Advertisement

Anonymous

Should I cancel/ surrender/ continue with my Vicocare?

I am holding insurance from NTUC income - Vivocare 100. Life/ critical illness with 100K payout ( before 65 there’s a booster to 3x) and early CI for 100K; premium paid is 15 years of 4K SGD per Annum. It’s whole life insurance with cash value.

I’m now into 5th year for premium n the more I calculate the more I don’t feel justified for paying such due to the Low premium

What’s the thought process here?

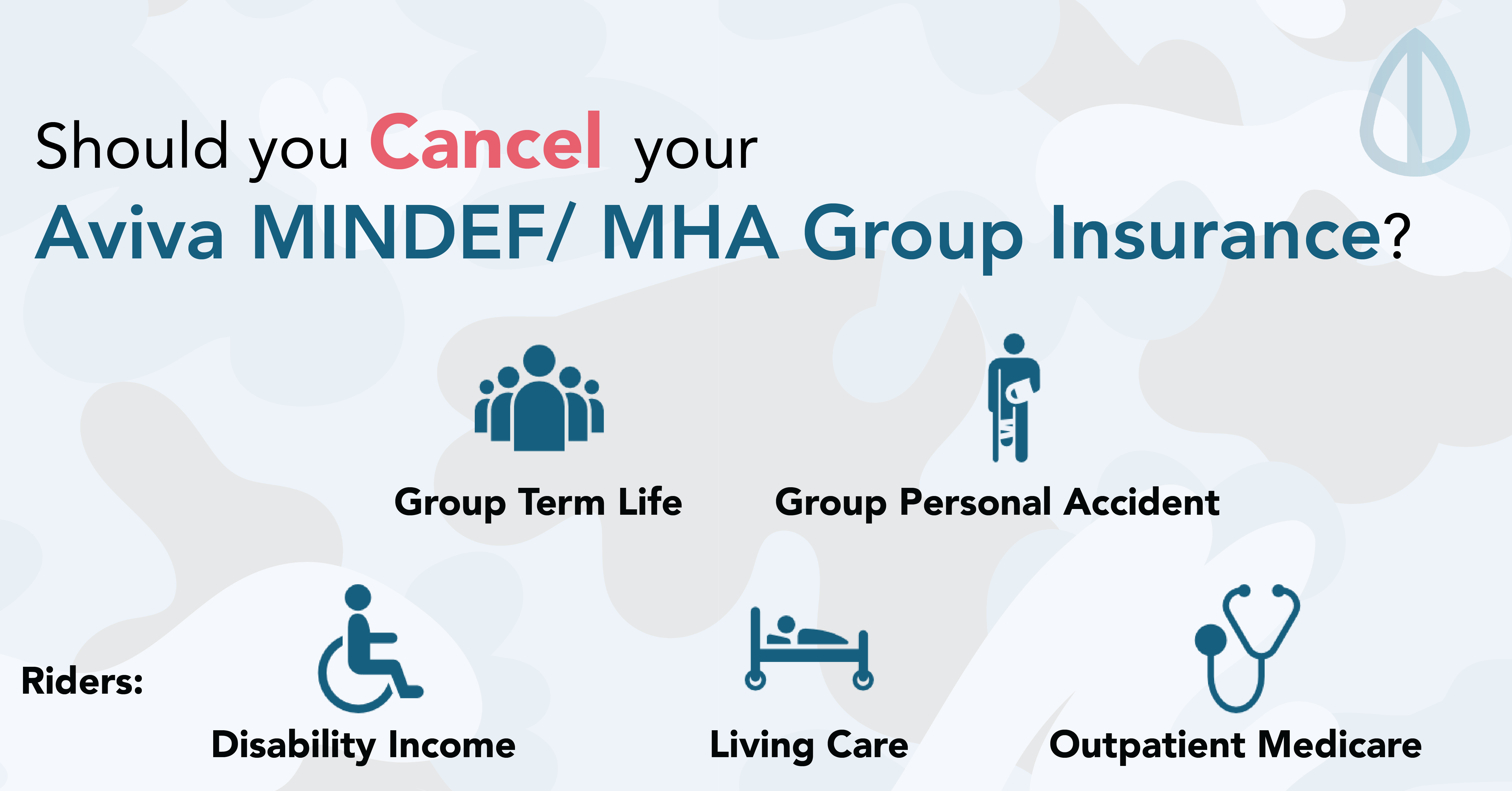

I currently also have the Aviva Mindef living care and life. 100K as well.

4

Discussion (4)

What are your thoughts?

Learn how to style your text

Loh Tat Tian

24 Sep 2019

Founder at PolicyWoke (We Buy Insurance Policies)

Reply

Save

View 3 replies

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Could you explain better when you say " the more I calculate the more I don’t feel justified for paying such due to the Low premium"

I am trying to understand your thought process over here.

But all in all, a Whole Life is not meant to be an investment or IRR generator, whereby its meant to be held to pay for your non-traditional CI treatment methods (CI protection) or for your dependents (Death).

It is a hybrid Whole Life with Term policy. I never advocate surrender.

But if you truly wish to surrender, I will buy over your policy.