Advertisement

Anonymous

Is the Standard Chartered JumpStart account or DBS Multiplier better for me?

Which is better for a recent 23-year-old graduate and full-timer?

8

Discussion (8)

Learn how to style your text

Reply

Save

##edit: SCB interest still stay as 2% even after you pass 27 as confirmed by the community, though it's up to the bank discretion whether to maintain this interest in the distant future##

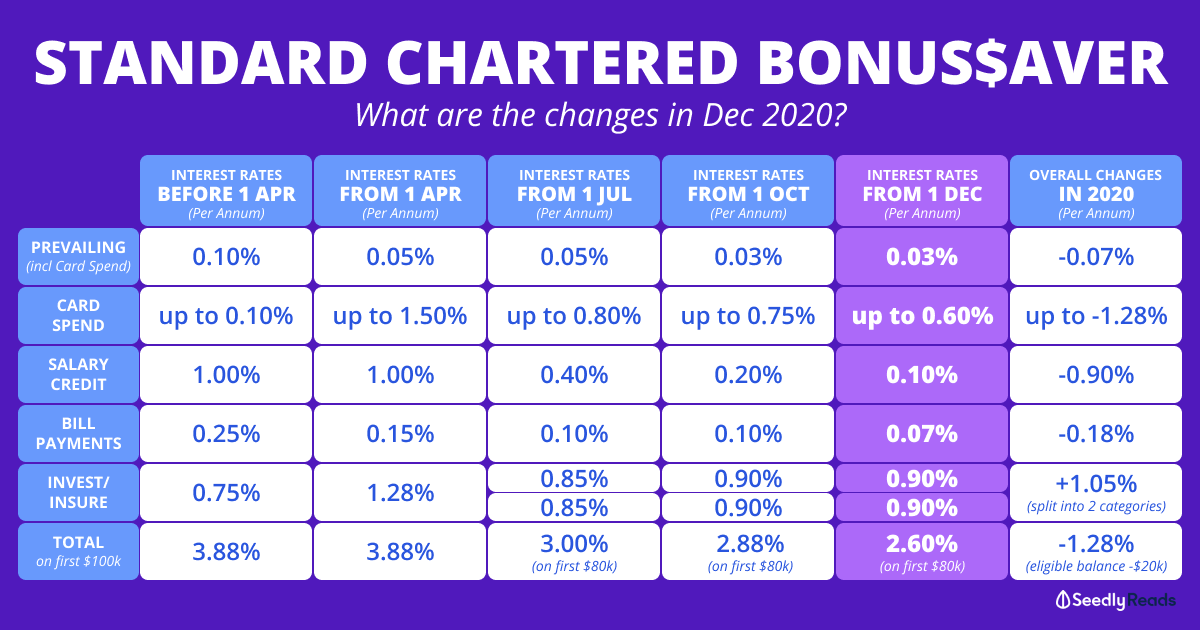

Standard Chartered JumpStart account can guarantee a 2% p.a. interest for up to 20k. The account does not have any penalty if you fall below any minimum account. The SCB debit card also has a 1% rebate for any amount spent, capped at a rebate of 60 dollars.

Whereas for DBS Multiplier, you would first need to credit your salary and transact in one or more of the categories (credit card spend, home loan instalment, insurance, investments). DBS Multiplier advertised that you can get up to 3.8% p.a. interest BUT that is if you achieve total eligible transactions of more than or equal to 30k a month, AND already have 50k in this DBS Multiplier account AND transactions in 3 or more categories. This means that to hit the 30k a month, say you credit 5k salary a month to your account, you need to have another 25k or more in your other transactions (credit card, home loan instalment, insurance and investment)! So realistically speaking, most undergraduate would only be able to hit the 1.85% p.a. tier (whereby total eligible transactions per month is 2.5k to 5k).

You can check out more about DBS Multiplier on:

dbs.com.sg/personal/deposits/bank-earn/multiplier

So in my opinion, I would open both accounts. SCB jumpstart account would kinda be my savings account whereby if you have spare cash saved from either your part-time work or parents allowance last time, I would just dump the money there to treat it as a "fixed deposit". The interest paid here is even higher than most fixed deposit currently in Singapore.

For the DBS Multiplier, I would treat it as a "spending account" whereby spending with the credit card can allow you to get back better rebates than the SCB debit card. (Do note some DBS/POSB credit cards have minimum spending to get back rebates) dyodd!

If you already have 20k in your SCB, then just leave the rest of the money in your DBS Multiplier to earn the DBS Multiplier interest since SCB jumpstart interest is capped up to 20k. Once you hit 27 or older, your salary would probably have increased such that you would be able to hit the higher tier of DBS Multiplier and earn better interest. This will coincide with the age limit of SCB jumpstart and can just transfer your money to DBS Multiplier if necessary.

These are just my opinions so you should plan out your financial means and how to allocate a portion of your salary to the jumpstart account if you do follow my advice on opening two accounts. Jiayou!

Reply

Save

Kenneth Lou

08 Oct 2019

Co-founder at Seedly

Seems like the community has confirmed:

**THE INTEREST RATE WONT BE REDUCED AFTER YOU TURN 27...

Read 2 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Products

DBS/POSB Multiplier Account

4.3

329 Reviews

Up to 4.10% p.a.

INTEREST RATES

$0

MIN. INITIAL DEPOSIT

$0

MIN. AVG DAILY BALANCE

Standard Chartered JumpStart Account

4.8

785 Reviews

OCBC FRANK Account

4.7

213 Reviews

Related Posts

Advertisement

I have both and I'm a recent 23 year old graduate too haha.

To see if the DBS multiplier is worth it you can use the calculator:

https://www.dbs.com.sg/personal/deposits/bank-e...

Basically there are 2 questions you can ask yourself:

1) Are you able to hit 1 more category easily (besides the credit card spend)?

2) Is your salary + credit card spend is 5k?

If your answer is yes to both - go for the multiplier. If it is no for either one, go for the SCB account. For question 1, dividends are the easiest to hit and I'm sure you have heard about the SSB ladder. However, with the current rates on the SSB, it may not be worth the trade off. My view would be to open both - use the jumpstart as a savings account and multiplier as the spending account. It helps you to budget as well.