Advertisement

Discussion (3)

Learn how to style your text

Elijah Lee

06 Jul 2021

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

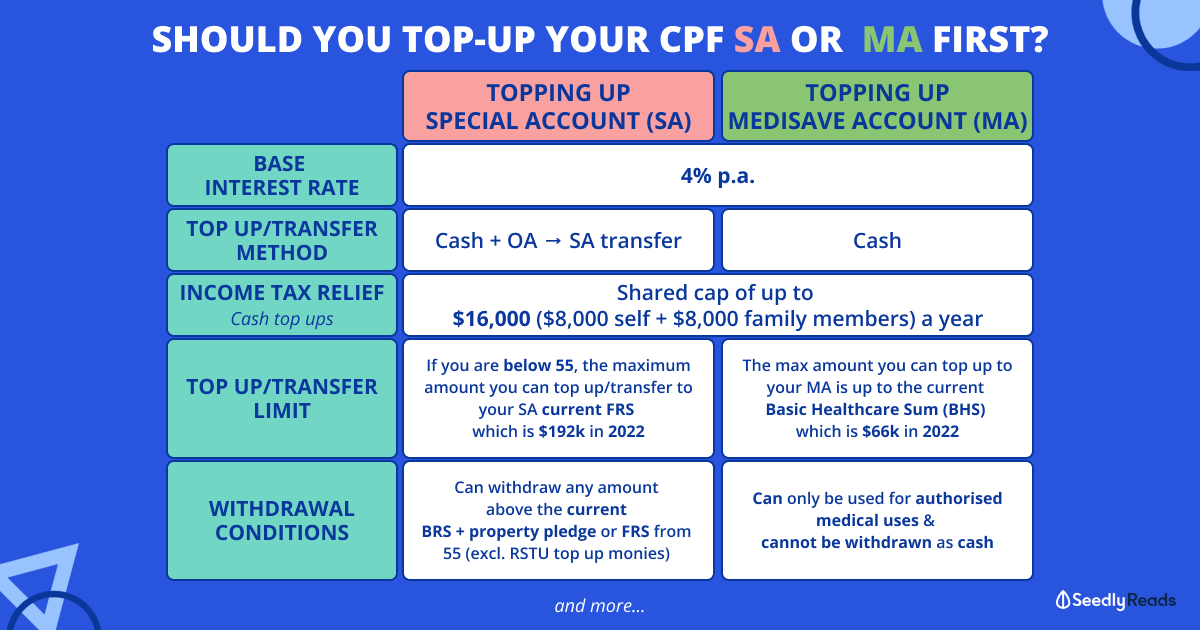

The $7000+$7000 tax relief is for voluntary cash top up to own SA and/or eligible loved one’s SA via RSTU. If the cash top up is lower than $7000, the tax relief is the actual amount of top up.

For voluntary cash top-up to the MA, the tax relief is the actual amount of top-up, provided the BHS is not reached and the CPF annual limit is not reached. Any excess voluntary contributions will be refunded without interest the following year.

If your MA has not reached BHS, you may want to consider topping up MA first as it can be used for medical stuff. SA is only for retirement purposes. And in my experience, usually once BHS is reached, it is easier to reach BHS the following year.

Yes, once BHS is reached, the MA contributions after will be redirected to the SA if FRS is not reached. If FRS is reached, the MA contributions will flow to OA. So there is more monies flowing to SA and if you contribute cash top-up for RSTU, the SA will grow faster.

If you prefer not to tie up your cash in the CPF system, you could choose to contribute to your SRS instead for tax relief purposes.

Reply

Save

Tan Choong Hwee

06 Jul 2021

Investor/Trader at Home

If you MA already hit BHS, you can't VCMA (Voluntary Contribution to MA) anymore. It is the MA porti...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi Ken,

The $7K top up applies to Retirement Sum Topping Up schemes for either yourself or your loved ones (another $7K). You can actually top up to the prevailing FRS (for receipient aged below 55) or prevailing ERS (age above 55), but you only get relief for the first $7K in each scenario and only if the receipient has lesser than the FRS amount regardless of age.

This $14K is independent of the CPF annual limit of $37740.

MA top ups grant tax relief on the full amount but will utilize your CPF annual limit, thus, if you are going to max your CPF contributions from work, your top ups will be refunded to you without interest.

The sequence of spill over is as follows:

Once you hit BHS, MA contributions from work or 3 account VC will spill to SA if you are not at FRS. If you are at FRS, it spills to OA.

MA interest at the end of the year will also spill to SA if you are not at FRS, and OA if you are at FRS. SA interest will stay in SA. There is no hard cap for SA monies, unlike MA, where the BHS is the hard cap.

Personally, I'd top up SA first. MA will build up as long as you work, and if you are self employed, you have to top up MA anyway, but no one makes it compulsory for self employed to top up SA or even do 3 account VC. So I know my MA balance will grow, and thus I prefer to focus on building my retirement safety net.