Advertisement

Anonymous

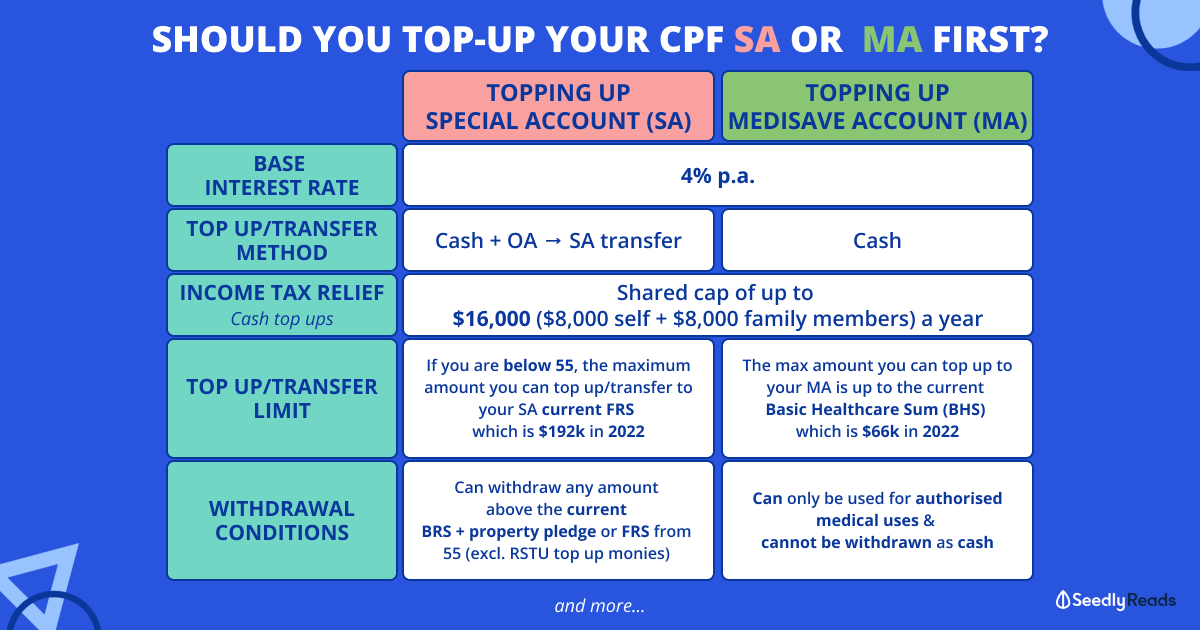

Should I top up SA via cash and transfer OA to SA aggressively in the early years?

I am worried about the cash top-up tax saving part. If I am at 120k tax bucket, my top up of 7k gives me saving of 11% of 7k. If I am the highest tax bucket, then a 7k top up would have 1540 tax saving. my question, although early cash SA top up and OA to SA transfer is good, it has a drawback of not able to enjoy tax saving at later years. And later stage the tax saving is also sizeable.

I am also thinking about this for my child. If I top up the child SA account since birth. I don't get tax saving and she may not able to get tax saving.

12

Discussion (12)

Learn how to style your text

Shengshi Chiam, CFA

03 Mar 2020

Personal Finance Lead at Endowus

Reply

Save

I think the ultimate question is whether you think cash is better or a saving account with guaranteed interest of 4%. Then I would probably choose cash. The flexibility to choose to spend and invest is within control of the individual. It is a trade off ultimately. Here is the take.

1, If income permits, then still top up SA and SRS accordingly. The FRS will hit eventually and don't worry about so much. There should be other ways to save tax when you are richer. :)

2, don't over top up SA for self and loved ones. As cash should have more value than SA top up. If used properly. Like get a good investment, a good vacation with family. A better housing and necessity spending.

3, if I am not purchasing a flat, then I should transfer OA to SA for better interest rate. As it is all locked up there and no use.

4, If I want to purchase flat. The question is whether I want to use cash or CPF OA to fund the purchase. Then it depends on how valuable each is. If cash is giving 5% yield and capital appreciation. And CPF is giving 2.5%. Then CPF OA is not as costly as cash. If cash is giving 1%, then should use cash.

Reply

Save

Irregardless whether you do rstu, the sa account balance will still increase due to your contributio...

Read 3 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi Anon,

This is a very personal decision that assumes that you have taken a cold hard look at your own cashflow and CPF/housing requirements, before you do the transfer. It is great that you are considering your options now!

Like you have pointed out, the OA to SA transfer will force you to artificially hit FRS earlier, and you would not be able to do RSTU top up in the future. If you forsee that your income will remain high, then you may want to use SRS accounts as a form of tax savings instead, as there is no limit and you can get equities returns for it.

I have never done the transfer, and in the past I invested my CPF OA monies in STI ETF (now I invest through Endowus) to maximise my wealth.

If you want to help your kid get a headstart in life, perhaps you can consider just investing in a low cost, globally diversified fund. That way her CPF remains untouched, and because she has a very long runway, she can get higher returns while taking some market risks. Hope this give an alternative perspective!