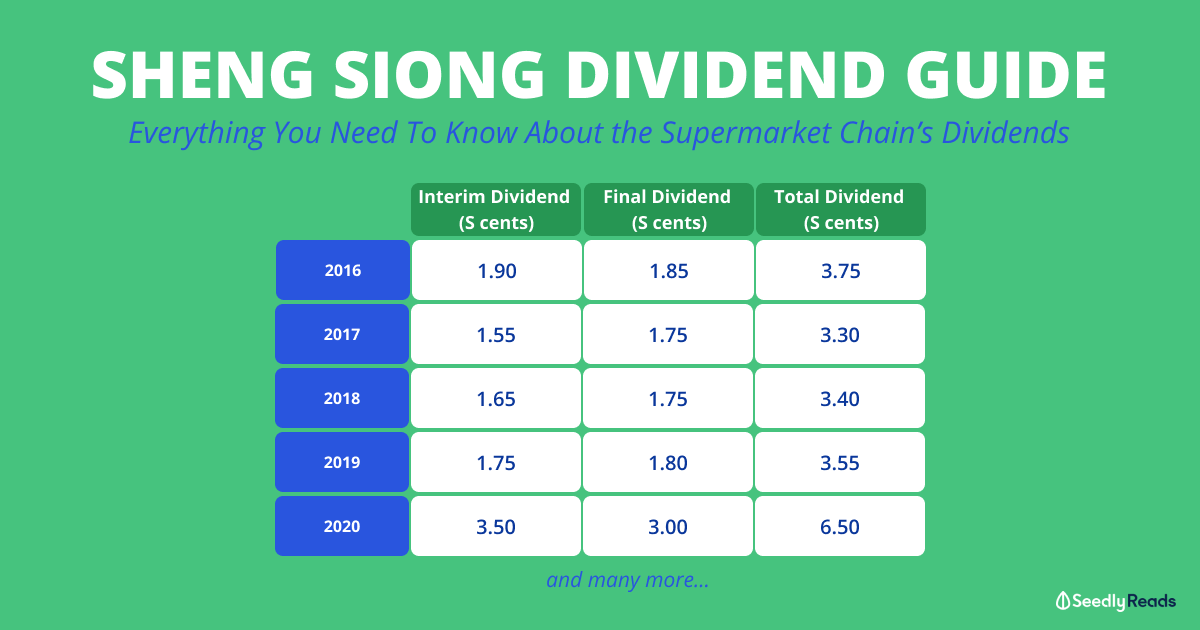

Ticker: SGX:BMT

Industry: Healthcare & Energy

Business Overview

New Silkroutes Group Limited, headquartered in Singapore, is an investment holding company that operates in the healthcare and energy sectors. Formerly known as Digiland International Limited, the company’s healthcare segment focuses on the provision of healthcare and related services in Singapore, Vietnam and China. The company’s energy segment focuses on physical oil trades in Asian markets. They are also engaged in providing services such as asset management, business management and investment consultancy.

Group Structure

Source: Annual Report 2018

- Healthsciences International Pte Ltd (HSI) owns and operates primary care medical and dental clinics in Singapore and Vietnam, as well as hospital development services and pharmacy management systems in Singapore and China. They also provide dental and medical supplies.

- International Energy Group Pte Ltd (IEG) trades oil and gas, produces power, and invests in strategic petrochemical assets.

Share Price Performance

Source: TradingView

For the last year, the share price of BMT declined by 17.19%. Over the last 5 years, BMT’s stock price has had mixed performance with respect to the STI.

Financials

New Silkroutes’ revenue grew by 59.9% in 2018, driven by the healthcare business and increase in oil trading activities. Net profit saw a further dip to US$2.961m, attributed to the expenses of newly acquired dental companies, and one-off expenses of writing off of receivables and professional fees for corporate exercises. If the one-off expenses were to be excluded, the Group would have improved in its performance and reduced its net loss to US$0.62m.

