Advertisement

Discussion (2)

What are your thoughts?

Learn how to style your text

Lim Boon Tat

29 Jul 2021

Mathematics at Cambridge University

Reply

Save

View 1 replies

Write your thoughts

Related Articles

Related Posts

Related Products

StashAway

4.7

1297 Reviews

StashAway Simple Guaranteed 3.55% p.a. (Guaranteed rate)

Cash Management

INSTRUMENTS

None

ANNUAL MANAGEMENT FEE

None

MINIMUM INVESTMENT

3.5%

EXPECTED ANNUAL RETURN

Mobile App

PLATFORMS

Endowus

4.7

662 Reviews

Syfe

4.6

936 Reviews

Related Posts

Advertisement

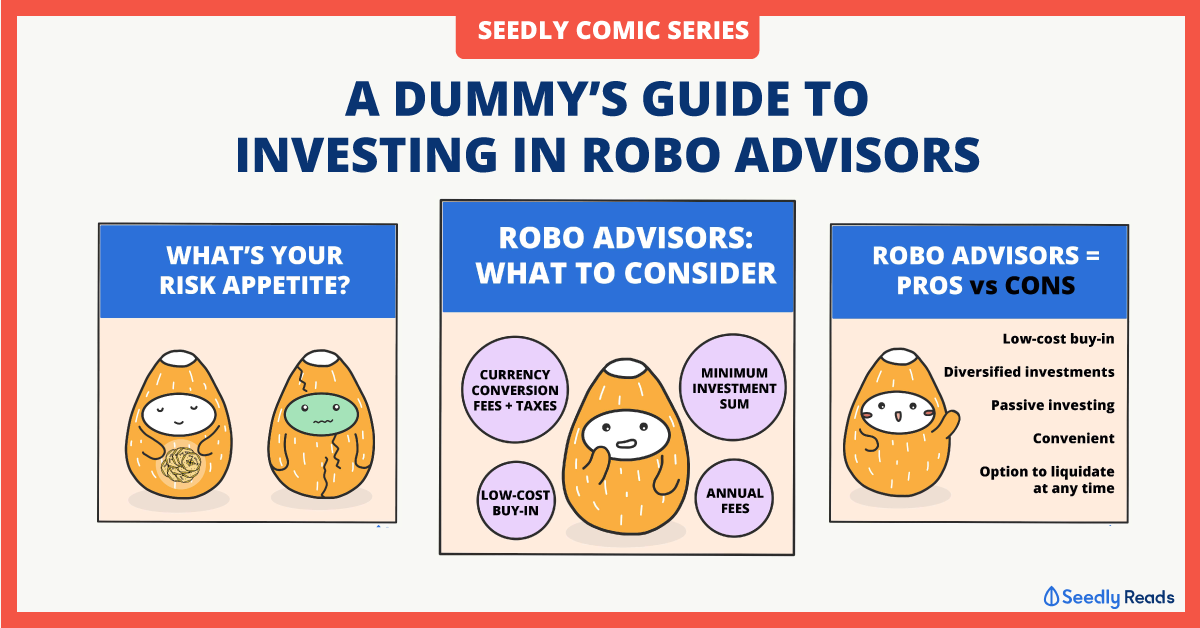

Robo-advisors generally tries to be your trusted advisor. They do webinars, "market updates", holds your hands when markets go down, and you can have multiple different "portfolios" through one single-login, and with the spiffy interface most of them have, you can't beat the ease of use. ETFs, in general, even AOA ones, involves some level of DIY. first you got to find a brokerage, and manage the entire registration process, which may or may not be as easy as the robo-advisors. Then you need to physically press "buy", and decide how many (not that many brokerages have the easy-button of "use all my money in the account"). Robo-advisors, again, like your trusted advisor, will help you "rebalance" your portfolios (generally subscribing to the belief of "reversion to the mean"), and also tax-loss harvesting (not so applicable in Singapore). Rebalancing between different ETFs on your own is a little tedious, involving buying and selling.