Advertisement

For bank accounts with no salary crediting, which one would give the best interest for e.g. 30k funds? Or would it be better to put it in a FD or SSB as the funds are not ended urgently?

Give the variables above, what would be the best course of action that i can take that would result in the best results?

12

Discussion (12)

Learn how to style your text

Reply

Save

FDs and SSBs are fine if you are sure that the funds will not be needed urgently.

Reply

Save

Cedric Jamie Soh

22 Dec 2019

Director at Seniorcare.com.sg

For bank account with no salary crediting,

If you are below age 26, gof or SCB jumpstart as you can get 2%

CIMB Faster Saver at 1% is next good bank account

Citi Maxigain is good too.

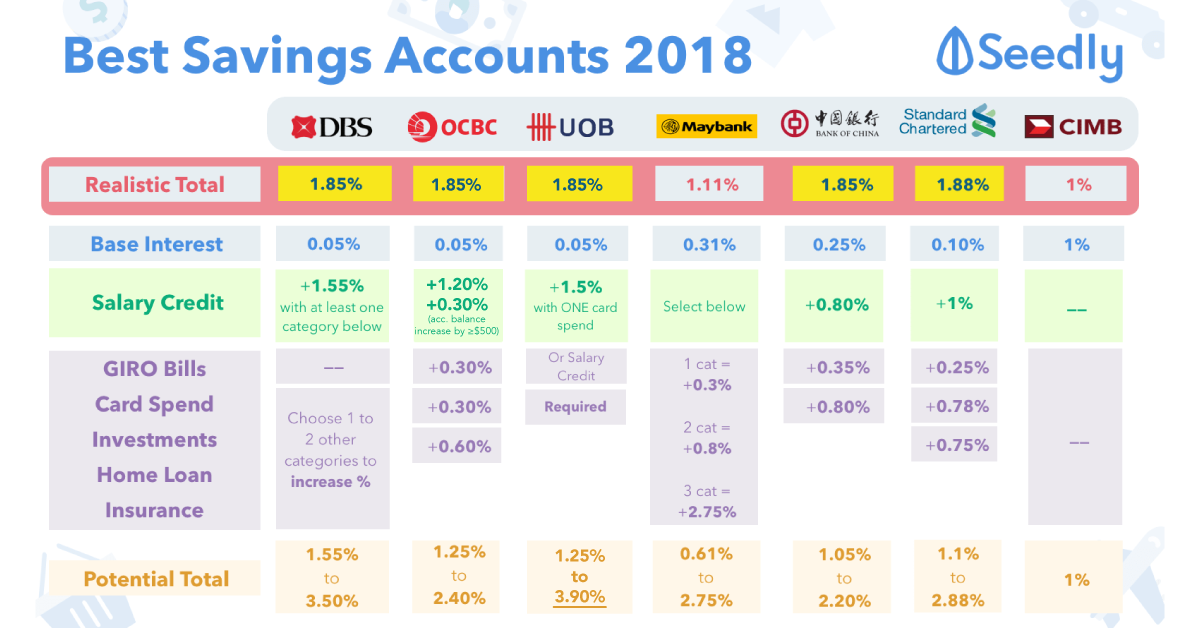

UOB One has higher interest but there are other criteria such as minimum credit spend before the next tier. (So is OCBC 360 account, even without salary credit, there are 2 more tiers)

Or you can talk to foreign banks (because local bank's fixed deposit rates suck) and ask for longer term fixed deposits.

I suggest singapore saving bonds also if you are risk adverse.

You can also read up on this higher interests than fixed deposits scheme.

Reply

Save

Bjorn Ng

22 Dec 2019

Business Analyst at 10x Capital

Do consider UOB One. Salary credit is not a main criteria. Instead, spend min. $500/month on your UOB cc (take a look at UOB x Grab promo), and create 3 GIROs from the account.

I think SSB interest rates right now is not worth to put it in, but the good thing about it is the liquidity where if you need the money suddenly, you can withdraw it out from SSB. FD has this disadvantage so only go for it if you have sufficient liquidity buffer.

Reply

Save

Pang Zhe Liang

06 Dec 2019

Lead of Research & Solutions at Havend Pte Ltd

Firstly, we need to have a complete understanding on our cashflow. Through this process, we will und...

Read 8 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

UOB One, if you can fulfill min. $500 spending + 3 GIRO. Followed by FDs and SSB, followed by CIMB Fastsaver. If you're less than 26 years old, you may also want to consider SCB Jumpstart.