Advertisement

Anonymous

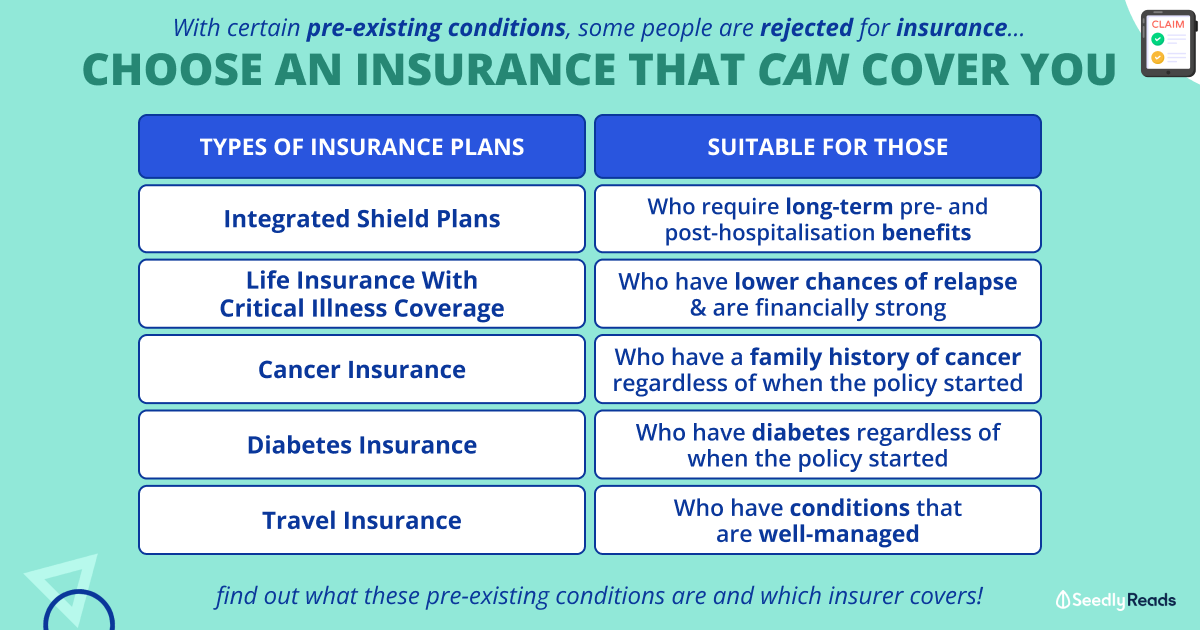

Should I take an an ILP with death and TPD cover if I have a pre-existing condition?

I am single, in early 30 with pre-existing condition. The only insurance plan I can get is an ILP with death and TPD cover. Should I take it?

As a single and young person, I don't feel that I need death & TPD benefit anytime soon. However my agent strongly advised me to take up this plan as it is hard for a person with cancer history to get offered with a plan. I saw the projected value, by the time I reach 60 (which is more likely to claim the TPD benefit), the total premium that I've paid will be almost the same amount as the sum assured. So whats the point? Wouldnt I be better off to save and do my own investment for higher returns?

4

Discussion (4)

Learn how to style your text

Elijah Lee

06 Feb 2021

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Pang Zhe Liang

06 Feb 2021

Lead of Research & Solutions at Havend Pte Ltd

Truth about Total & Permanent Disability:

Firstly, there is no absolute correlation between Total & Permanent Disability and age. For example, an accident (which may occur anytime) can result in a person's disablity as well.

Premium Allocation for Investment-Linked Policy (ILP):

Next, for an investment-linked policy, your premium is used to cover the cost of insurance (in your case death benefit, total & permanent disability benefit), as well as to invest the remainder into the selected investment-linked funds.

Depending on the returns of the investment-linked funds, the potential cash value may be

higher than your capital; and/ or

higher than the insured amount.

Needs Analysis:

Then again, we will need to go back to basics on why you need life insurance and I have summarised some of the common reasons in Part 1.2 here: 3 Types of Insurance Policies in Singapore

At this point, we will need to evaluate and plan for the long-term. For example, will you be buying a house or to start a family in the future? If yes, will you like to have the financial leverage to hedge against the potential risk of dying too early, or inability to work till retirement?

If the answer is no, then there is probably no point in getting life insurance at all.

On the other hand, if your answer is yes, then you will probably need life insurance. And generally the earlier you get life insurance coverage, the cheaper the cost of insurance.

Types of Life insurance:

Further to the point when you need life insurance coverage, the question will be whether you should get an investment-linked policy for your protection needs. Generally, the insurance component works in similar fashion to an increasing term insurance policy, i.e. cost of insurance increases over time. As a result, this may not be an efficient way to get insured in the long run.

More Details: Types of Term Insurance Policies in Singapore

Consequently, we will need to understand your needs once more - if your priority is on life insurance coverage only (i.e. not on the potential investment cash value), then you may be better off with a term insurance policy or a participating whole life insurance policy. This is because the insurance charges is usually level in both cases. In other words, the total cost of insurance (for term or whole life insurance) will likely be cheaper than that of an investment-linked policy. Hence, this may become a point for consideration as well.

More Details:

Overall, this is what I will suggest:

Establish your long-term goals.

Understand your needs and how an insurance coverage may help you.

Determine the type of insurance policy that you should get.

I share quality content on estate planning and financial planning here.

Reply

Save

Write your thoughts

Related Articles

Related Posts

Related Products

Great Eastern GREAT CareShield

4.1

18 Reviews

$5,000

MAX MONTHLY BENEFIT

Unable to perform ≥ 1 ADL

MONTHLY PAYOUT CRITERIA

300% of first monthly benefit

MAX LUMP SUM PAYOUT

Unable to perform ≥ 1 ADL

LUMP SUM PAYOUT CRITERIA

Singlife Careshield Standard

4.3

3 Reviews

NTUC Income Care Secure CareShield

No rating yet

0 Reviews

Related Posts

Advertisement

Hi anon,

Sorry to hear about your medical history at such a young age. I hope the cancer is in remission already.

You need death/TPD cover if you have liabilities or dependents. Most TPD definitions also have a provision to pay out if you are certified permanently unable to earn a wage, so that can be something to consider as well.

However, liabilities get paid off and dependents will be come independent one day. Thus they don't last forever and a term plan covering only the critical years is probably better suited to your case. A typical term plan to cover death/TPD will likely be cheaper than an ILP. Remember that the payout from the term plan is fixed, and so is the premium. And when you retire, you probably don't need death/TPD cover any more.

There is also the possibility that you can get coverage in future, typically after 5 years in remission you may try again to get CI coverage. So don't give up hope.