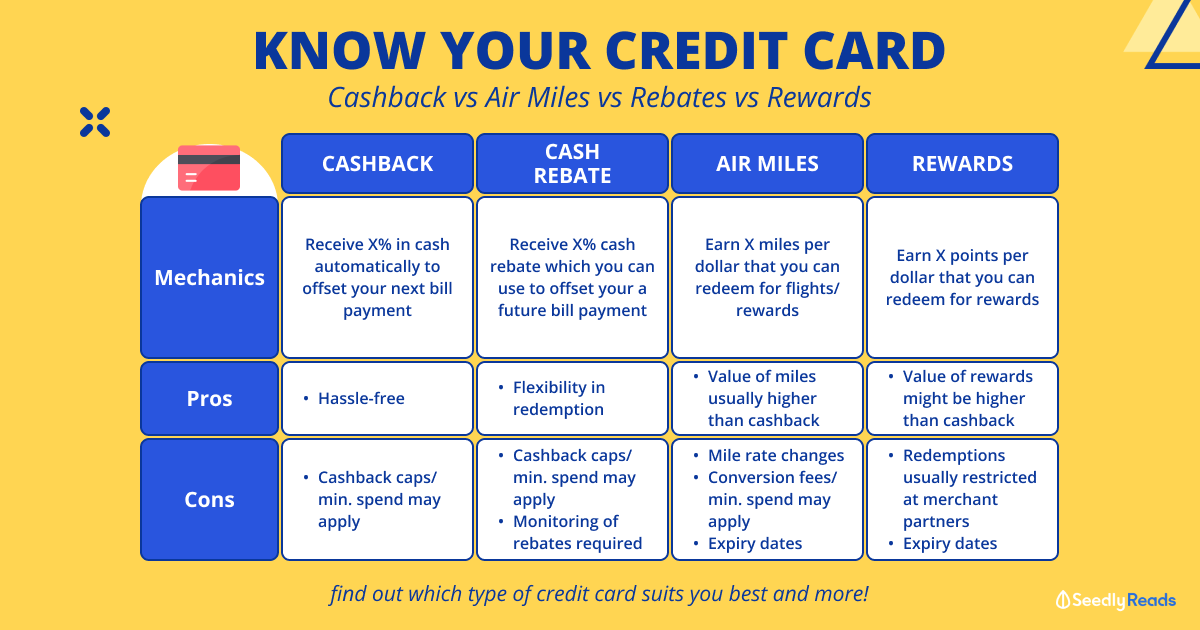

If I spend $500 or less every month, should I opt for a miles or cashback credit card?

Which would be the most beneficial rewards system in this scenario and which cards should i consider?

18

Discussion (18)

Learn how to style your text

Cedric Jamie Soh

20 Dec 2019

Director at Seniorcare.com.sg

Reply

Save

Keith Ng

19 Dec 2019

Assistant Digital Marketing Manager at Mandai Wildlife Group

UOB One, min spend $500/month - 3.33%

$500 x 3.33% = $16.65

$16.65 x 12 = $199.80

Miles cards at 4mpd, no min spend

$500 x 4mpd = 2,000 miles

2,000 miles x 12 = 24,000 miles

That's a one-way Business Class ticket to Bangkok ($962).

But it's Bangkok.. I can fly Scoot...

Well, using the right card and you can fly Business Class with the same spend.

Travel better for less.

Reply

Save

Certainly cashback card would be a better option because you can see the cashback rewards and use it after just a few spend.

For miles card, you do have to spend quite a lot to clock a good number of miles.

Reply

Save

Depends on what do you want out of your spendings. It also depends on your spending pattern too. If you're not even a traveller, I would suggest you don't even bother with miles. Personally I would think that cashback may work out better for you because the credit cards that give high mpd have expiry to the miles (which means you probably should clock sufficient spending in order for the miles to translate into something valuable), the credit cards that have no expiry to the miles have low mpd. So unless you are fine with taking a long time to accumulate your miles, it is more likely that a cashback card gives you a more tangible return.

Reply

Save

Angeline Teo

16 Dec 2019

Calculator at The Internet

Cashback!

Take the time to learn about miles, and wait for your income and spending to increase bef...

Read 14 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

If its me, I will prefer cashback as my spending is below $500 per month.

This allow me to have more consistent rewards, rather than miles that I need to accumulate over a long period of time for a decent redemption.

I will still keep a miles card for large spending.

For big ticket item, such as for travel, wedding, home furnishing etc, then I will use that miles card to earn miles.