Current assets increased 9% mainly due to an increase in inventories, and cash and cash equivalents, while current liabilities rose 22% because of an increase in trade and other payables, and borrowings to finance oil trades. In 2018, the company also issued 25,394,048 more shares.

Moving forward, healthcare will be New Silkroutes’ core business. Therefore, the company has divested its non-core assets, such as its 30% stake in New Silkroutes Asset Management Pte Ltd in 2017.

Healthcare Segment

Acquisitions of dental clinics and dental supplies companies in 2017 contributed to a 10 times growth in healthcare segment revenue. In 2018, HSI entered Vietnam under the brand name ‘The Dental Hub International’ through a joint venture. To break into the Chinese market, the Group acquired Shanghai Fengwei Garment Accessory Co., Ltd, a manufacturer and distributor of fabric and products used in healthcare consumables. With rising demand for healthcare in China, a healthcare consumables business will definitely see growth.

However, the company’s acquisition of Shanghai Fengwei is a rather indirect route to enter the Chinese healthcare market. They also paid a hefty price tag of S$12.5m for it. Only time will tell if this acquisition pays off and increase profit margins.

The Group also looks to grow its healthcare segment organically in the future to balance their initial foray into healthcare which consisted of only acquisitions.

Energy Segment

For the energy segment, increased oil trading activities and logistics capacities helped to increase revenue by 1.6 times. The company altered their strategy to charter vessels instead of leasing fixed storage to be able to redeploy its vessels according to changes in market demands. This has helped to strengthen their shipping logistics capabilities, which will put them in a good position to come. However, financing costs remained high due to rising oil prices and stronger USD.

Just March this year, the Group sold its stake in IEG for US$10m in cash. The purchaser, TK Energy Limited, will make available a US$10m loan to New Silkroutes which will be deemed repaid in full when the sale is completed. This will strengthen the company’s earnings and financial position, streamline operations to focus on its healthcare segment, and enhance the long-term interests of shareholders.

Piotroski F-Score

For my analysis, I will be using the Piotroski F-Score. It assigns a number between 0-9 which is used to determine the strength of a company’s financial position. Comparing 2018 vs 2017, the criteria awarded with a point (1) means there was an improvement from the previous year and vice-versa (0).

New Silkroute was awarded a score of 1, which is bad. Current ratio fell from 1.43 to 1.27, but is still above 1 which means they are able to pay off their debt obligations. Gross margin ratio also dropped from 2017 to 2018. The company’s return on assets also dropped further, indicating that they have become more inefficient at using their assets to generate earnings. However, the Group has become efficient in using their assets to drive revenue as asset turnover increased.

Valuation

From the above figures, it seems that New Silkroutes is structurally fundamentally weak. Even though P/B ratio looks considerable fine, but P/E and P/S ratios prove my point. They also have negative returns on capital which suggests that the company is destroying its own value.

Conclusion

With the above analysis, the shares of New Silkroutes seam bearish. I do not see strong impetus that will create an economic moat for New Silkroute for the next couple of years. Current shareholders are hinging on the company’s efforts to refocus on the healthcare segment to deliver them returns. I would skip this stock as the company is fundamentally weak and does not have a good track record. Management has also not outlined a concrete plan or vision to develop the healthcare segment.

Hopefully, this foray into healthcare will not be another misadventure like their fund management that never panned out.

Ticker: SGX:BMT

Industry: Healthcare & Energy

Business Overview

New Silkroutes Group Limited, headquartered in Singapore, is an investment holding company that operates in the healthcare and energy sectors. Formerly known as Digiland International Limited, the company’s healthcare segment focuses on the provision of healthcare and related services in Singapore, Vietnam and China. The company’s energy segment focuses on physical oil trades in Asian markets. They are also engaged in providing services such as asset management, business management and investment consultancy.

