Advertisement

Anonymous

Any insights about the AIA Smart Wealth Builder (Participating Endowment)? No intention to leave a legacy (ie: for passive income only), is CPF top-up better?

Premium Term: 20 Years ($3000 annually)

Policy Term: Till Age 125 of insured (passed to spouse/child upon death, the policy continues); if none then 105% of paid premiums/ 101% of guaranteed value to a nominee.

Year 15: unlimited withdrawal w/o penalty

Year 20 (premium term ends): Guaranteed: $61,500; Non-guaranteed total: $72,082 (illustrated 3.25%)

Author: 98 years till Age 125.

Investment risk: Mod.

Already invested in Robo; BCIP; 2 other endowments (both mature 2025).

No CPF top-up (yet).

3

Discussion (3)

Learn how to style your text

Elijah Lee

20 Nov 2019

Senior Financial Services Manager at Phillip Securities (Jurong East)

Reply

Save

Loh Tat Tian

20 Nov 2019

Founder at PolicyWoke (We Buy Insurance Policies)

The question to ask yourself would be...

(1) what does the endowment serve its purpose in the grand scheme of things?

(2) What is the payout that you are looking at?

(3) How far away are you from your Full Retirement Sum?

(4) Can this be complemented with other types of investment?

(5) what is the tax relif that you get should you take some of it to contribute to SRS or CPF RSTU?

Do what it makes sense to you (overall networth/assets increase).

Reply

Save

Pang Zhe Liang

19 Nov 2019

Lead of Research & Solutions at Havend Pte Ltd

AIA Smart Wealth Builder is a participating policy. Accordingly, the returns depends on the insuranc...

Read 1 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Hi anon,

AIA SWB is a perpetual endowment plan.

First, you'll have to ask yourself: What do you need this plan for?

If it doesn't fit your need, then there's no need to get a plan

If you are planning for a definite timeframe goal (e.g. future children's education), whereby funds must be needed, then such a plan might fit into your needs.

If you are planning to accumulate a portion of your wealth with a floor (the guaranteed component) that grows over time, then such a plan might fit into your needs, since you are cushioned from negative market impact.

If such a plan fits your needs, then you'll want to consider comparing across multiple insurers to see your options (many insurers carry perpetual endowments), and evaluate factors such as the guaranteed component and non-guaranteed component to find the most effective plan for your money. An independent financial advisor can assist you here.

I had a client get this type of plan recently because she wanted to set aside money for her new born son's future education, but wasn't sure if he'd go through the JC or poly route, and thus no idea of when he would enter university. She needed a guarantee on her monies with a decent return and flexibility to draw down when the time came.

Please note that I wouldn't classify such plans as passive income, because you'll have to manually draw on the policy value each time you need to withdraw funds, if you don't, you don't get any income from a plan like this. Contrast this with an annuity which will pay you automatically on a monthly basis when the time comes.

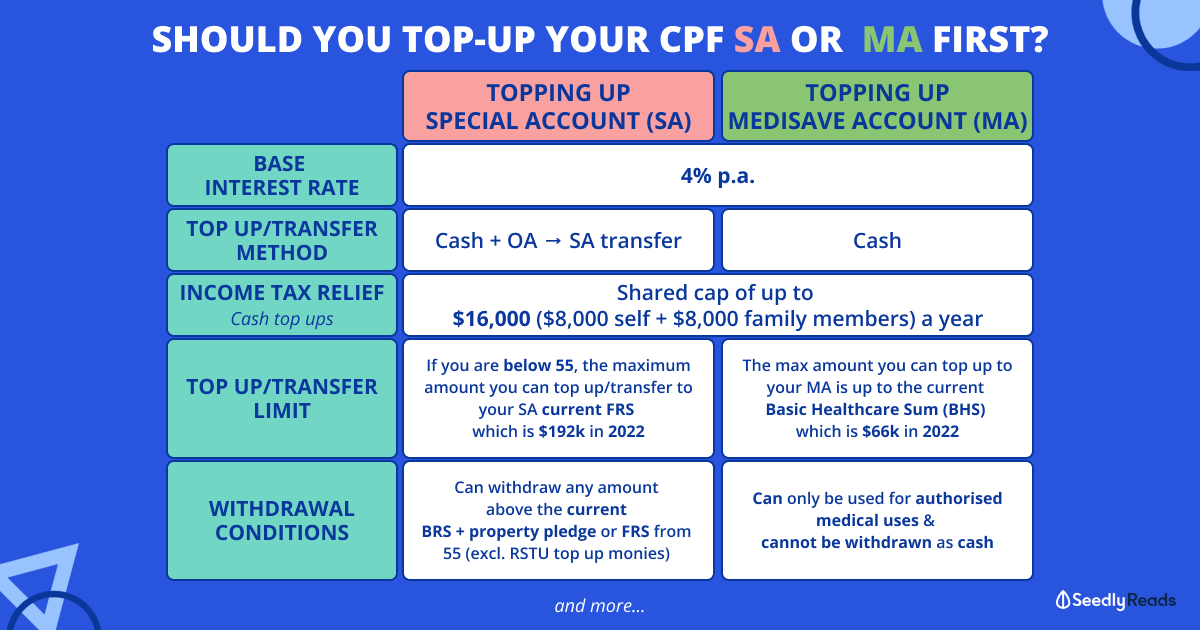

Is CPF top up better? Yes and no. RSTU will give 4%, but you are not in control of when you can get the money. If policy changes occur, you might end up waiting longer than expected. Also, you can't take anything from SA till 55, which might be a little too far away for your liking. However, in such cases, I'd divide and conquer. Nothing wrong with locking up some monies in CPF SA for a higher guaranteed return, but having your own perpetual endowment for easy access to monies down the road. I'd normally recommend just a short payment term, as the guaranteed returns only start becoming apparent when the premiums have ended and the plan is running for 5 to 10 years.