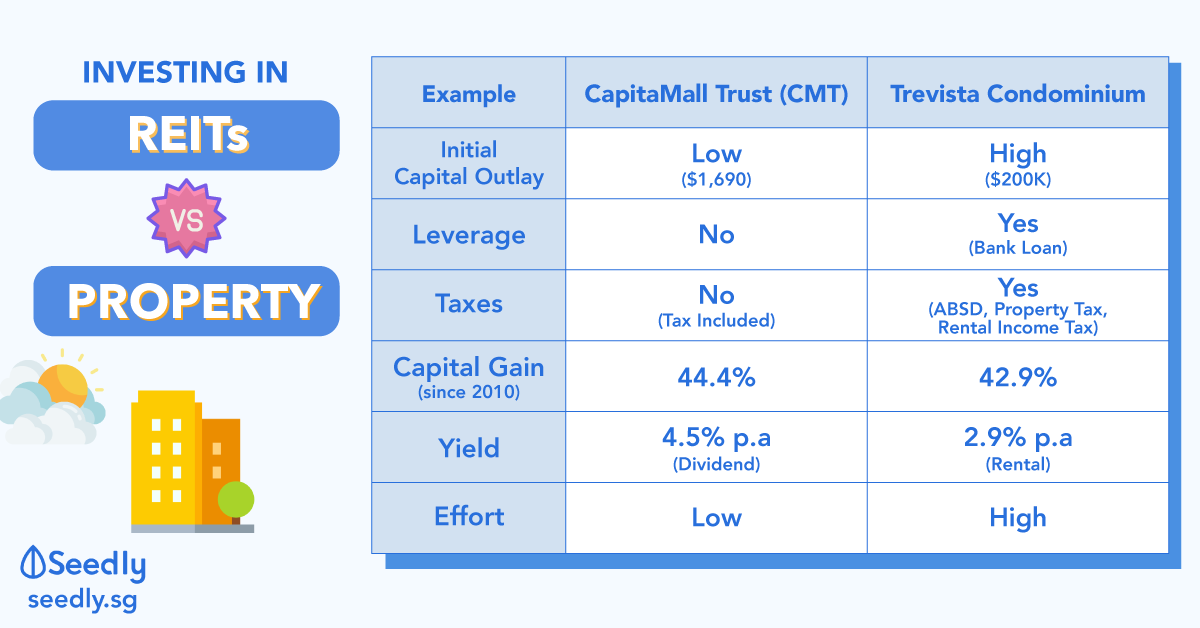

Property investment is always a smart choice for investment as by investing in property market you get theregular passive income source.

It is good that you are investing in property directly by buying the preoperty but there are other indirect way to invest in property i.e . Singapore REIT.

You migh be wondering it is even more hectiv to do all the study to find best Singappore REITs.

Well, it is not if you know the right source to guide you.

Reply

Save

Luke Ho

12 Jan 2019

Founder and Director at CFX Money Maverick Pte Ltd

Current times are currently in a pear shape for Singapore - we used to have a lot of opportunity and...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Definitely not a second residential property because the ABSD kills the profit. You lost 12% immediately when you buy a 2nd one?

And I will only buy old properties for the chance to enbloc.

Other than that, REITS is a terrific choice.

In the older days, our parents have no REITS, there is no way to get real estate in their portfolio other than outright buy a property.

We are luckier now, we have REITS and we can diversify from day 1.