Group Structure

Source: Annual Report 2018

Share Price Performance

Source: TradingView

For the last year, the share price of BMT declined by 17.19%. Over the last 5 years, BMT’s stock price has had mixed performance with respect to the STI.

Financials

New Silkroutes’ revenue grew by 59.9% in 2018, driven by the healthcare business and increase in oil trading activities. Net profit saw a further dip to US$2.961m, attributed to the expenses of newly acquired dental companies, and one-off expenses of writing off of receivables and professional fees for corporate exercises. If the one-off expenses were to be excluded, the Group would have improved in its performance and reduced its net loss to US$0.62m.

Current assets increased 9% mainly due to an increase in inventories, and cash and cash equivalents, while current liabilities rose 22% because of an increase in trade and other payables, and borrowings to finance oil trades. In 2018, the company also issued 25,394,048 more shares.

Moving forward, healthcare will be New Silkroutes’ core business. Therefore, the company has divested its non-core assets, such as its 30% stake in New Silkroutes Asset Management Pte Ltd in 2017.

Healthcare Segment

Acquisitions of dental clinics and dental supplies companies in 2017 contributed to a 10 times growth in healthcare segment revenue. In 2018, HSI entered Vietnam under the brand name ‘The Dental Hub International’ through a joint venture. To break into the Chinese market, the Group acquired Shanghai Fengwei Garment Accessory Co., Ltd, a manufacturer and distributor of fabric and products used in healthcare consumables. With rising demand for healthcare in China, a healthcare consumables business will definitely see growth.

However, the company’s acquisition of Shanghai Fengwei is a rather indirect route to enter the Chinese healthcare market. They also paid a hefty price tag of S$12.5m for it. Only time will tell if this acquisition pays off and increase profit margins.

The Group also looks to grow its healthcare segment organically in the future to balance their initial foray into healthcare which consisted of only acquisitions.

Energy Segment

For the energy segment, increased oil trading activities and logistics capacities helped to increase revenue by 1.6 times. The company altered their strategy to charter vessels instead of leasing fixed storage to be able to redeploy its vessels according to changes in market demands. This has helped to strengthen their shipping logistics capabilities, which will put them in a good position to come. However, financing costs remained high due to rising oil prices and stronger USD.

Just March this year, the Group sold its stake in IEG for US$10m in cash. The purchaser, TK Energy Limited, will make available a US$10m loan to New Silkroutes which will be deemed repaid in full when the sale is completed. This will strengthen the company’s earnings and financial position, streamline operations to focus on its healthcare segment, and enhance the long-term interests of shareholders.

Piotroski F-Score

For my analysis, I will be using the Piotroski F-Score. It assigns a number between 0-9 which is used to determine the strength of a company’s financial position. Comparing 2018 vs 2017, the criteria awarded with a point (1) means there was an improvement from the previous year and vice-versa (0).

New Silkroute was awarded a score of 1, which is bad. Current ratio fell from 1.43 to 1.27, but is still above 1 which means they are able to pay off their debt obligations. Gross margin ratio also dropped from 2017 to 2018. The company’s return on assets also dropped further, indicating that they have become more inefficient at using their assets to generate earnings. However, the Group has become efficient in using their assets to drive revenue as asset turnover increased.

Valuation

From the above figures, it seems that New Silkroutes is structurally fundamentally weak. Even though P/B ratio looks considerable fine, but P/E and P/S ratios prove my point. They also have negative returns on capital which suggests that the company is destroying its own value.

Conclusion

With the above analysis, the shares of New Silkroutes seam bearish. I do not see strong impetus that will create an economic moat for New Silkroute for the next couple of years. Current shareholders are hinging on the company’s efforts to refocus on the healthcare segment to deliver them returns. I would skip this stock as the company is fundamentally weak and does not have a good track record. Management has also not outlined a concrete plan or vision to develop the healthcare segment.

Hopefully, this foray into healthcare will not be another misadventure like their fund management that never panned out.