Advertisement

Anonymous

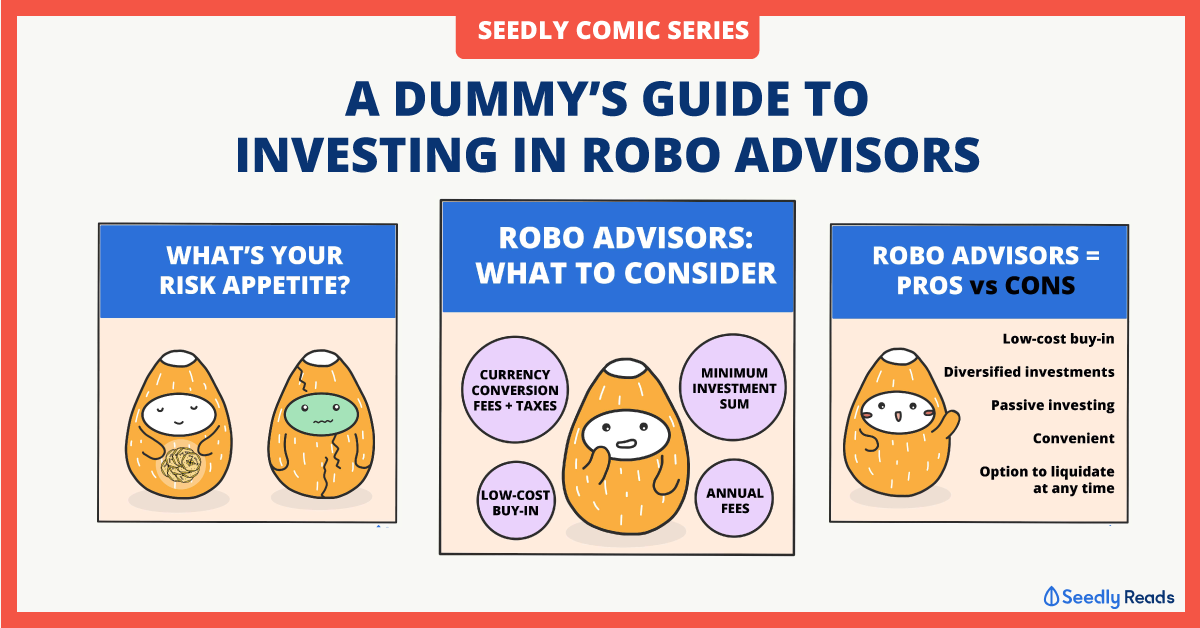

Why do many feel that robo advisors are low cost when the fees are calculated against AUM? Is it really that low cost as advertised?

It became few hundreds to thousands when portfolio hit above 5 digits.

3

Discussion (3)

Learn how to style your text

Elijah Lee

10 Jun 2020

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Robo advisors' costs are low relative to the fees/charges of comparable alternatives. The reason for the much lower cost is usually due to:

The type of underlying assets they are investing in.

The advice given is automated based on the data client chooses.

The lack of actual human handling each client's portfolio.

You can bypass these fees by investing yourself and save some money, which is why you may feel that the fees are high.

Reply

Save

I'm curious to know more about this too....

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1297 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

662 Reviews

AutoWealth

4.7

223 Reviews

Related Posts

Advertisement

Hi anon,

It's quite common in the industry to peg fees to a percentage of the AUM.

If the AUM goes up as a result of the portfolio growing, the absolute amount of the fee also goes up, even if the percentage stays the same (say, 0.5% p.a.). And if the portfolio goes down, the absolute amount also goes down.

This creates a situation where the robo (or the human advisor) wants to ensure that long term growth is delivered so that the client is happy that his portfolio is growing, and the advisor/robo is also compensated for the work in growing the portfolio, so that both parties can work towards a win-win scenario.

Possibly one way to reduce fees is to step down the percentage as the portfolio grows bigger. But this is up to the robo.

Also, if there is only one fee, then we are also avoiding the performance fee based on high watermark that hedge funds and other discretionary portfolio services possibly charge.

To be fair, the robo has to keep the lights on. The advisor also needs to eat and make a living.

0.5% as a fee for robo is quite low. There are also advisory services (via human advisors) which also charge 0.5%. In the end, the question would be: Are robos suitable for you? Or would you invest on your own? Or do you prefer to work with a human advisor to shape a strategy for yourself? No single answer is correct, it all depends on you.