Advertisement

Anonymous

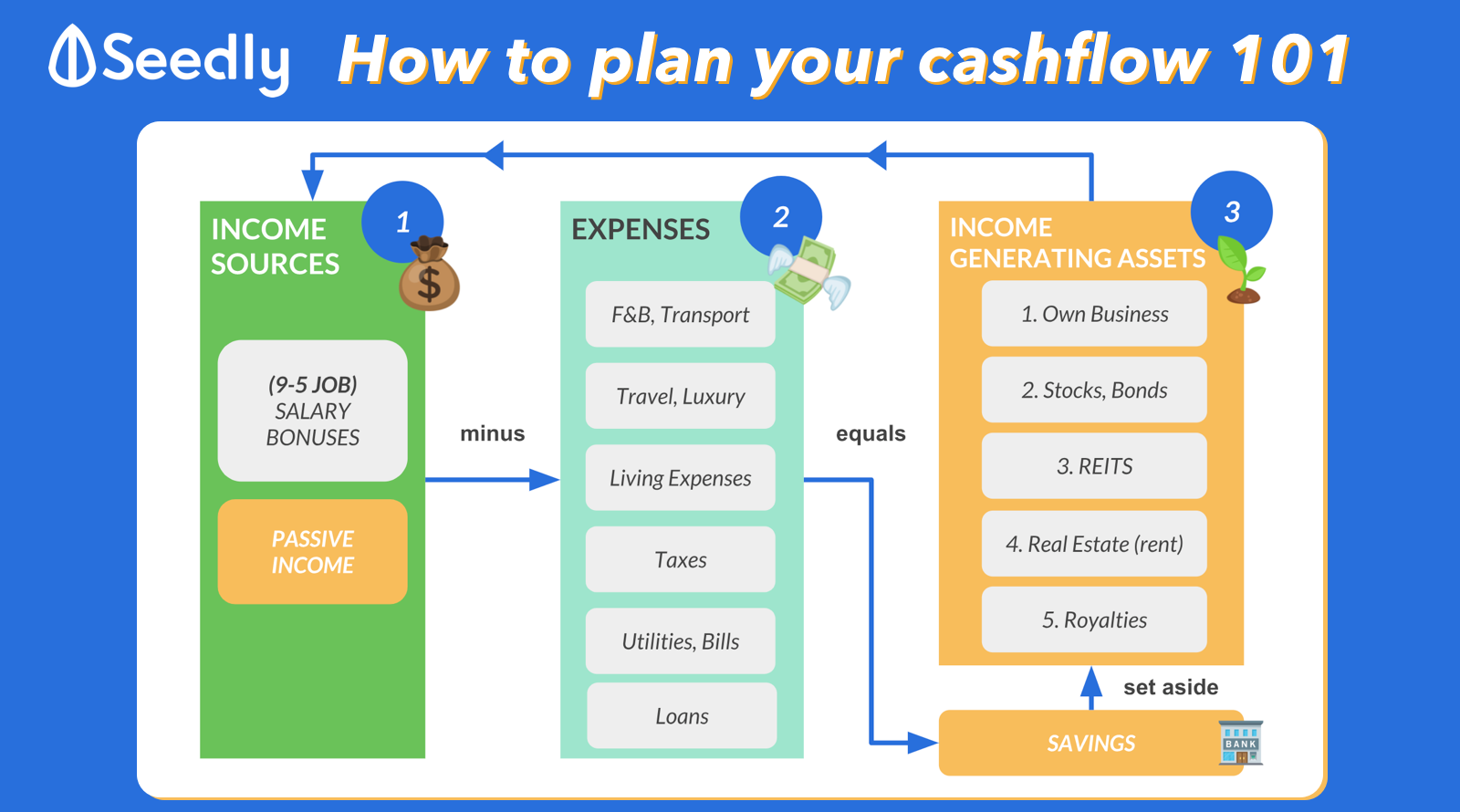

Parents are 62 yo and have not achieved retirement adequacy. I am 32 yo and earning a healthy income. Thinking of doing RSTU to Mom's RA which is currently <$60k and earns 5-6% interest. Should I?

Two issues are holding me back: i) RSTU is irreversible; ii) RA can only be drawn out either through CPF LIFE annuities or the old Retirement Sum Scheme (RSS).

My projections show that the IRR for topping up and enrolling in CPF LIFE's Standard Plan only becomes more than 4-5% (my hurdle rate) if my Mum lives beyond 85 yo. Any life span before that gives <4-5% - i.e I'd be better off investing on my own.

Have not done projections under the RSS as I am not sure how it works.

Any advice?Thanks

2

Discussion (2)

What are your thoughts?

Learn how to style your text

Reply

Save

View 1 replies

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Based on your question, you seem knowledgeable in terms of the payouts and calculations, so let's take it that you've gotten those aspects covered. These are other considerations that you may consider:

Am I able to provide my mum the CPF LIFE monthly payout amount without using CPF LIFE currently?

What happens if I lose the ability to provide her this monthly amount?

If I choose to invest instead, is my investment portfolio able to provide this monthly amount consistently? What happens during a major drawdown in my portfolio?

Does my mum have other form of savings/investments that will tide her through retirement?

While you can approach this issue from an IRR perspective based on your mum's lifespan, another possible way to think of CPF LIFE would be an insurance to ensure your mum gets a stable retirement with consistent monthly income upon turning 65. Is it worth buying an insurance with a premium of $X per month for Y years to ensure that mum gets consistent $Z amount till 90y.o.?