Advertisement

Anonymous

I am graduating this year and ready to adult (I hope). However, can someone help me to sort out my accounts please?

My savings are now down to $4k because I've been supporting myself for awhile now. I read that it is better to get 3 different types of account—savings, expenses, short term savings. Would like to know what are the recommendation you guys have? Is it okay to use DBS Multiplier as both Savings & Expenses?

I am now separating them to

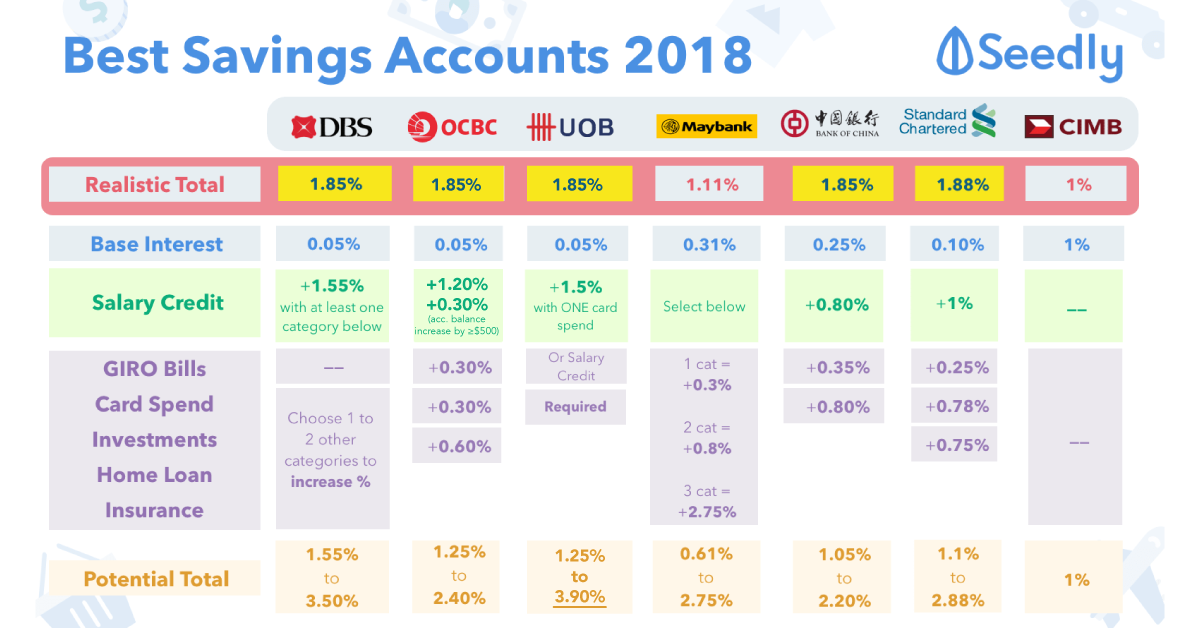

1. Savings — DBS Multiplier

2. Expenses — DBS Multiplier

3. Short Term — SCB Jumpstart

Thank you!

3

Discussion (3)

Learn how to style your text

Reply

Save

Elijah Lee

29 Jan 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Hi anon,

I'll just share my own way of doing my expenses to give you an idea:

Salary to OCBC 360 to satisfy salary crediting (no other requirement to get the extra interest, which is good for me)

A fixed amount transferred to POSB to spend

Rainy day fund in CIMB due to the high interest without any requirements

Of course, you'll have to go through the hassle to set this up, but once done, transfers between bank accounts is pretty much instantaneous. You can of course use one account to satisfy both savings and expenses, but then you must know how to manage it well.

Reply

Save

Pang Zhe Liang

22 Jan 2020

Lead of Research & Solutions at Havend Pte Ltd

Firstly, we need to have a complete understanding on our cashflow. Through this process, we will und...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

Standard Chartered JumpStart Account

4.8

785 Reviews

Maximum Interest: 2.50% p.a. for balances up to S$50,000

INTEREST RATES

$0

MIN. INITIAL DEPOSIT

$0

MIN. AVG DAILY BALANCE

DBS/POSB Multiplier Account

4.3

329 Reviews

OCBC FRANK Account

4.7

213 Reviews

Related Posts

Advertisement

With just $4k it might not be worth your effort to split into so many accounts.

Do note that there are min amounts to keep in most of these accounts. If you go below there will be a fee charged to you.

The disadvantages of having many accounts are;

1. lessen the free cash you have to use, without incurring charges, if you go below min amount.

2. Less interest received. With multiplier accounts, likely you can only fulfil the requirements of 1 account and not all accounts to get the best interest rates.

I will suggest you find 1 account that can have you the best interest rates, and use it to accumulate wealth to a meaningful amount before splitting into different accounts.

In mean time, you’ll have to monitor your expense, old fashion way, on excel sheet.

If you are really afraid of overspending, then either use the envelope method by withdrawal cash for you expenses or find an account with no or really low min amount.

For me, I’ll try to accumulate to say $50-70K before getting another account.

I used to like OCBC because you can allocate saving goals and ‘“lock” in an amount so it won’t be available to withdraw at the ATM. So that 1 account can effectively function as several accounts. Left because the interest isn’t that good compared to others.