Advertisement

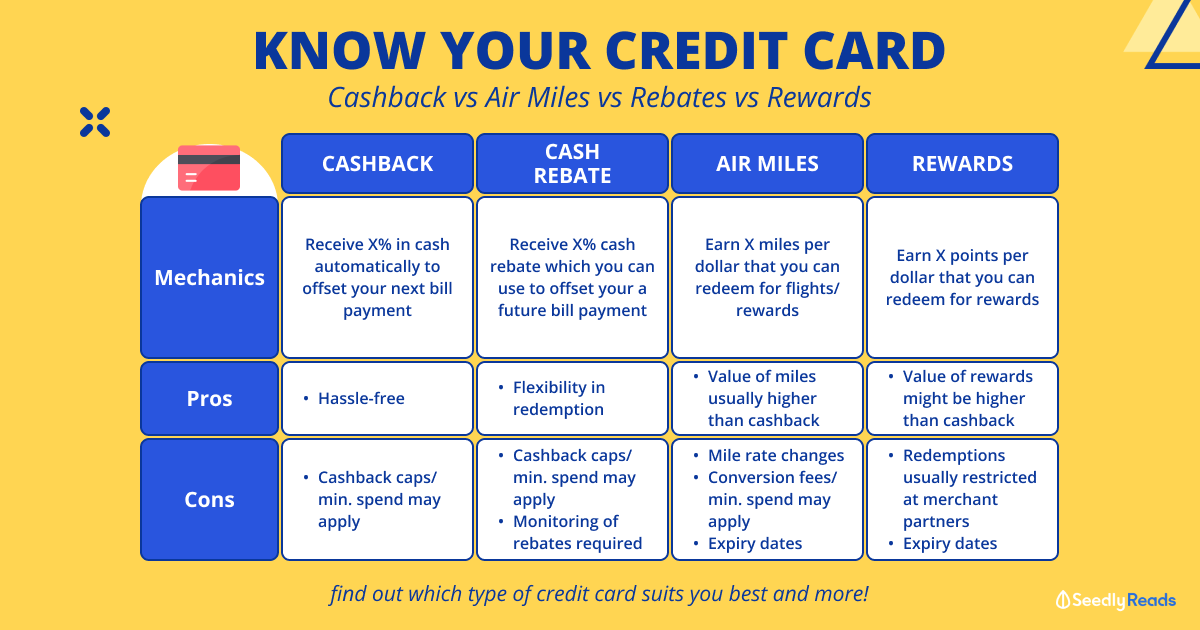

Thinking to get a credit card — Cashback or Miles? Currently, I am more geared towards miles but given the situation, I am conflicted. Any advice?

My reason for miles is to accumulate enough points for honeymoon trip down the years, 2 years to be exact.

10

Discussion (10)

Learn how to style your text

Reply

Save

Just Being Ernest

13 May 2020

Content Creator at www.youtube.com/c/JustBeingErnest

You can get back miles and cashback

looking at current situation, cashback would be ideal as it is liquid and mroe valuable now

I make videos about interesting stuff at youtube here

Reply

Save

I am team cashback based on my personality.

Perhaps this will help you to understand yours and ultimately decide: https://milelion.com/2019/12/22/is-it-worth-col...

Reply

Save

Elijah Lee

08 May 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi Zachary,

As someone who used miles for my honeymoon, I can tell you that if you wish to accumulate miles, you might as well do so now. Depending on the card you use, you may find that your miles earned and credited on the bank's side (in the form of points or whatever) have no expiry date (which is great), but even if they do have an expiry, transferring them to Krisflyer will extend your expiry by another 3 years.

You'll find that you will take time to accumulate miles. Even spending $2000/mth @ 4 mpd will only net you 96K miles a year, or 192K miles in 2 years, which is just enough to fly you and your wife to be in business class (if not, why are you in the miles game?) to Tokyo and back. If you were thinking of going further, you're out of luck and will have to fly economy. And that's assuming you manage to find award space available on SQ saver instead of the more expensive advantage rates.

So start now. There is no better time.

Reply

Save

Pang Zhe Liang

08 May 2020

Lead of Research & Solutions at Havend Pte Ltd

It depends on your needs and spending.

If you love travelling and don't mind delayed gratification,...

Read 36 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

UOB One Card

4.1

166 Reviews

Get up to 10% cash rebate across 5 categories

CASHBACK

Up to 5% cash rebate on all other retail spend

ALL SPEND

Standard Chartered Simply Cash Credit Card

4.1

176 Reviews

POSB Everyday Cashback Credit Card

3.9

199 Reviews

Related Posts

Advertisement

For myself, I go for cashback. More fuss free. Able to 'cashout' upfront.

For miles, you need to research more and calculate the conversion rate, and it differs from airline to airline. Unless you are going for business class, most likely the miles are not worth it. Furthermore, some miles may expire.

In short, the miles could possible 'earn' more but you need to play the miles game. Which is too troublesome for me thus I go for cashback.