Advertisement

Anonymous

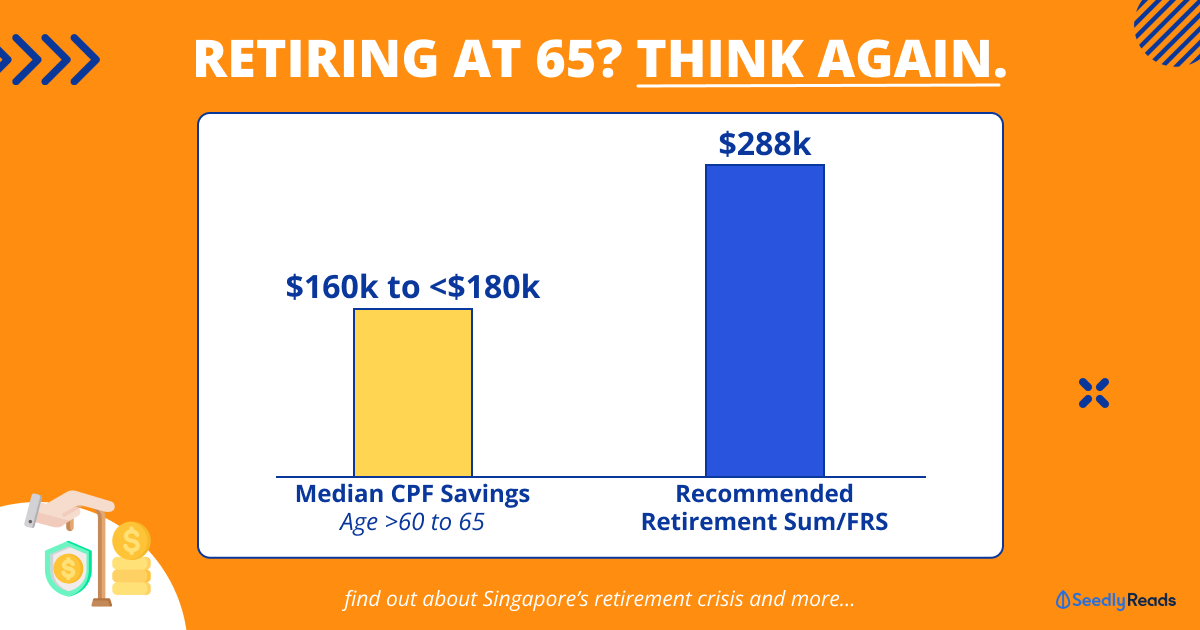

I will be 39 this year. Have reached FRS in SA and foresee that I should be able to hit ERS when I retire so long as I continue to work and contribute to CPF.

Qns: I have used over $200k of CPF for my HDB. Does it make sense to voluntarily refund this amount back to CPF OA? Noted that the refund amount comes with acrued interest too. But since I will likely hit ERS, my current thinking is that I will eventually get back what I refunded when I reached 55 years old, right? I.e., CPF OA will just likely be similar to a savings account with a bank. It is also risk free interest compounded at 2.5%. Any other considerations I should note? Tyvm!

8

Discussion (8)

Learn how to style your text

Reply

Save

Imo, are you going to sell your HDB? If no, then I'd say don't bother with the refund, because when the flat get sold after you pass on, the accrued interests doesn't matter anymore.

If yes, then next question to ask is, are you risk-adverse or risk-taker; are you active or passive investor?

My spouse is sooo passive that I didn't bother with the risk appetite and advise for partial volunteering housing refund, because of the stability in keeping money in CPF.

We also started regular investing portfolios so that the investment is "auto-pilot" and hopefully get better returns.

Reply

Save

In the current high interest environment, it is fairly easy to beat that 2.5% interest you will be g...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Maybe consider paying off housing loan (save interest) or topping up medisave yearly?