Advertisement

Anonymous

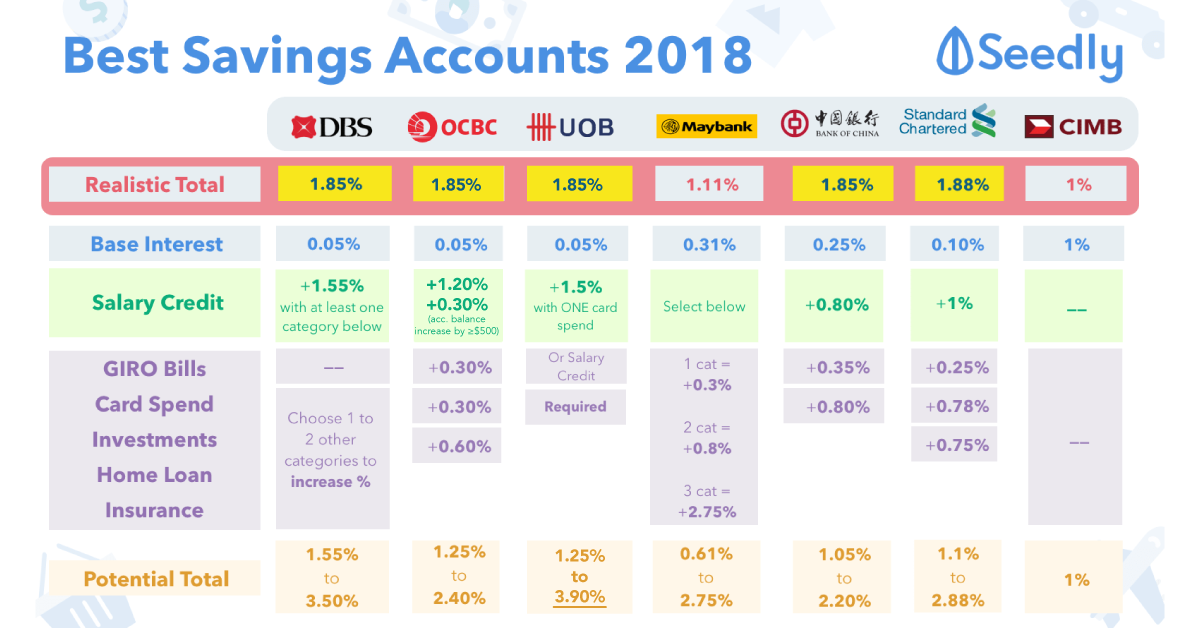

With the latest changes to the savings account interest rates, what are you doing differently to work around this?

Any smarter way to move my money around? My current effective interest rates are around 1.8% only. (only salary component). With the changes in DBS, OCBC, UOB and essentially every other bank. Please comment below if I missed out on any.

21

Discussion (21)

Learn how to style your text

Reply

Save

Dyon Yip

08 Apr 2020

Financial Consultant at Great Eastern Financial Advisers

Hi there!

Definitely a valid concern when the announcement was announced.

Here are some of my 2-cents worth point of view.

You can explore into the following areas:

Money Market/Low Yield Funds - Looking at least 1.8% and above would align with your current strategy, possibly to grow idling monies before allocating into other investment assets.

SCB Jumpstart Account: $20,000 at 2% p.a

- CIMB Fastsaver: 1% p.a (good for emergency funds)

Hope the above helps.

Cheers!

Reply

Save

Here to share my savings strategy! :) Would like to know if there's other better strategies out there or any opinion on my current strategy! :-)

*interest rates are subjected to post-changes from May 2020 onwards

1) SC Jumpstart : 2%pa on first 20k ($400/yr)

- already have 20k, placed these funds here to roll interest as I continue to build my capital.

2) DBS multiplier : 1.6%pa on first 15-25k ($240+/yr)

- I am currently building on my next 15k on this account so as to move on to step 3 (will explain again later). And since I have already started crediting my salary into POSB and opened a multiplier account so might as well continue on this account. However I still have to spend a few dollars on creditcard to acheive the 1.6%pa

3) OCBC 360 : 2.4%pa salary credit + 0.4%pa when you increase acc balance by $500/mth (as compared to prev month) + 0.4%pa $500 cc spend = 2.8-3.2%pa

These rates are only for $35k, hence I will move my 20k(SC) and 15k(DBS) into this account and start earning 2.8-3.2%pa. As for excess funds (other than $500topup) I will continue to pump into SC jumpstart for no-frills 2%pa and I might just close DBS multiplier. *** is optional as we wouldn't want to spend the extra $500/mth for the interest of (0.004x35k=$140/yr), not really worth but if you are already spending that amount on cc normally then why not :)

As for other criterias it is out of my way to achieve those categories so I would stick with this final step 3) which would make up my emergency funds + travel funds + electronics/medical etc

4) Invest!!!

- Excess funds after 40-50k cash should be up for investments! :) (only if the i/r are worth and depends on liquidity)

Reply

Save

1) SingLife for emergency funds (2.5% on 10k)

2) SCB JumpStart (2% on 20k)

3) DBS Multiplier for salary crediting (2% on 50k, main acct with salary + cc + rsp)

4) Joint POSB Savings for salary and dividends crediting ($0 balance and maintains another multiplier acct with cc, 1.85% down to 1.6% on 25k)

Also consider if you can get more from OCBC 360 with salary + $500 cc

Reply

Save

For me I love flexible and liquidity with cash without overspending so most of my funds are in Mayba...

Read 7 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

DBS/POSB Multiplier Account

4.3

332 Reviews

Up to 4.10% p.a.

INTEREST RATES

$0

MIN. INITIAL DEPOSIT

$0

MIN. AVG DAILY BALANCE

OCBC 360 Account

4.3

209 Reviews

UOB One Account

4.3

92 Reviews

Related Posts

Advertisement

Maxing out various frills-free accounts

SingLife first 10k at 1.5%

SingLife 10-99k at 1%

Jumpstart first 20k at 0.4%