Advertisement

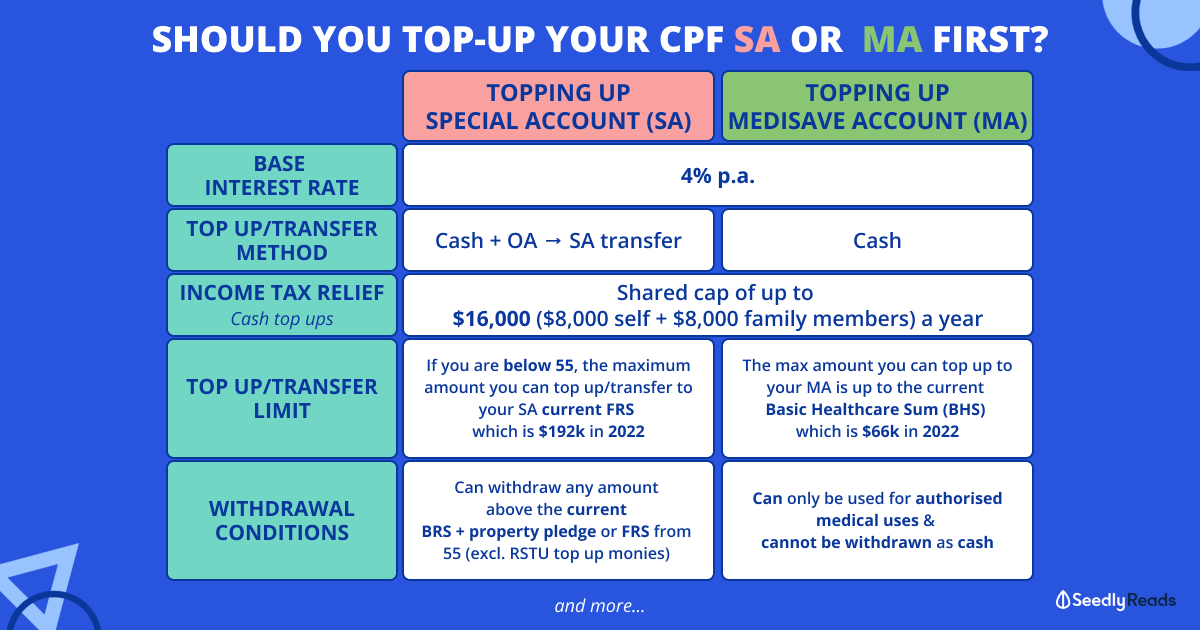

Should we top-up MA or SA?

Which one will be the most beneficial?

Considering that MA has many more uses and that SA is solely for retirement, which do you think would be good to top up and why? what are the pros and cons for both accounts and why would you prioritise topping up one over the other? should I focus on topping up one of the accounts or both?

17

Discussion (17)

Learn how to style your text

Wee Keat

31 May 2020

Tea Lover at Don't Tell You :P

Reply

Save

SA as it goes towards retirement.

Reply

Save

SA, high interest rate at the same time will go to your retirement fund later on. MA fr medical insurance n medical expenses. However, there is a cap on the amount u can withdraw yr MA fr hospitalisation insurance.

Reply

Save

Loo Cheng Chuan

20 Nov 2019

Founder at 1M65 Movement

SA for a simple reason. The interest earnings of SA stays in SA and compounds at 4-5%. The interest of MA, beyond the cap, which I think is S$60k now, will flow to SA, and if SA cap is reached, will go to OA, which yields only 2.5%.

Reply

Save

Pang Zhe Liang

19 Nov 2019

Lead of Research & Solutions at Havend Pte Ltd

The benefits really depends on your objective - for your medical expesnes or for your retirement?

...

Read 4 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Both SA and MA have the same interest rate at 4%. So it might seem like there isn't much of a difference to top-up either. However, one tiny difference that all the answers up till now have not mentioned is that it indirectly affects your withdrawal amount at age 55.

When you top-up your SA directly, the amount you put in will not be withdrawable at age 55. You must remember that your RA is created with the funds from both your OA and SA (and not MA).

"You may also withdraw your Retirement Account savings (excluding top-up monies, government grants, and interest earned) above your Basic Retirement Sum if you own a property."

https://www.cpf.gov.sg/Members/Schemes/schemes/...

But, if you were to top-up your MA first, you will soon hit the BHS (Basic Healthcare Sum) which is currently capped at $60K, this will allow all your future MA contributions to flow into your SA if it hasn't hit FRS yet. It's an indirect way of topping up your CPF SA, while not being affected by the CPF clause I quoted above. This will ensure that you are able to maximise the amount you can withdraw from your CPF at age 55. Although some people might argue that you shouldn't make any withdrawal and let the interest grow it further, it's always good to have more options (: