Advertisement

Anonymous

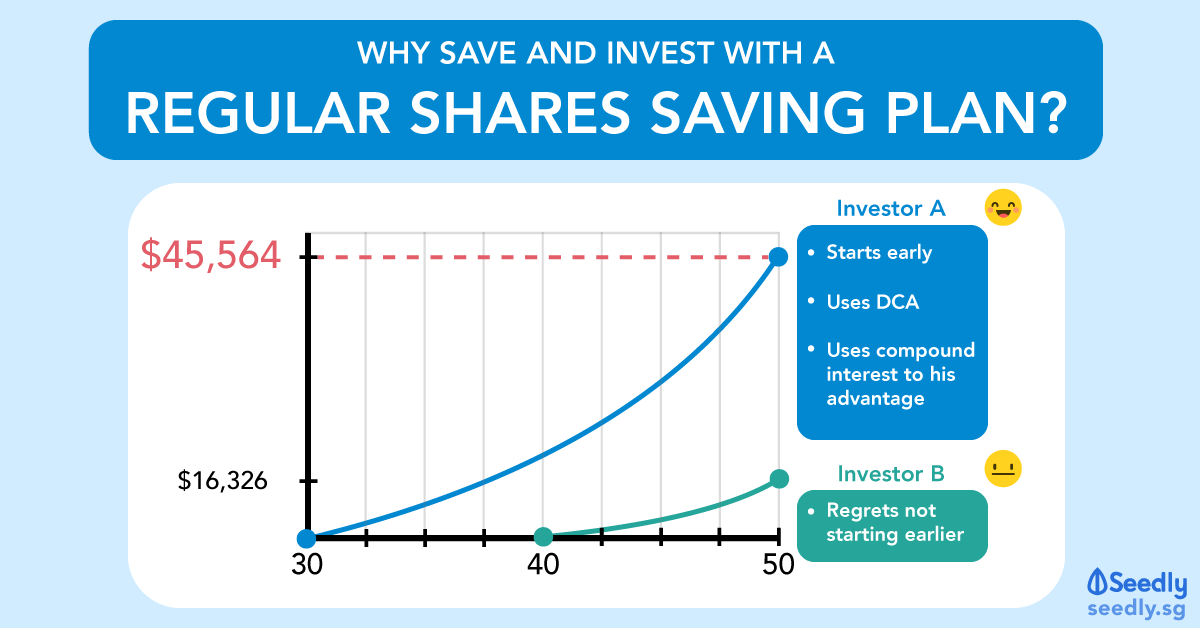

Is it wise to put $3k per mth into a Regular Savings Plan?

I've just started putting 3k per mth (1k each for Nikko STI ETF, Singtel and DBS), and have another 5k cash per mth for additional investment if needed. I've also set aside my emergency funds and have insurances covered. I'm 35 this year and married with no plan to have kids.

What can I better do with the money?

4

Discussion (4)

Learn how to style your text

Eric Chia

09 Oct 2019

Senior Financial Consultant at Prudential

Reply

Save

Elijah Lee

08 Oct 2019

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon, I would advise you to consider building a well-balanced portfolio. Going 100% on equities will lead to your portfolio exposed to market risk. You can consider asset classes such as bonds, ETF, UTs, annuities to balance out the overall risk of your portfolio. There are many asset classes available with their pros and cons so you should take time to understand the options in order to deploy your funds in a balanced manner and construct a diversified portfolio with reduced risk.

I'm going to take a step back and look at your situation as a whole. What is your purpose for investing? Were you trying to ensure that there would be sufficient income assets in retirement for you and your spouse to have comfortable golden years? If we look at the big picture, I would say that eventually, everyone wants to retire. What would we expect from our retirement (financially) would impact what kind of investment decisions we take and what asset classes we use to reach them. DBS and Singtel are relatively decent dividend payers, but one has to pay attention to the company in the long run as things can change. So you'll definitely have to monitor these companies.

I do note that your cash flow would be in the region of $8k/mth (since you have $5k/mth still available). I'm going to go out on a limb here and presume that you have a relatively significant income tax obligation. In view of this, you might want to also want to consider contributions to SRS to reduce your taxable income as well and then deploy your SRS funds. In this way, you'll cut your income tax and still be able to invest.

On the question of your spare $5K/mth cashflow, this can be utilized in many ways. You can start some RSP into UTs. Start an annuity. Put some in a high-interest savings account to act as a warchest waiting for market opportunities to show up. Contribute to SRS (as mentioned above). Although you seem comfortable with risk as you are doing equities, I can still only give general advice based on the details you provided. When you retire, look for income assets that form a stable, inflation hedged, low volatility portfolio. To that end, I would recommend you create a 3-pronged retirement strategy, ensuring that

- You have a systematic withdrawal plan from your assets

- Proper segmentation of your assets into various buckets and layers

- Have a basic retirement income floor with guaranteed income solutions for the essentials.

There's no one size fits all solution but I hope the pointers I highlighted will guide you towards finding the answer that suits you. Let me know if you like me to elaborate on any part of my answer.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi there, it seemed that all of your money is in equities, there's no guarantee in the returns that they can offer. You may want to consider diversifying your retirement nest into the other asset classes such as

You're pretty lucky you have quite the budget to play around with. So you can consider making better use of your money by putting some of them in places with better guarantees to hedge against risks which you are taking in other investments. Then your retirement strategy is stronger.