Advertisement

Anonymous

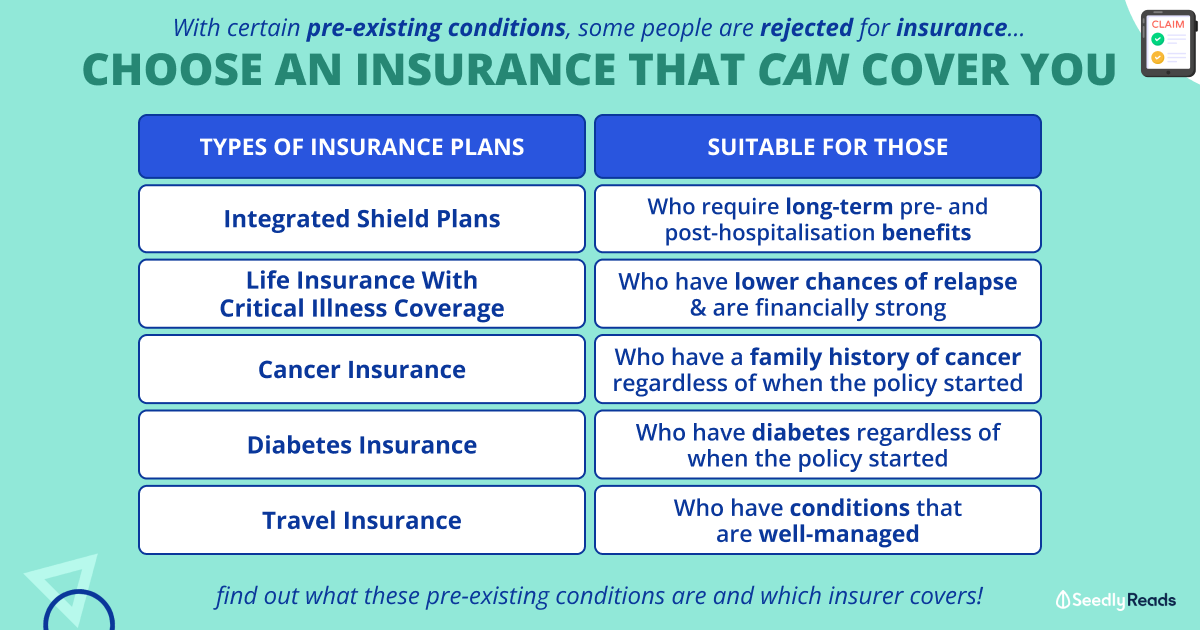

Advice needed for M, Age 31 next bday, non smoker. Have pre-existing condition of severe OSA (BMI 21). Living with parents who are still working, and looking to marry soon. What coverage to top up?

Got these before I was diagnosed:

400k D/TPD, 100k ECI, 300k CI @ 6134 pa

1) GE Shield plan - Private ($838 pa 100% rider)

2) GE Flexilife mulitplier X3 whole life: $65k x3 for Death/TPD/CI ($2594 pa with personal accident and DII riders)

3) NTUC i-term till age 65: $150k Death/TPD, $50k CI ($478 pa)

4) GE Critical Care Advantage till age 65: $100k ECI ($926 pa)

5) NTUC Living Policy whole life: $40k Death/TPD/CI ($700 pa)

6) GE Early Cancer Care Plan B till age 85: $100k for cancer ($596 pa)

16

Discussion (16)

Learn how to style your text

Pang Zhe Liang

13 Apr 2020

Lead of Research & Solutions at Havend Pte Ltd

Reply

Save

Colin Lim

13 Apr 2020

Financial Services Consultant at Colin Lim

Hi, need to find out more about your situation.

If your parents decide to retire, are they self sufficient, you do not need to provide for them.

Do they have health insurance?

What do you work as?

You are going to get married soon, great news!

Is your wife gonna stop working to take care of kids? How many kids do you want?

You will be getting property right?

There are alot of things i need to know to give u a holistic solution. But in a good view, at least you are covered. 👍🏼

Reply

Save

Tan Li Xing

13 Apr 2020

Financial Consultant at Prudential Assurance Company (Singapore)

Hi Anon,

Just based on the information alone, it does feel comprehensive. And like Hariz mentioned,...

Read 2 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

Advertisement

Firstly, it will be valued if you have done a consolidation for all your existing insurance policies. Generally, the this helps you to understand all your existing coverage at a glance. Thereafter, it is more efficient when we do planning for your future.

Key Reasons Why:

Why Every Client needs an Insurance Policy Summary

Healthcare

On the whole, it looks like you are well-covered for inpatient hospitalisation. For a side consideration, you may wish to consider boosting hospital income as an add-on to offset co-payment and inconvenience. Otherwise, it is good to keep it as it is.

Moreover, I will suggest for you to have a detailed look on the personal accident and DII riders for GE Flexilife Multiplier. While the cost is not high, it usually makes more sense to get a standalone personal accident coverage. This is because of the better benefits that it offers (as compared to the rider).

Life Insurance

For your case, we need a further breakdown on the insurance coverage that you have and stays with you over time. For example, I noticed that there are some term policies that stops at age 65, as well as a whole life policy that works on a multiplier basis.

With this in mind, we will need to spend some time to understand you and your needs. As an illustration, you are intending to get married soon. Thereafter, you may move out and start a family. Accordingly, we need to ensure sufficient payout for your dependents, e.g. parents, wife, children in time to come, as well as for your liabilities, e.g. car, house. If you intend to move to a second property, e.g. because of family needs, then it is imperative to plan ahead. This is simply because insurance gets more expensive over time!

In brief, it may look like you have sufficient life insurance coverage now. However, we will only know the truth when we do a detailed life planning for your future.

Critical Illness

Depending on when you bought the policy, we need to have a further analysis on the scope of coverage, e.g. number of covered conditions, terms for payout. This is especially important for early critical illness as the definition and terms for payout may not be the same.

It is only then we can be confident on what you have and its adequacy.

As for #6, take a look at what it covers. Thereafter, evaluate whether it makes sense to keep it or to channel the funds for critical illness coverage or other purposes instead.

General Rule

In any case, as a general rule,

10% to 20% of your annual income on healthcare insurance and life insurance

Basic Life Cover = 10 times your annual income

Critical Illness Coverage = 5 times your annual income

More Details:

Understanding Your Personal Cash Flow

While we value the importance of insurance coverage, be sure to keep your budget in check to ensure that you are not overspending on insurance itself. Ensure that you have sufficient liquidity for other purposes, e.g. marriage, family, house, filial piety, holiday, retirement.

Finally, spend quality time to understand yourself and plan how your future will be like. Thereafter, it will be clear on whether there is any coverage that you should top up.

I share quality content on estate planning and financial planning here.