Advertisement

Anonymous

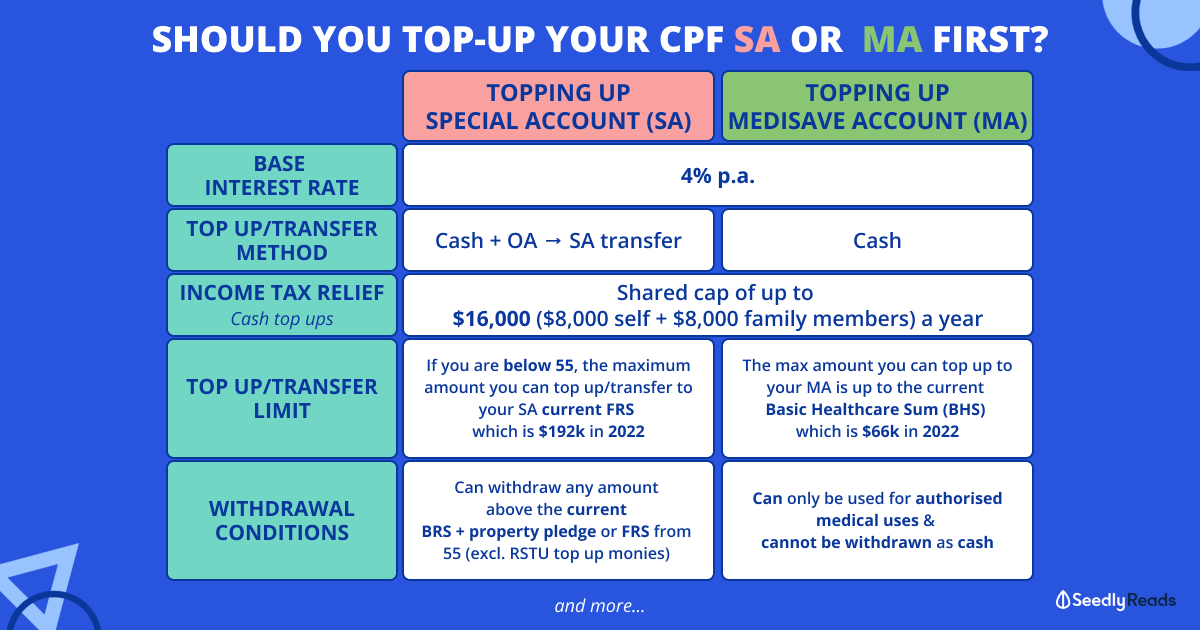

I’m turning 19 and now in national service. Should I top up my CPF? If so, which account?

8

Discussion (8)

Learn how to style your text

Gabriel Tham

07 Jun 2019

Tag Team Member at Kenichi Tag Team

Reply

Save

Siow Nan

23 May 2019

E at NUS

If you really want to forego the liquidity which you might need in the future, then MA topup shld be the first for you to consider, at least you can also use Medisave for paying part of MediShield plans.

otherwise, you can consider ssb which is safer and may provide you with certain amount of liquidity such that you can redeem it within 1-2 months if necessary at arnd 2% avg yield per year..

if you still have spare cash after setting aside some amount for emergencies, then at your age, you can try to explore riskier investment vehicles like stocks for potentially higher returns (but learn first and don’t overtrade if you are New in this)

Reply

Save

Vincent Tan Wen Bin

21 May 2019

Assistant Vice President at Thinkers Alliance

What is your objective of doing so?

If you're topping it up to save, I would say you might not st...

Read 2 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

That depends on your objective and immediate needs.

Do you need any cash in the immediate or near future? Like planning for house, BTO etc? As you are still young, I would suggest building up your personal cash savings first. Because you might want to use it for further studies, BTO in future, renovations, baby planning, wedding planning etc

Do you need the tax relief? (I suppose in NS the pay is still low so no need to pay tax at all)

For CPF topups, it can be top up to SA (which will grant you tax relief) or top up to all 3 accounts (OA, SA, Medisave), the allocation will be done for you, and the money split into all 3.